© The Indian Express Pvt Ltd

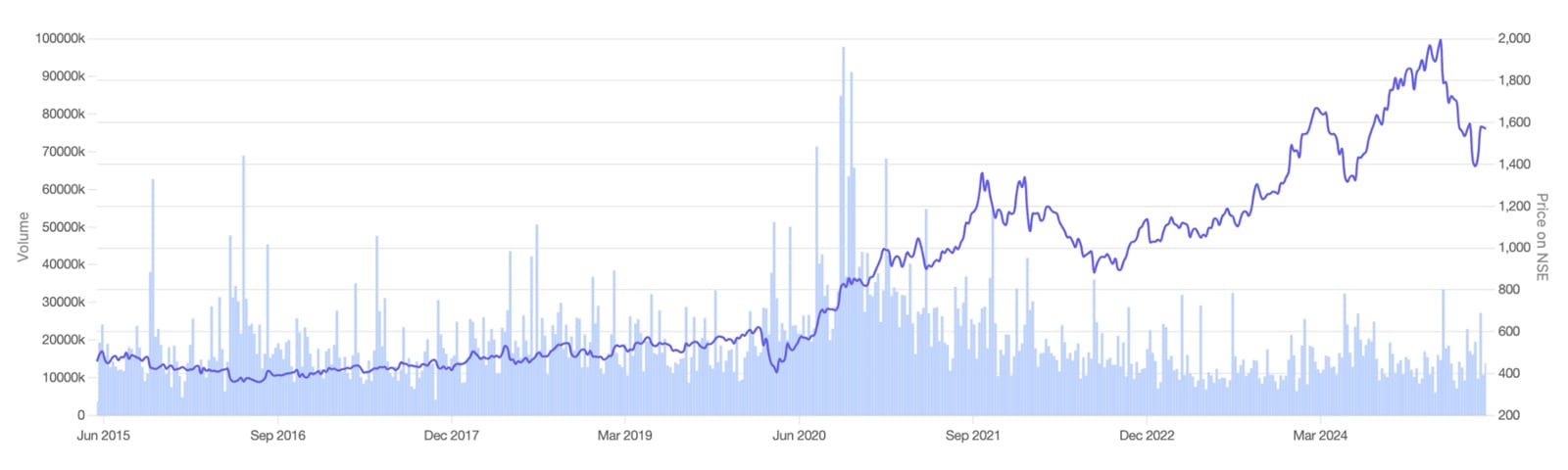

From under Rs 500 in early 2020, HCL Tech surged to touch Rs 2,000 by January 2025. (Source: File)

From under Rs 500 in early 2020, HCL Tech surged to touch Rs 2,000 by January 2025. (Source: File)For a long time, HCL Tech was the quiet IT stock in investors’ portfolios.

Between 2015 and 2020, it mostly moved sideways, stuck in the Rs 450-550 range. For five straight years, the stock barely budged, even as peers like Infosys and TCS saw more action.

But post-Covid, the story changed.

From under Rs 500 in early 2020, HCL Tech surged to touch Rs 2,000 by January 2025. That’s a 4x move in less than five years, translating to a remarkable 32% CAGR.

Then came the pullback.

Over the past few months, as global tech budgets softened and investor excitement around AI and digital deals gave way to realism, the stock slipped back to the Rs 1,600 range. It was not a crash, but enough to make investors pause and ask: Was that rally overdone, or is this correction a chance to get in before the next leg?

HCL Tech continues to do a lot right, including deal wins, margin protection, bets on AI and cloud, and a strong balance sheet. However, the IT landscape is shifting fast, and staying relevant means more than just execution; it requires reinvention

So, is HCL still the reliable compounder it proved to be post-Covid, or is its best phase already behind it? Let’s examine the business strategy, recent financials, industry trends, and whether there’s still enough fuel left in the tank for long-term investors.

Share Price Movement of HCL Tech Ltd. (Source: Screener.in)

Share Price Movement of HCL Tech Ltd. (Source: Screener.in)

To understand where HCL Tech might be headed, we first need to understand where its growth comes from and how it’s evolving.

HCL has three main business segments: IT and Business Services (ITBS), Engineering and R&D Services (ERS), and Software and Products (also called Mode 3).

1. IT & Business Services: The bread-and-butter

This is the largest part of HCL’s business, roughly 70% of total revenue. It includes traditional IT services like cloud migration, app modernisation, data centre management, and digital workplace solutions. While this segment doesn’t grab headlines, it generates stable, recurring revenue and serves as the cash engine for the company.

Interestingly, this is also where a lot of the AI-led cost efficiency work is happening. Clients aren’t necessarily spending more, but they’re asking HCL to help them spend smarter. That’s why this segment is under constant margin pressure, even as deal sizes remain large.

2. Engineering & R&D (ERS): The differentiator

ERS accounts for around 16-17% of revenue, and it’s one of the more exciting pieces of HCL’s puzzle. This business includes product engineering for clients across auto, aerospace, telecom, and manufacturing. As devices get smarter and connectivity becomes universal, companies need partners who can handle embedded software, electronics, and complex engineering.

HCL is among the top global players in ER&D services, and this segment is a big reason why the company wins deals in Germany, Japan, and other advanced manufacturing markets. However, in the last couple of quarters, ER&D has seen some pressure, especially in the automotive vertical, where clients have pulled back on spending.

Still, over a 3-5 year horizon, this segment gives HCL a clear differentiator compared to many IT services peers who lack deep engineering chops.

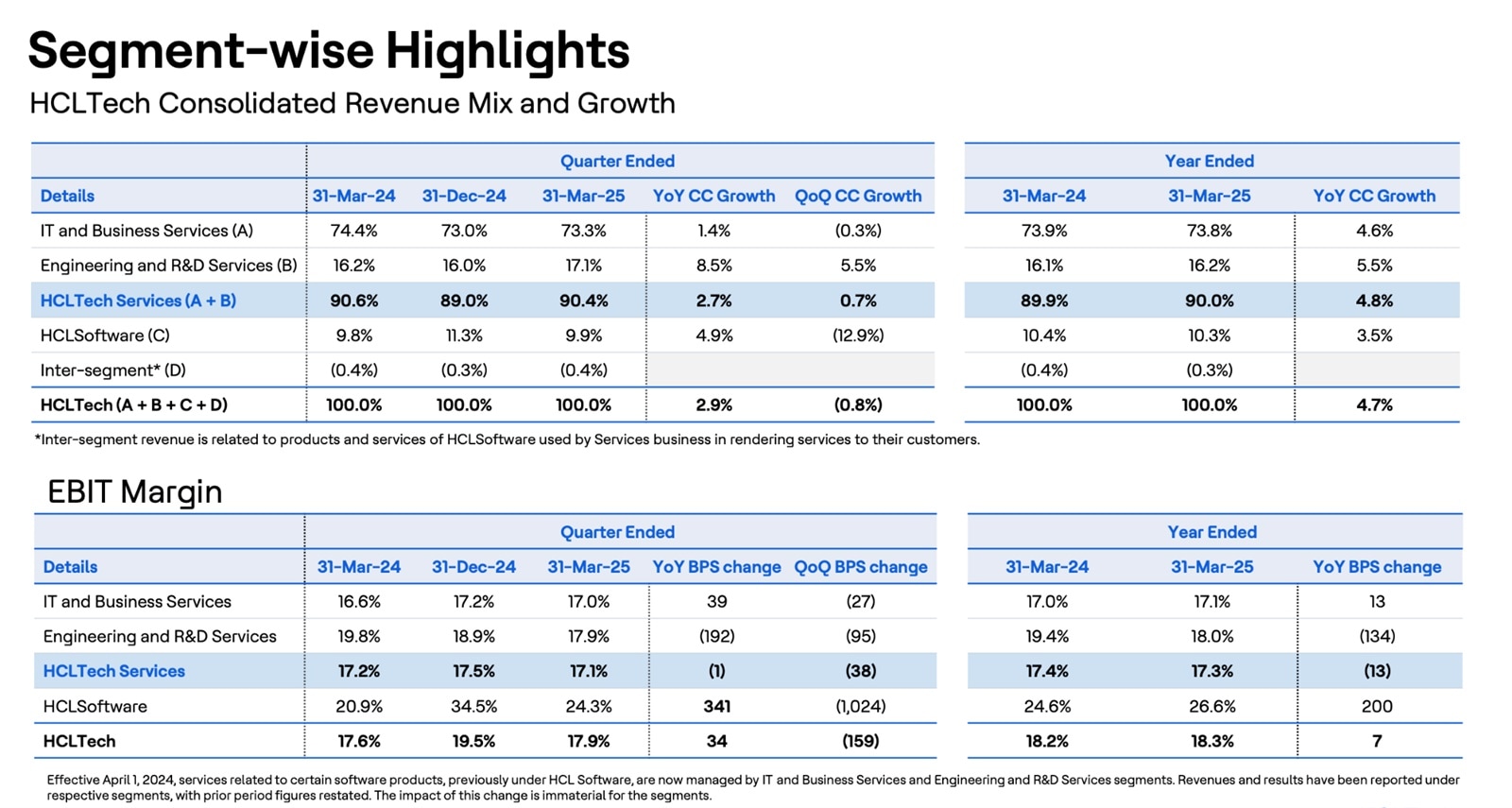

HCL Tech’s Segment-wise Highlights. (Source: Quarterly Report Mar 25)

HCL Tech’s Segment-wise Highlights. (Source: Quarterly Report Mar 25)

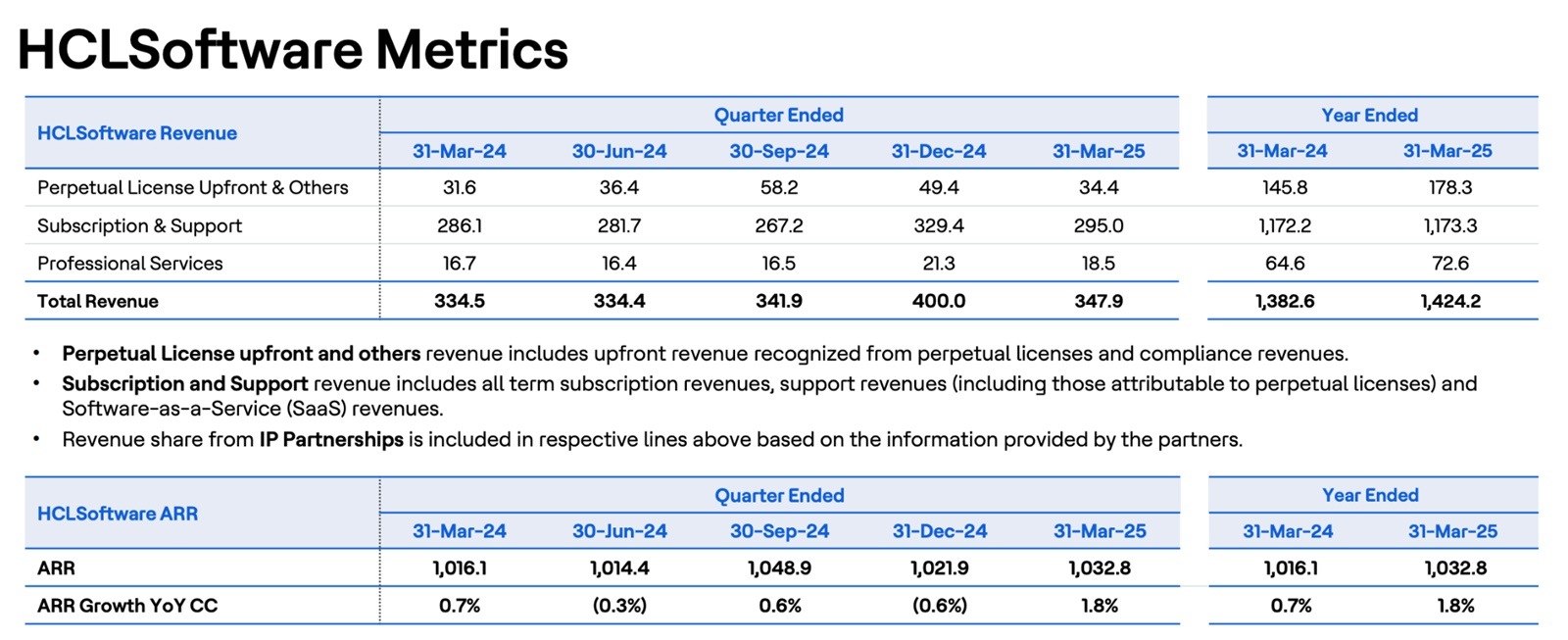

3. Software & Products (Mode 3): The wild card

HCL’s intellectual property business is its own software platforms, tools, and licensed products. It’s smaller, contributing just under 13% of revenue, but more profitable. The unit includes products like DRYiCE (automation), BigFix (endpoint security), and a variety of IPs acquired from IBM over the years.

The big story here is the margin. This business runs at a 25-30% EBIT margin, much higher than the core IT services margin. But growth has been patchy, especially recently. In fact, HCL’s latest quarter results indicated that product revenue declined quarter-over-quarter, dragged down by weak license renewals and slower enterprise spending.

That said, HCL has been launching AI-powered products and platform-led offerings in this space, hoping to revive growth and make it a bigger driver in the future.

HCL Software Key Metrics. (Source: Quarterly Report Mar 25)

HCL Software Key Metrics. (Source: Quarterly Report Mar 25)

Over 65% of HCL Tech’s revenue comes from the Americas, mostly the United States. That’s where most of the large enterprise clients sit, and it’s also where most of the slowdown fears are centred right now, especially with tech, retail, and manufacturing clients tightening budgets.

Europe contributes around 28-30%, with strong positions in Germany, the UK, and the Nordics. HCL’s engineering services and telecom partnerships have helped it build deep client relationships in continental Europe, though macro uncertainty in the region has led to cautious client behaviour.

India and ROW (Rest of World) make up the balance, about 7%. This includes fast-growing emerging markets like APAC and the Middle East, but it still remains a small share of the overall business.

The geographic exposure gives HCL global reach but also links its fortunes closely with the US and European enterprise health. When these clients pull back like they’ve done lately, it shows up in HCL’s numbers.

HCL Tech’s Revenue Mix. (Source: Quarterly Report Mar 25)

HCL Tech’s Revenue Mix. (Source: Quarterly Report Mar 25)

One of HCL Tech’s most underrated qualities is its ability to grow wallet share within existing clients. Instead of chasing hundreds of small logos, the company has focused on deepening engagement with large, strategic clients.

As of the latest data:

This “land and expand” strategy has helped HCL maintain revenue momentum even when new client acquisition slows. Many of its large clients are now engaging HCL for multi-stack solutions, not just IT support but also engineering, cloud, cybersecurity, and AI implementation.

If there’s one trend to watch, it’s how quickly HCL can cross-sell emerging capabilities, especially generative AI tools, to these clients. That could be the next leg of revenue growth, even in a cautious spending environment.

HCL Tech’s Client Mix. (Source: Quarterly Report Mar 25)

HCL Tech’s Client Mix. (Source: Quarterly Report Mar 25)

The mood across the global IT services space right now is cautious. Discretionary tech spending remains under pressure, clients are hyper-focused on cost efficiency, and deal cycles are getting longer.

HCL Tech is no exception, but it’s holding up better than most.

In FY25, the company delivered 4.7% revenue growth in constant currency, and EBIT margins expanded to 18.3%, marking the third straight year of outperformance versus similar-sized peers. That’s no small feat in a year where many large IT players missed or revised guidance downward.

While Q4 saw a slight sequential dip in revenue (-0.8% QoQ in CC terms) due to seasonality in the software segment, the services business grew modestly (+0.7% QoQ), and deal bookings came in strong at $3 billion, the second-highest in HCL’s history. Notably, 50% of these bookings were closed in March alone, suggesting that urgency among clients remains high, especially for cost-efficiency and AI-led projects.

What does management expect ahead? A revenue growth guidance of 2-5% for FY26, with the lower end assuming further macro deterioration. That’s a sober but pragmatic stance, considering the visible slowdown in North America and verticals like BFSI and healthcare.

Still, with a robust $9.3 billion in total bookings for FY25 and a healthy pipeline across geographies and service lines, HCL is positioned to navigate this period without major damage.

Now let’s talk about the buzzword of the moment: Generative AI. While many peers are still showcasing demos, HCL seems to be deploying at scale.

In short, HCL isn’t betting on a single blockbuster AI product. Instead, it’s going horizontal, embedding AI into every layer of the enterprise tech stack. From L1 service desks for an automotive OEM to Agentic AI-led workflow automation in retail, it’s aiming for enterprise-wide integration.

Also worth noting: more than 100,000 employees have been trained on GenAI, showing that the company is not just building external solutions, but also preparing for internal transformation.

Will this AI strategy translate into material revenues soon? That’s the big unknown. But in terms of deal pipeline, AI is now a component in nearly every major RFP, and clients are actively looking for cost takeout + transformation bundles. That’s where HCL’s end-to-end delivery model and engineering DNA give it an edge.

While Infosys and TCS dominate media headlines, HCL has quietly gained ground, especially in engineering, telecom, and emerging verticals. In FY25:

However, there are clear soft spots too — Financial Services was down 1.6%, and Life Sciences declined by 3.8%, reflecting budget freezes and client-specific challenges.

Geographically, Europe and ROW saw healthy growth, but North America, which accounts for nearly 64% of revenue, was flat, impacted by a large retail programme winding down and overall spending moderation.

Still, management remains bullish on sectors like AI-powered silicon, software-defined vehicles, and cloud modernisation — areas where HCL’s deep engineering roots and platform approach can create defensible differentiation.

HCL Tech’s Services Mix and Growth. (Source: Quarterly Report Mar 25)

HCL Tech’s Services Mix and Growth. (Source: Quarterly Report Mar 25)

Project Ascend, HCL’s margin expansion programme, is doing its job. EBIT margins stayed above 18% despite salary hikes, sales investments, and currency volatility. Even though Q4 margins dropped to 17.9% (due to software seasonality and increment cycles), the full-year delivery was solid.

But here’s the catch: don’t expect further margin expansion from here. The company itself guides FY26 EBIT margin between 18% and 19%, meaning future earnings growth will have to come from top-line acceleration, not cost-cutting.

At the time of writing, HCL Tech trades in the range of Rs 1,650-1,750. Based on FY25’s reported EPS of Rs 64.09, that puts the stock at roughly 26-27x trailing earnings — a valuation that’s neither cheap nor euphoric.

Here’s the thing: HCL is no longer the undervalued underdog it was in 2020 when it traded below Rs 500. That 4x rally over five years was driven by a combination of earnings growth, multiple expansion, and the re-rating of Indian IT in general. But now, the bar is higher.

If HCL delivers on its FY26 EPS estimates of Rs 68-70, and the market continues to value it around 25x forward earnings, the stock could gradually move toward the Rs 1,750-1,850 range. Under an optimistic scenario, say EPS touches Rs 75-77 by FY27, and sentiment improves, it could stretch toward Rs 2,000+ again, albeit slowly and only if macros cooperate.

But it’s important to note: much of the re-rating is already done. For the next leg up, investors will need to see:

What could limit the upside?

Note: This is not a prediction of where the stock price could head. It’s just an if-then calculation for academic purposes.

So, is it still worth betting on?

If you’re looking for a high-beta IT stock that might double in a year, HCL Tech probably isn’t it. But if you want a steady compounder with a consistent track record, margin discipline, a clean balance sheet, and real AI execution, HCL makes a strong case.

It’s delivering 10%+ earnings growth, generating 38%+ return on capital, and paying out over 90% of profits as dividends. Not many companies offer that combination today, especially in a sector navigating uncertainty.

The rally from Rs 500 to Rs 2,000 may be behind us, but the next Rs 300-400 move could still be driven by real earnings and strategic delivery.

Bottom line: HCL Tech isn’t a sprint, it’s a marathon. The easy money may have been made, but the long-term story still looks intact. If you’re patient and okay with some short-term volatility, this might still be a stock worth holding onto or even adding to, on dips.

Note: This article relies on data from annual and industry reports. We have used our assumptions for forecasting.

Parth Parikh heads the growth and content vertical at Finsire. He holds an FRM Charter along with an MBA in Finance from Narsee Monjee Institute of Management Studies.

Disclosure: The writer and his dependents do not hold the stocks discussed in this article.

The website managers, their employees(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.