ExplainSpeaking-Economy is a weekly newsletter by Udit Misra, delivered in your inbox every Monday morning. Click here to subscribe

For a while now the issue of the old pension scheme (OPS) versus the new pension scheme (NPS) has dominated news. Unfortunately, instead of creating more light, the debate has only generated heat as it has morphed into a political slugfest between Congress supporters and BJP supporters.

In a nutshell, the detractors of the OPS argue that it is fiscally unsustainable — that is, governments in India do not have the money to fund it — while the detractors of NPS call NPS politically unsustainable — that is, it fails to address the felt needs of the people.

The dominant narrative, however, is that Congress is resurrecting the OPS — a scheme that it threw in the dustbin in the first place — just to achieve political power even though it knows that it will be financially ruinous for governments in the future. That’s why you might have read that Congress’ return to OPS has been labelled as both bad economics as well as bad politics.

This article aims to take a step back and help you understand how to think about a pensions system in our country. Once there is an agreement on the framework, the analysis becomes less chaotic and more inclusive.

And it is important to be inclusive because contrary to how it appears at the moment, even those who don’t serve the government in India get old and require an old-age pension.

To be sure, according to the World Economic Forum: “For the first time in human history, people aged 65 and over outnumber children aged five or younger”. And while this stress may be less for a country such as India, which has a relatively younger population profile, there is such a thing as longevity risk.

Story continues below this ad

Longevity risk points to a scenario where rising life expectancy could result in pension and insurance companies needing more cash because people are living for longer than anticipated.

In this context, merely obsessing over the nitty-gritty of OPS and NPS makes one miss the forest for the trees.

A good starting point is a working paper titled “Public Expenditure on Old-Age Income Support in India: Largesse for a Few, Illusory for Most” by Mukesh Kumar Anand and Rahul Chakraborty of the National Institute of Public Finance and Policy. NIPFP is an autonomous research institute under the Ministry of Finance, Government of India.

So, where does India’s pension system stand in a global context?

Story continues below this ad

There is an index for ranking the pension systems across the world. It is called the Mercer CFA Institute Global Pension Index.

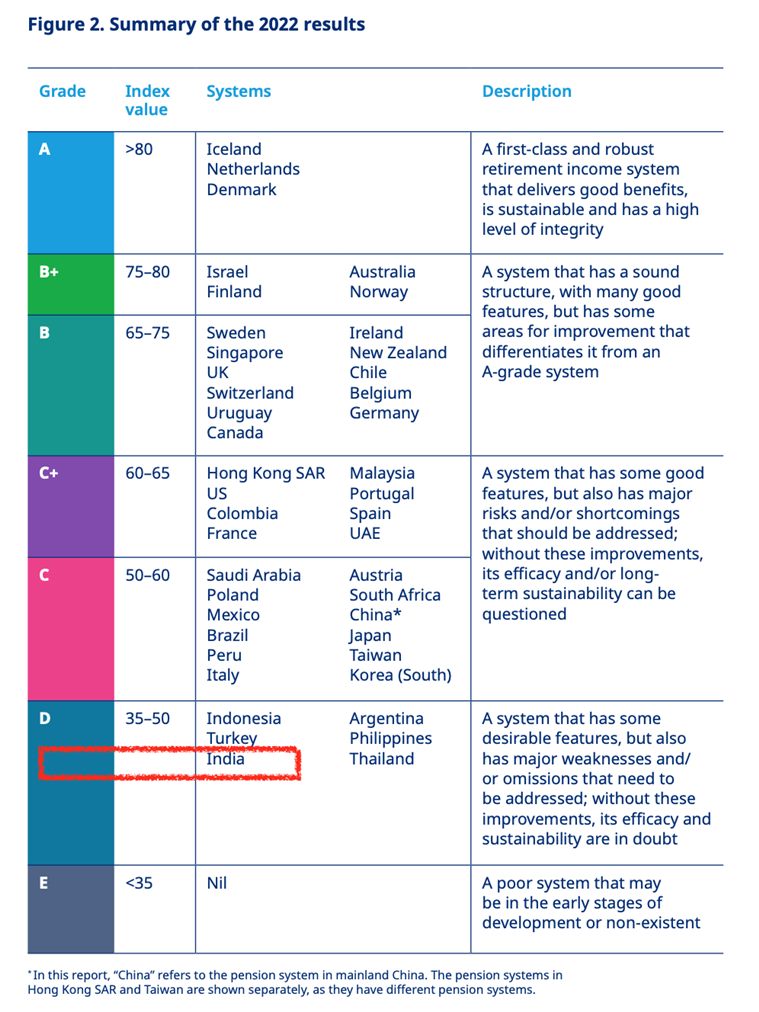

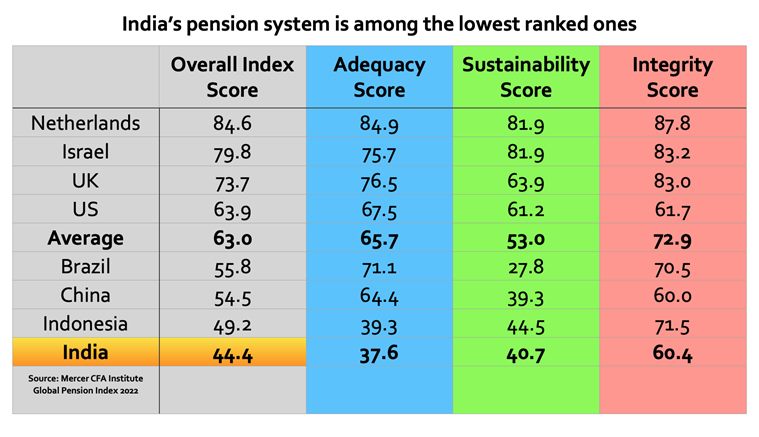

The 2022 edition of this index ranks India’s pension system at 41 out of the 44 countries it considers. That’s a low rank but it is also important to note that India has consistently ranked low on this index even when only 16 countries were analysed in 2011.

Table 1

Table 1 provides a brief summary of where India stands relative to other countries in this index. Based on the index value, India is placed in grade ‘D’. There is a grade worse than ‘D’ but there are no countries in it.

So, what does this index track?

The index report admits that it is neither easy nor straightforward to compare pension systems across the world. Imagine for a moment the differences in population profile and requirements, economic growths, government revenues, regulatory maturity and the development of private markets.

Story continues below this ad

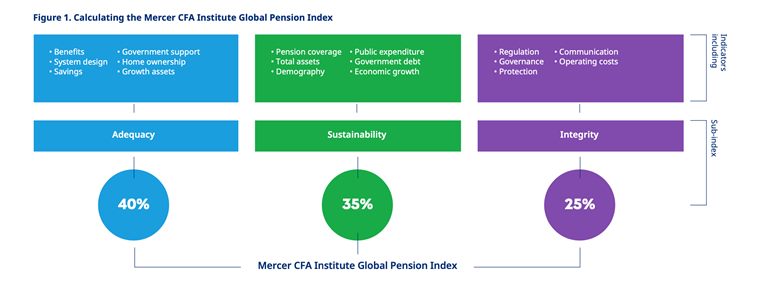

Still, David Knox, the lead author and senior partner at Mercer, explains that the index ranks countries on three criteria:

#1 Adequacy: What benefits are future retirees likely to receive?

#2 Sustainability: Can the existing systems continue to deliver, notwithstanding the demographic and financial challenges?

#3 Integrity: Are the private pension plans regulated in a manner that encourages long-term community confidence?

Chart 2 provides more details of the three sub-components and their weightage in the overall index.

Story continues below this ad

And Table 3 gives a more detailed look at where India stands on each sub-component.

A quick look at the average score of 44 countries suggests that the pensions regime in India is nowhere near adequate, remotely sustainable and scores relatively low in integrity.

But this is the index and one might want to know what all this means in the Indian context.

That’s where the paper of Anand and Chakraborty, which was written in 2019, is useful.

Story continues below this ad

Here are some highlights about the gross inadequacy of India’s pension architecture.

- At least 85 per cent current workers are not members of any pension scheme, and in their old age likely to remain uncovered or draw only social pension

- Of all elderly, 57 per cent receive no income support from public expenditure, and 26 per cent collect social pension as part of poverty alleviation

- 11.4 per cent of the elderly draw defined benefit as government ex-workers (or their survivors), cornering 62 per cent of system expense

- The system for old age income support entailed 11.5 per cent of public expenditure, and sub-national governments bear more than 60 per cent

- Contributory program funds invested in government paper soak up 40 per cent of all interest payment of sub-national governments

Point C above is crucial because that is where all the current debate of OPS vs NPS is situated — that’s less than 12 per cent of the elderly and it corners 62 per cent of all the expenses.

Point D is also quite relevant to the current debate of OPS vs NPS since 60 per cent of the expenditure burden for pensions is on state governments.

So what is the framework that yields such a lopsided pensions system?

Story continues below this ad

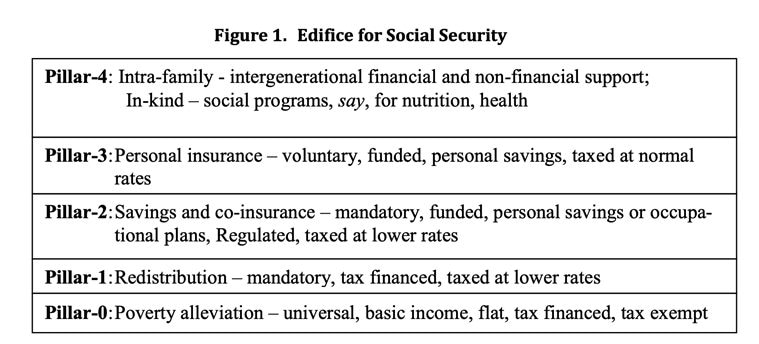

In 1994, the World Bank provided a framework in its publication titled “Averting the old age crisis”. In 2008, it refined it to provide “The World Bank Pension Conceptual Framework”.

Zero pillar: A non-contributory basic pension from public finances to deal explicitly with the poverty-alleviation objective

First pillar: A mandated public pension plan with contributions linked to earnings, with the objective of replacing some pre-retirement income

Second pillar: Typically, mandated defined contribution (DC) with individual accounts in occupational or personal pension plans with financial assets

Story continues below this ad

Third pillar: Voluntary and fully funded occupational or personal pension plans with financial assets that can provide some flexibility when compared to mandatory schemes

Fourth pillar: A voluntary system outside the pension system with access to a range of financial and non-financial assets and informal support such as family, healthcare and housing

Table 4

Anand and Chakraborty have tweaked it for India and it is presented as Table 4.

“Differing pillars in the pension system place differing demand on public funds. For example, pillars 0 and 1, are financed exclusively out of current revenue. These extend direct benefit to the elderly. In contrast, development of pillars 2 and 3 consists in participation and contributions, particularly of non-elderly,” state the authors.

It is noteworthy that the OPS falls under Pillar 1 and the NPS falls under Pillar 2.

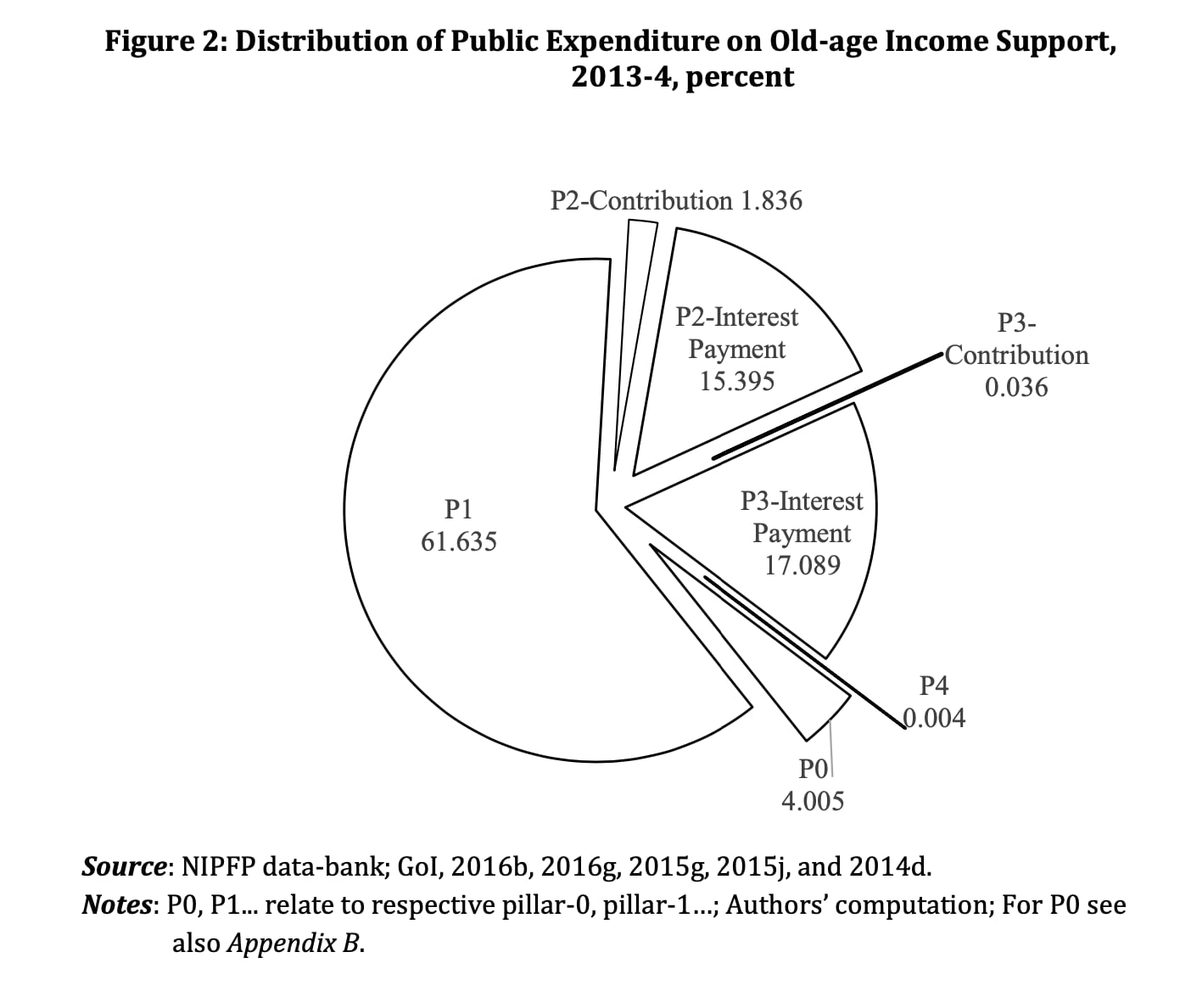

Chart 5

Now look at Chart 5; it shows how lopsided India’s pensions system as well as the debate around it is.

P1 or Pillar 1, where the government funded pension schemes to a small percentage of elderly accounts for almost 62% of all public expenditure.

Pillar 0, possibly the most essential one, gets just 4% of the total outgo.

How did this lopsided arrangement come into being?

Anand writes that most countries in the world accord some patronage to their ceding public servants, with rules that define retirement benefits as state (social) obligation (pillar-1).

“The practice has origins in erstwhile monarchies, where meritorious public servants were rewarded benefits upon retirement. However, the reward then was drawn only at the ‘pleasure’ of the benefactor and, often co-terminus with death of benefactor or beneficiary. That arrangement often retained a heavy lid on both state obligation and benefits. In the present world, not only the modern states are longer-lived (than average for an erstwhile monarchy) but also the obligation may extend beyond the life of the public servant. And, if not adequately calibrated, this could cause a sharp escalation in resultant benefits,” states the paper.

Upshot

The larger point highlighted by these numbers and framework is that India’s pensions system is in a dire need of a reform and that doing so will be both good politics and good economics.

Of course, merely fluctuating between OPS and NPS is not a reform. OPS was problematic on the count of sustainability while NPS may not only appear hugely discriminatory — at least to officers belonging to the same service but different generations — but might also suffer from inadequacy.

Is it time for India to relook its pensions system? Should the current debate be broadened to look at pension requirements for the whole set of elderly?

Share your views and queries at udit.misra@expressindia.com

Until next week,

Udit

Table 1

Table 1 Chart 2

Chart 2 Table 3

Table 3 Table 4

Table 4 Chart 5

Chart 5