On May 6, India and the UK concluded a landmark Free Trade Agreement (FTA), marked as a historic milestone by Prime Minister Narendra Modi. The deal grants India zero-duty access to all industrial goods and eliminates import tariffs on over 99.3 per cent of animal products, 99.8 per cent of vegetable/oil products, and 99.7 per cent processed foods. Currently, the UK imports goods worth $815.5 billion, primarily from countries like China (12 per cent, amounting to $99 billion), the US (11 per cent, amounting to $92 billion), and Germany (9 per cent, amounting to $76.2 billion). India is the 12th largest trading partner of the UK, but with a meagre 1.8 per cent ($15.3 billion) share in goods imported to the country. The UK exports goods worth $512.9 billion, mainly to the US ($71.3 billion), China ($46.4 billion) and Germany ($38.8 billion).

As of 2024, the India-UK total trade in goods was $23.3 billion, $8.06 billion of which was exports to India. The export basket largely comprises pearls, nuclear reactors, spirits, and vehicles, while the imports from India are machinery, mineral fuels, pharmaceuticals, apparel and footwear. The FTA has set an ambitious target of taking the trade partnership to $120 billion by 2030.

But to make this happen, India needs to stitch several loose ends in its T&A value chain, especially in designing high-value apparel products for the UK market.

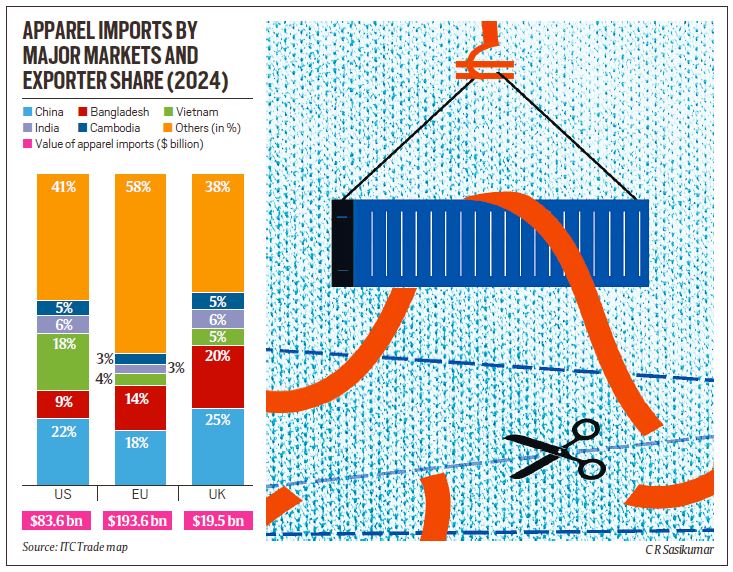

Currently, the UK imports T&A valued at $26.9 billion, of which apparel imports are $19.6 billion (72.8 per cent). The country’s apparel imports are primarily from China (25 per cent share, $4.9 billion), followed by Bangladesh (20 per cent, $3.9 billion). India has a meagre 6 per cent ($1.19 billion) share. Before the FTA, the UK imposed average tariffs of around 11-12 per cent on apparel from major importing countries. After the FTA, India will get preferential treatment with zero tariff entry — this can be a game changer for it vis-à-vis its competitors. To take advantage of this, we need to set a few things in order in the T&A value chain.

India’s T&A sector has three structural challenges. The first is its fragmented manufacturing base, with MSMEs operating in silos across states. Second, is the disjointed value chain. Cotton is grown in Gujarat and Maharashtra, yarn is spun in Tamil Nadu, fabric is processed in other parts of the country and garments are stitched at several places across the country. This geographical dispersion raises the costs of logistics and causes delays — the time from order to delivery is 63 days compared to 50 days in Bangladesh (BGMEA, 2022). Third, India’s policies around manmade fibres (MMF) lag global preferences hampered by an inverted GST structure and restrictive quality norms.

To address these issues, India must move swiftly on three fronts —policy, practices, and products — to realign its T&A sector with global market demands. On the policy front, the first priority is the swift operationalisation of PM MITRA parks, particularly in Navsari in Gujarat and Virudhunagar in Tamil Nadu, focused on exports. Simplification, consolidation, and elimination of compliance-heavy processes for exporters is a low-hanging fruit. Rationalising the inverted GST duty structure in MMF textiles is another immediate requirement. Currently, fibre inputs are taxed higher than the finished products, making Indian MMF garments globally uncompetitive. Building on the momentum of the India-UK FTA, India must put its T&A sector at the forefront in trade negotiations with the EU and the US, the biggest apparel importers (See graphics). EU imports $193.6 billion worth of apparel — competitors to India like Bangladesh and Vietnam enjoy duty-free access. Similarly, the US ($83.6 billion), presents a rare window of opportunity, having effectively eliminated Chinese dominance (22 per cent share) through the imposition of high reciprocal tariffs. Securing zero-duty access to these high-value markets can be a boon for India’s T&A sector.

In terms of practices, India must work to match up to global fashion aesthetics. Compliance is another area that requires attention. For example, with the EU implementing the Corporate Sustainability Due Diligence Directive (CSDDD) by 2029, Indian suppliers will need to embed ESG compliance, traceability and green audits in their supply chains. Finally, India must scale up towards value-added products like activewear, athleisure and technical textiles, which are dominated by MMFs. Indian firms also need to invest in functional and performance fabrics and develop capabilities to plug into global retail supply chains.

It is interesting to reflect on the irony of history. Once the heart of global T&A industry, the UK, with mills in Lancashire and James Hargreaves’ Spinning Jenny, was the birthplace of the Industrial Revolution, which dismantled India’s traditional spinning hubs. Today, in a reversal of sorts, India could be a major supplier of T&A to the UK.

The India-UK FTA also offers a timely blueprint for the ongoing trade negotiations with the US and the EU. But deals alone won’t suffice. We must re-imagine India’s textile future through integrated hubs, modern manufacturing, compliant supply chains, and demand-driven exports. The opportunity is massive, but so is the urgency. As the saying goes, a stitch in time saves nine and for India’s textile sector, this is that critical stitch.

Gulati is distinguished professor, Rao is senior fellow and Jain is research assistant at ICRIER. Views are personal