Possibly the most fundamental policy debate around India’s economy is about the nature of the economic slowdown. Correctly diagnosing the root cause for India’s anaemic growth rate in the recent past is critical to finding the right policy solutions.

The key question is: Is India’s growth rate being held back due to weak consumer demand or should we blame inadequate supply for being a drag?

A quick, albeit incorrect, way would be to look at any one sector or the other and arrive at a conclusion. For example, many who argue that India’s economic slowdown is not because of weak demand, and rather due to supply bottlenecks while pointing to carmakers struggling to meet demand owing to a global chip shortage. Others could counter it by looking at some other variable, say the box office sales, and argue that consumer demand is still weak.

Instead of picking and choosing sectors and industries, a more robust way would be to look at the official data for Gross Domestic Product, which is the monetary measure of the country’s total output.

The key variable to track within the GDP table is the Private Final Consumption Expenditure (PFCE). A look at how this variable has grown over the years should give us a decent understanding of whether India suffers from weak consumer demand.

What is PFCE and what is its significance?

The GDP is calculated by capturing the total expenditures of different components of the economy. So it adds up the expenditure by private individuals (PFCE), by the businesses investing money to ramp up production (Gross Fixed Capital Formation or GFCF), and all the spending by the government (Government Final Consumption Expenditure or GFCE).

Story continues below this ad

In India, the PFCE accounts for 55%-56% of all national GDP in a year and is, quite obviously, the biggest driver of economic growth.

But apart from its direct influence of 55%, it also indirectly influences the next biggest driver of India’s GDP — the Gross Fixed Capital Formation (GFCF). The GFCF is nothing but a measure of the money spent by businesses when they make investments, and it accounts for 33% of all GDP.

It is crucial to understand the economic logic that links these two biggest drivers of economic growth which together account for 88% to 89% of all GDP in India.

If consumer demand slows down, it robs the businesses of any incentive to boost productive capacities by making fresh investments. More precisely, just boosting investments — without regard for demand — will not make sense.

Story continues below this ad

The tremendously weighty role of private consumer demand in boosting India’s GDP makes it the most important factor determining India’s economic fortunes.

The third driver of GDP is government spending (GFCE), and it accounts for 10%-11% of all GDP. It should typically be counter-cyclical. In other words, when the rest of the economy is doing well — consumers are demanding lots of goods and businesses are investing in new capacities to furnish such demand — the government should try to limit its spending in such a manner that it does not hurt (or “crowd out”) private sector firms from accessing credit and markets.

But when consumer demand is weak, and firms are holding back (justifiably) from making fresh investments, the government should ramp up its spending to jump-start the economy and, hopefully, “crowd in” the private sector in the growth process.

The fourth engine — net exports or the net effect of India’s demand for imports and the Rest of the World’s demand for our products (exports) — is quite small in India’s case.

Story continues below this ad

How has consumer demand grown over the years?

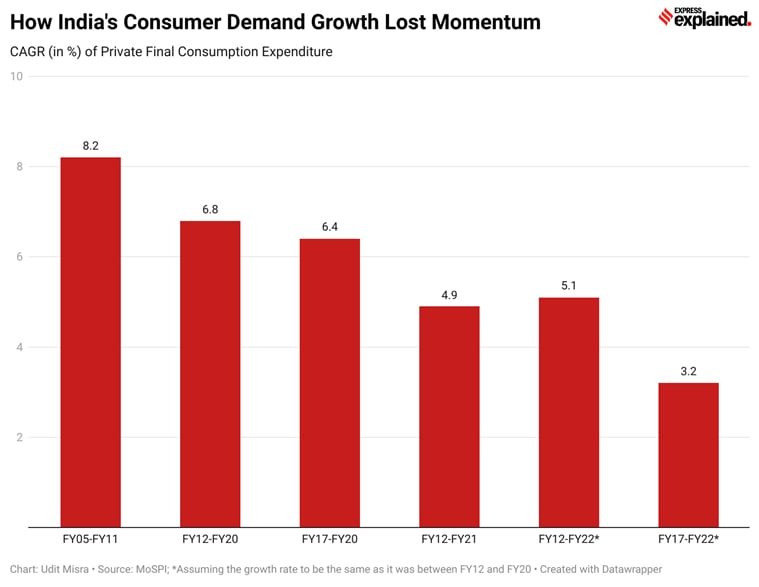

Given the overwhelmingly dominant role of private consumption demand in determining India’s economic growth in any year, it is instructive to look at how PFCE has grown in the recent past (see bar graph above).

The graph maps the last two GDP data series — one based on 2004-05 prices and the second based on 2011-12 prices.

As can be seen, private consumption expenditure grew at an annual rate of 8.2% between 2004-05 (Financial Year 2005 or FY05) and 2011-12.

Then, between FY12 and FY20 (that is, just before Covid hit India), its annual growth slowed down to 6.8%. In fact, if one further zooms into the years FY17 (after which India’s GDP growth rate started decelerating sharply) and FY20, the PFCE annual growth rate had slowed to 6.4%.

Story continues below this ad

Then came Covid-induced lockdowns in FY21 and they destroyed the already weakening demand. If we include FY21 as well, then the PFCE growth rate since FY12 falls to below 5% per annum.

What about the current year?

Of course, in FY22, the current financial year, the Indian economy is expected to register a recovery. Even if we assume that at the end of the current financial year, PFCE would grow at the same rate — 6.8% — that it had in the eight years before Covid, the FY12 to FY22 annual growth rate would barely rise above 5%.

But what is most revealing is if one forecasts the growth rate between FY17 and FY22 based on the same assumption; such a calculation throws up an annual growth rate of just 3.2%.

Comparing this 3.2% annual growth rate in private consumption expenditure in the past five years with the preceding years, especially the 8.2% annual growth rate during FY05 and FY11, which was the best phase of GDP growth in India’s history, shows how India’s consumer demand lost its growth momentum.

Story continues below this ad

What is the implication?

The most important implication of weak consumer demand is that investments by corporations are unlikely to pick up in a hurry. They are expected to remain subdued for the coming year or two as indeed they were in the years preceding the pandemic despite historic cuts in corporate tax rates in 2019. For instance, GFCF grew by just 3.9% every year between FY12 and FY20. It grew by 10.9% per annum between FY05 and FY11.

Still, does India have a supply problem?

A good measure of whether India has inadequate supply capacity or not is the rate of capacity utilisation. The data from repeated RBI’s OBICUS (Order Books, Inventories and Capacity Utilisation Survey) show how capacity utilisation has struggled to breach the 75% mark. Clearly, firms have been working far below their full capacity for several years now.

Of course, Covid disruptions have created several bottlenecks or broken supply chains, say, due to shortage of labour etc., and this is reflected in delays and price inflation.

But, as the analysis above shows, the truly substantive issue holding back India’s growth — and this holds true for the period before Covid as well — is the weak growth in consumer demand. Unless this variable improves sharply, India’s GDP growth will fail to achieve its potential.

Stay safe,

Udit

Source: MoSPI

Source: MoSPI