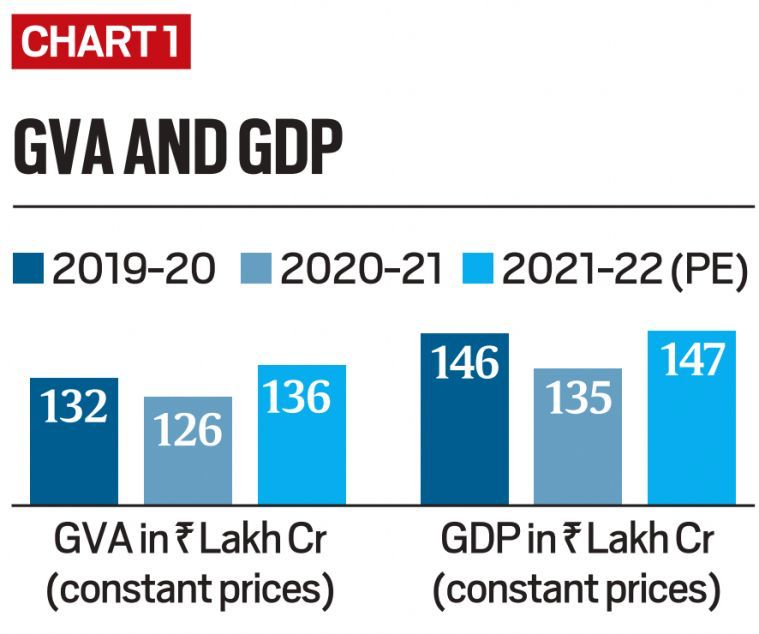

Simply put, GDP provides the demand side of the economy, and GVA the supply side. (Source: MoSPI)

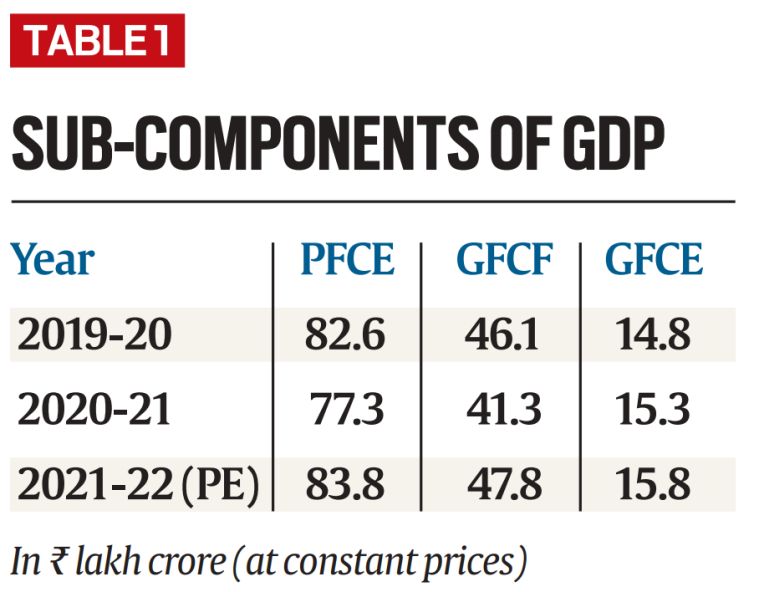

Simply put, GDP provides the demand side of the economy, and GVA the supply side. (Source: MoSPI) Sub-components of GDP (Source: MoSPI)

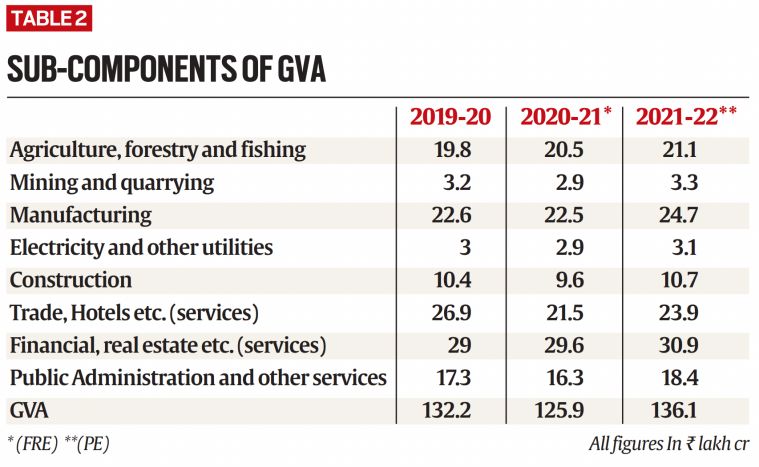

Sub-components of GDP (Source: MoSPI) Sub-components of GVA. (Source: MoSPI)

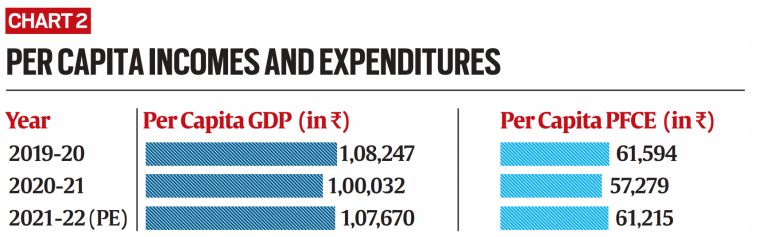

Sub-components of GVA. (Source: MoSPI) Per capita incomes and expenditures (Source: MoSPI)

Per capita incomes and expenditures (Source: MoSPI)

Udit Misra is Senior Associate Editor at The Indian Express. Misra has reported on the Indian economy and policy landscape for the past two decades. He holds a Master’s degree in Economics from the Delhi School of Economics and is a Chevening South Asia Journalism Fellow from the University of Westminster. Misra is known for explanatory journalism and is a trusted voice among readers not just for simplifying complex economic concepts but also making sense of economic news both in India and abroad. Professional Focus He writes three regular columns for the publication. ExplainSpeaking: A weekly explanatory column that answers the most important questions surrounding the economic and policy developments. GDP (Graphs, Data, Perspectives): Another weekly column that uses interesting charts and data to provide perspective on an issue dominating the news during the week. Book, Line & Thinker: A fortnightly column that for reviewing books, both new and old. Recent Notable Articles (Late 2025) His recent work focuses heavily on the weakening Indian Rupee, the global impact of U.S. economic policy under Donald Trump, and long-term domestic growth projections: Currency and Macroeconomics: "GDP: Anatomy of rupee weakness against the dollar" (Dec 19, 2025) — Investigating why the Rupee remains weak despite India's status as a fast-growing economy. "GDP: Amid the rupee's fall, how investors are shunning the Indian economy" (Dec 5, 2025). "Nobel Prize in Economic Sciences 2025: How the winners explained economic growth" (Oct 13, 2025). Global Geopolitics and Trade: "Has the US already lost to China? Trump's policies and the shifting global order" (Dec 8, 2025). "The Great Sanctions Hack: Why economic sanctions don't work the way we expect" (Nov 23, 2025) — Based on former RBI Governor Urjit Patel's new book. "ExplainSpeaking: How Trump's tariffs have run into an affordability crisis" (Nov 20, 2025). Domestic Policy and Data: "GDP: New labour codes and opportunity for India's weakest states" (Nov 28, 2025). "ExplainSpeaking | Piyush Goyal says India will be a $30 trillion economy in 25 years: Decoding the projections" (Oct 30, 2025) — A critical look at the feasibility of high-growth targets. "GDP: Examining latest GST collections, and where different states stand" (Nov 7, 2025). International Economic Comparisons: "GDP: What ails Germany, world's third-largest economy, and how it could grow" (Nov 14, 2025). "On the loss of Europe's competitive edge" (Oct 17, 2025). Signature Style Udit Misra is known his calm, data-driven, explanation-first economics journalism. He avoids ideological posturing, and writes with the aim of raising the standard of public discourse by providing readers with clarity and understanding of the ground realities. You can follow him on X (formerly Twitter) at @ieuditmisra ... Read More