Journalism of Courage

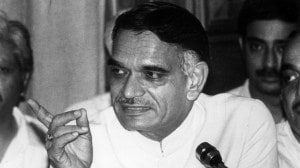

At a time when bankers across the world are being termed as ‘London Whale’,hedge-fund sharks and various other deadly creatures,Indian financial system remains intact despite its “boring banking” tag,industry leader Deepak Parekh said today.

Noting that the regulation of Indian financial system has been appreciated globally and the robustness of banking system here is very much intact,Parekh said even most of the restructured loans are not stressed because of poor credit quality,but due to “prevalent policy uncertainties”.

Speaking at Motilal Oswal Annual Global Investor Conference here,the eminent banker and financial services giant HDFC Chairman said a rock-bottom level of investment cycle in the country has indeed taken a toll on banking sector.

But,India has got far too pre-occupied with its “woes on slowing GDP growth,policy paralysis,inability of the government to push reforms; and investor confidence being shaken due to GAAR and other tax uncertainties.”

“In the process,we seem to have forgotten that the key fundamentals of the economy are very much intact in India,” he said,while listing out factors like a young population,growing middle class,better job opportunities,rising disposable incomes and a high household savings rate.

Parekh said banks are taking unprecedented beating globally amid issues like subprime crisis,collapse of financial institutions,Eurozone debt crisis,rate rigging scandal and failures to prevent money laundering.

“And,of course,the London Whale,hedge-fund sharks and heaven knows what other deadly creatures are lurking in the financial world!” he said in a lighter vein.

On the other hand,he said,Indian banking has been fairly isolated from this chaos,in part because it “was never as sophisticated or complicated as that of the Western world.”

“To my mind,the winning strategy for banks in India is ‘Basic Banking Model’ – what is otherwise known as ‘boring banking’. There is enough of retail business potential for all existing banks,new banks (as and when fresh licences are given),NBFCs and microfinance companies and other players,” he said.

Parekh said there are various factors that will continue to drive the Indian economy and consequently the Indian financial sector. “While investor or business confidence has taken a beating in the recent period,consumer confidence has continued to remain robust,” he said.

Parekh has been at the forefront of top industry leaders voicing their concerns over a slow pace of economic reforms and growing perception of policy paralysis in recent months.

He further said that banking,the world over,works on the principles of trust and confidence and in the recent period and both have reached a record low.

“Greed has trampled over trust,respect and legality,” he said,while recalling a new word coined recently,’Banksters’ — implying that bankers were ready to dethrone gangsters with their despicable behaviour,” Parekh said.

“Today,there are no longer any ‘Wall Street Stars’ or celebrated champions in the financial industry,” he added.

Parekh said leadership plays an important role in shaping the culture of a bank,but banks have grown so large and the key question arises whether bank CEOs are able to keep track of what their traders or employees are up to.

“Thus,the recommendation of ring-fencing retail banking from investment banking is becoming more compelling now – at least amongst the regulators. The solution to banking scandals cannot be financial penalties,resignations and tighter regulation,” he said.

In the context of Indian banking system,Parekh said public sector banks have a disproportionately larger share of the NPAs compared to private sector banks and “a distinct trend seen in the banking sector,particularly with public sector banks is that the concentration risk has increased as many banks have high exposures to the same few groups.”

Identifying retail focus as a key for better performance,Parekh said that consumer credit penetration in India is extremely low compared to countries like China,Japan,Singapore and Malaysia.

Asking investors to take a “big picture” view,Parekh said banking will see exponential growth by the end of this decade.

“Mortgages are expected to cross Rs 40 trillion by 2020. With a growing bankable population,by 2020,the number of bank branches is expected to double from 2010 levels. This means 70,000 more branches will be added. Similarly,there will be a five-fold increase in the number of ATMs.

“Wealth management is also expected to grow by 10 times. So,the prospects are very promising. Private equity has also seen a healthy growth in India,” he said.

“India still has an estimated USD 20 billion of dry powder,that is funds committed but not invested. However,much greater effort especially in terms of a more conducive regulatory environment will be needed to increase penetration of insurance.

“In the recent period,both the mutual fund industry and life insurance sector have unfortunately,seen de-growth. This is partly attributable to the many regulatory changes,” Parekh said,while admitting that ULIPs were indeed being mis-sold.

Still,the life insurance industry has been saddled with a number of new regulations and frequent changes made the operating environment difficult,he said,while terming that it has become a case of ‘a regulation a day keeps business away!’

“In the future,I see more mergers taking place – there will be fewer,but larger players” in the insurance space,Parekh said,while expressing hope about growth in mutual fund industry as well on the back of recent measures taken by Sebi.

“So on the whole,Indian financial system will continue to grow and the future outlook remains encouraging,” he said.

Listing out the concerns and challenges,Parekh said that one of the risks is that of regulatory overbearance.

“Admittedly,today the job of a financial regulator is extremely challenging and while there is a need to be vigilant,it is also important for the regulators not to be too prescriptive and let market forces work.

“Indian financial conglomerates have additional challenge of having to deal with multiple regulators in the financial sector. As mentioned earlier,frequent regulatory changes are unwarranted and the diktat on where and how and at what rate to lend at is not good for the financial system,” he said.

Giving example of the recent regulatory changes is in the priority sector norms,Parekh said that agriculture as a percentage of GDP over the years has come down significantly,but the mandated 18 per cent priority sector limit continues.

At the same time,indirect lending to housing finance firms and most NBFCs are no longer priority sector lending.

“To my mind it is more important that credit be made available and it does not always have to be that bank provides credit directly. I do not buy the ‘lazy banking’ argument!

“If infrastructure financing is a national priority,then why is not it included as priority sector lending?,” he asked.

He also expressed concern about the regulators’ perception on NBFCs.

“It appears that there is an attempt to slowly and steadily curb activities of NBFCs by clamping down on their ability to raise resources. The regulators don’t want NBFCs raising retail deposits,” he said.

However,he admitted that some regulatory concerns on NBFCs were valid,such as NBFCs excessively funding promoters who pledged their shares or the rapid rise in gold loans.

“Regulators do not seem to appreciate that there are many NBFCs that have a very good track record and have provided credit where banks have been unable or unwilling to do so.

“The question then arises is whether RBI will be willing to grant bank licenses to convert these NBFCs into banks?”

Parekh also called upon the government to ensure a conducive environment,remove policy uncertainties,hike insurance FDI cap,bring in legislation and taxation changes for Financial Holding Firms,and articulate its plan to fund PSU banks’ additional equity requirement of Rs 1.5 trillion.

He said that private sector banks should be able to more easily meet their additional capital requirements,but it may also result in more banks having a foreign shareholding in excess of 51% per cent and consequently,complexities arising from ‘foreign owned Indian controlled’ financial entities would need to be ironed out.