© The Indian Express Pvt Ltd

Suzlon remains largely unaffected by US tariffs as it generates most of its revenue within India. Its wind turbines are also manufactured domestically. (Photo Credit: Suzlon)

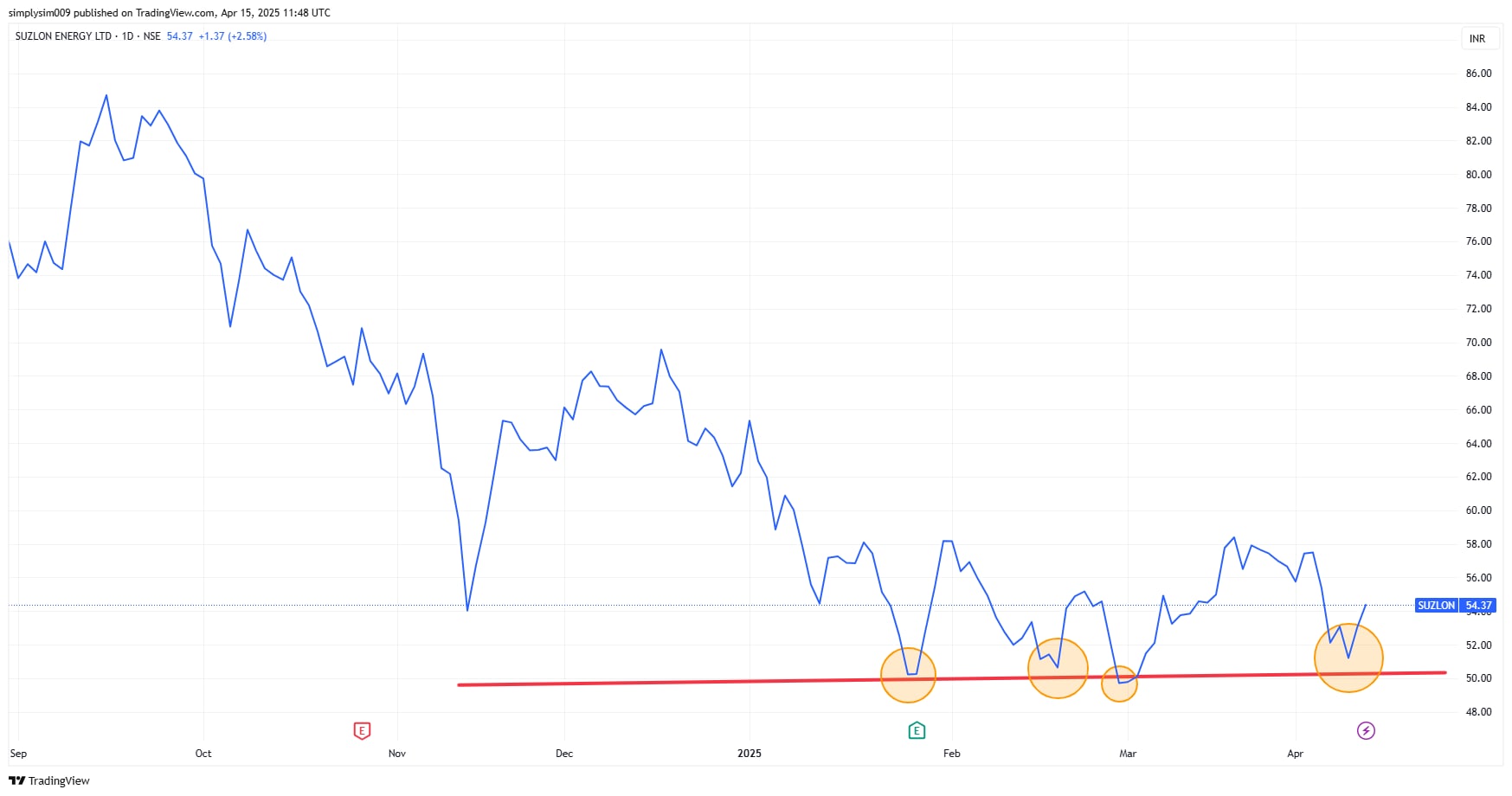

Suzlon remains largely unaffected by US tariffs as it generates most of its revenue within India. Its wind turbines are also manufactured domestically. (Photo Credit: Suzlon)Donald Trump’s recent imposition of reciprocal tariffs has rattled global stock markets, including India’s. On April 2, the US announced a 26% reciprocal tariff on Indian solar goods, only to defer it for 90 days. The announcement saw a sharp dip in renewable energy stocks, particularly in the solar sector. Even Suzlon Energy, the integrated wind energy company, saw its stock fall 7.5%. However, it continued to trade above Rs 50 as retail investors continued to buy the dip. The stock rebounded after the temporary tariff pause.

Suzlon Energy’s Stock Price Momentum from September 2024 to April 2025. (Source: Trading View)

Suzlon Energy’s Stock Price Momentum from September 2024 to April 2025. (Source: Trading View)

According to BSE shareholding data, Suzlon Energy’s retail ownership rose to 25.12% Q4 FY25, up from 24.49% in the previous quarter. This suggests that retail investors are confident about the stock’s growth potential.

Why are investors confident in Suzlon?

Suzlon remains largely unaffected by US tariffs as it generates most of its revenue within India. Its wind turbines are also manufactured domestically.

Brokerages are bullish, maintaining a “buy” rating as the stock trades near Rs 50 price range.

Suzlon’s five growth drivers — order book, lower competitive intensity, market leadership in India’s wind energy market, favourable government policies, and the 2030 target of 100 GW wind energy — remain intact.

The tariffs could make solar energy costly, as India relies heavily on imports for solar equipment. Conversely, India might lower tariffs on Chinese solar imports to reduce solar energy costs.

Suzlon, with over 85% of its turbine components sourced domestically, is less dependent on imports. Its order book mostly comprises domestic orders, unlike its counterparts, such as Waaree Renewable Technologies, which also exports solar modules to the United States.

Suzlon’s long-term growth strategy is to export wind turbines to Europe. While its operations and future growth strategy won’t face direct impact from the US tariffs, a tariff-led global slowdown could delay long-term expansion. For now, Suzlon’s domestic order book remains robust.

Suzlon Energy’s last updated order book stood at 5,622 MW — up from 5,523 MW as of January 28, 2025 — even after the cancellation of two orders. Most of its orders have a quick turnaround as they are non-engineering, procurement, and construction (EPC).

A key win was a third repeat order from Jindal Renewables for 204.75 MW, taking their total orders to 907.2 MW.

This has made brokerages bullish on Suzlon’s revenue and earnings growth. Geojit Financial Services, in its 24 March 2025 report, forecasts the Wind Turbine Generator (WTG) segment’s profitability to improve due to a better product mix. It expects Suzlon’s PAT to grow at a compounded annual growth rate (CAGR) of 30% in FY25- 27. While it is lower than the last three year’s CAGR of 45%, it still signals strong double-digit growth.

Morgan Stanley expects India’s 2030 target of 100GW in wind energy to increase Suzlon’s order book to 32GW and increase its market share by 35-40% by FY27 from the current 31%.

But what after FY27?

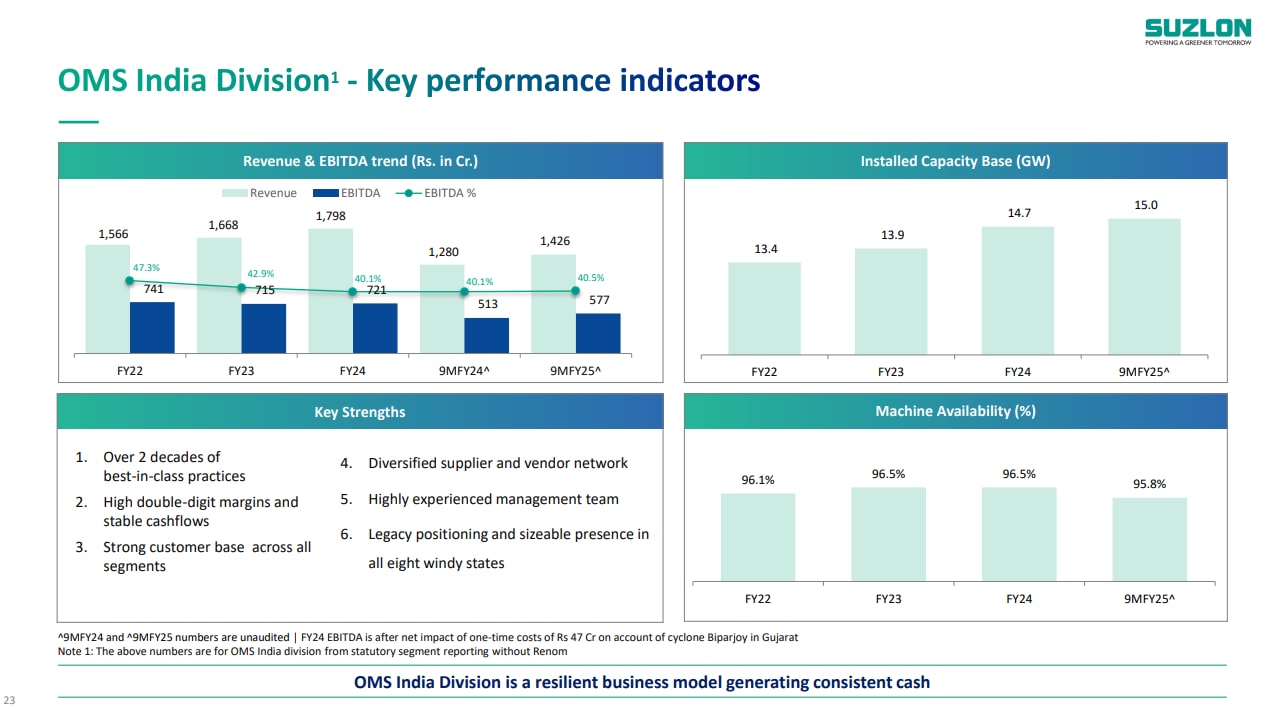

Suzlon’s dual-revenue model supports sustainable earnings: Wind Turbine Generators (WTG) account for 70% of revenue, while Operations and Maintenance Services (OMS) account for 70% of EBITDA and provide long-term, annuity-like cash flows. The OMS segment is bolstered by commercial clients like Jindal Renewable, which brings significant O&M opportunities.

Every wind turbine Suzlon sells brings in 25 years of OMS revenue and grows its OMS fee by 4-5% annually. Moreover, the company has acquired Renom to provide OMS to non-Suzlon wind turbines. So far, Suzlon’s OMS is serving 15 GW of installed capacity, and Renom will add another 3 GW of wind capacity.

Suzlon Energy’s OMS India Division Financial Performance (Source: Suzlon Energy’s Q3 FY25 earnings presentation)

Suzlon Energy’s OMS India Division Financial Performance (Source: Suzlon Energy’s Q3 FY25 earnings presentation)

The wind energy business is cyclical and depends heavily on government incentives to encourage companies and utilities to install wind turbines. Periods of downturn can prove detrimental to the company’s earnings. Such cyclical companies should have lower debt on their balance sheet to maintain financial flexibility across cycles.

During the 2023 turnaround, Suzlon Energy became debt-free by raising equity capital to repay debt.

While cyclicality could drive its sales and stock price, the stable cash flows of OMS could assure investors that the company can stay profitable even in a downturn.

Is Suzlon better than its peers?

Suzlon’s main competitor, Inox Wind, has a short-term debt of Rs 3,746 crore, making it riskier in a volatile industry. Suzlon’s relatively clean balance sheet gives it a financial edge.

Suzlon also competes with low-cost solar energy. However, Firm and Dispatchable Renewable Energy (FDRE) projects allow for the development of hybrid projects covering both wind and solar, thereby making Suzlon’s biggest competitor (solar energy) its ally. The mix of wind and solar energy can make renewable energy more dependable during the off-season.

Industry challenges are a major growth deterrent

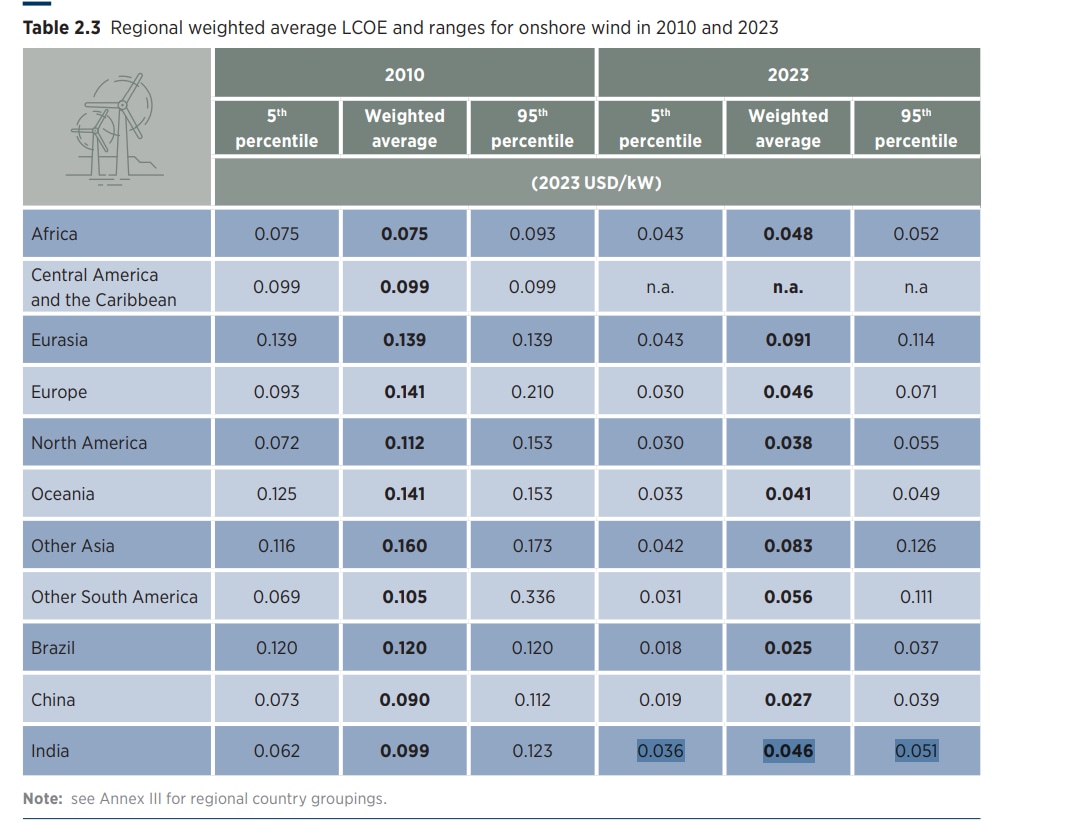

The renewable power sector is seeing a cyclical upturn. Wind energy’s Levelized Cost of Energy (LCoE) has significantly reduced and is competitive with fossil fuel power plants because of government incentives. If it weren’t for the government’s mandatory renewable purchase obligations (RPOs), utilities wouldn’t have purchased wind energy.

Moreover, India is still behind Brazil, China, North America, and Oceania in terms of lower LCoE. To compete globally, Suzlon must lower its LCoE before scaling up exports.

Onshore Wind’s Levelized Cost of Energy in 2010 and 2023 (Source: International Renewable Energy Agency 2023 Report)

Onshore Wind’s Levelized Cost of Energy in 2010 and 2023 (Source: International Renewable Energy Agency 2023 Report)

Is Suzlon a good buy at its current valuation?

Suzlon’s conservative approach to expansion makes it an attractive medium-term investment owning for the next two years or so. It has a strong order book, stable cash flow streams, and cyclicality. However, visibility beyond FY27 is limited because of its order books.

The company’s order book is currently driven by a 100% Inter-State Transmission System (ISTS) waiver for 25 years on projects completed till 30 June 2025, 75% for projects completed next year, and 50% for the third year. It remains to be seen what happens after the end of ISTS.

Moreover, new renewable power plants are growing at a faster rate than the battery storage and transmission infrastructure. If the renewable energy generated cannot be passed on to consumers, the projects may not run at full capacity, delaying new orders.

Suzlon stock has already completed its multibagger rally of 800-900% in the last two years. This rally has inflated the stock’s valuation to a 62.59x price-to-earnings ratio (P/E).

Brokerage Price Target for Suzlon Energy (Updated in March 2025)

|

Brokerage House

|

Suzlon Energy Target Price in Rs (March 2025)

|

Analyst Rating

|

Previous Target in Rs

|

|

Motilal Oswal Financial Services

|

70

|

Buy

|

Initiated Coverage in 2025

|

|

Geojit Financial Services

|

71

|

Buy

|

68

|

|

Morgan Stanley

|

71

|

Buy

|

78

|

|

JM Financial

|

71

|

Buy

|

80

|

|

Nuvama Institutional Equities

|

60

|

Buy

|

64

|

|

Ventura Securities

|

No Update

|

–

|

50

|

Source: Brokerage reports

Given that the next two years could see strong double-digit growth, Motilal Oswal Financial Services has set a price target of Rs 70, considering a target PE ratio of 34x on its December 2026 earnings per share (EPS) estimate for Suzlon. A Rs 71 price target represents a 30% upside potential from the current trading price of Rs 54.5.

Suzlon is increasing its manufacturing capacity to 4.5GW from 3.15GW. Any signs of earnings growth potential through new order wins or the execution of major EPC contracts could drive Suzlon’s share price.

In summary

Suzlon Energy has the fundamentals to withstand a downturn. While short-term volatility may arise, particularly in July, when the ISTS waiver reduces (July 1) and the 90-day tariff pause ends (July 8), its EPS growth prospects could drive the rally over the next two years.

It would be interesting to see how India’s renewable energy focus pans out for Suzlon in the next two to five years.

Note: We have relied on data from http://www.Screener.in throughout this article. Only in cases where the data was not available have we used an alternate, but widely used and accepted source of information.

Puja Tayal is a financial writer with over 17 years of experience in the field of fundamental research.

Disclosure: The writer and her dependents do hold the stocks discussed in this article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.