Last week, official data showed that in January, India’s retail inflation surged by 6.5%. In other words, the general price level facing the consumers in January 2023 turned out to be 6.5% higher than the price level in January 2022; this is called a year-on-year (or y-o-y) growth rate.

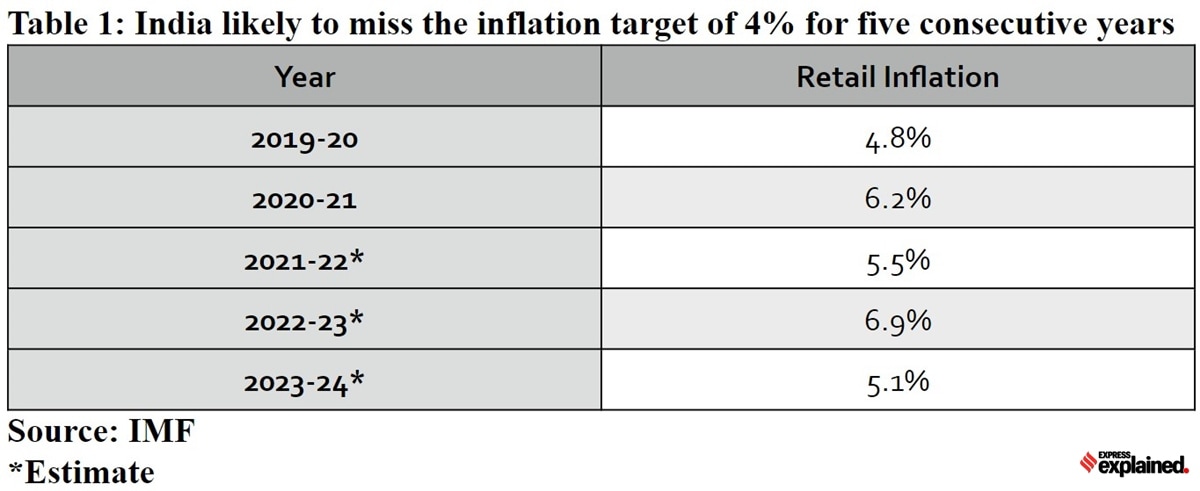

As things stand, it now looks quite likely that India’s inflation rate will be above the crucial 4% level in each of the five years of the current government’s term (see Table 1). To be sure, 4% inflation is the target level under the current monetary policy regime.

Table 1: India’s retail inflation from 2019 to 2021, and estimates from 2022-2024

Policy significance of inflation spike in January

For one, the January increase was a sharp turnaround from the deceleration in inflation that was being witnessed in the recent months. The headline retail inflation rate was 7.4% in September but since then it was fast losing steam every month and fell to 5.7% in December.

This moderation had convinced many to demand that the RBI should avoid raising interest rates — something the RBI did not do when it met on February 8.

In fact, the RBI raised the repo rate — the interest rate at which it lends money to the banking system — by 25 basis points (100 basis points make up a full percentage point). RBI raises the repo rate when it believes that inflation is not in control. Higher interest rates drag down overall demand for goods and services by making loans costlier. Lower demand is expected to cool down inflation.

The January surge was also an unexpected event — most economists and observers expected inflation to rise by just 6% — and it has renewed the apprehensions of the RBI raising the interest when it meets again in April. RBI’s Monetary Policy Committee (MPC) meets every two months to reconsider its monetary policy stance.

Story continues below this ad

Each passing jump in the interest rate, while doing its bit towards containing inflation, by design also hurts India’s economic growth. To be sure, there is a constant tradeoff between maintaining price stability (read containing inflation) and boosting growth (which hopefully creates jobs and reduces unemployment). In fact, the six-member MPC of the RBI chose to increase the repo rate in February by a split vote of 4-2. The previous review in December also witnessed a hike in repo rate with a split vote of 5-1.

Simply put, if inflation stays persistently high (‘sticky’), it would necessitate the RBI to keep raising interest rates — or, at the very least, keep them at a high level for a longer period — and, in doing so, hurt India’s economic recovery out of the twin shocks of the Covid pandemic and the Russia-Ukraine war.

One, higher food inflation. In particular, it was the cereal prices that seem to have shot up. Cereals are grains such as wheat and maize. Although, economists at Kotak Institutional Equities — Upasna Bhardwaj, Suvodeep Rakshit and Anurag Balajee — state that there “appears to be some data anomaly in the cereals index for January”. Their calculations suggest that cereal price inflation was far more modest than mentioned in the official release. In their view, it is possible that the final retail inflation rate may fall to 6.2%, instead of 6.5%.

Story continues below this ad

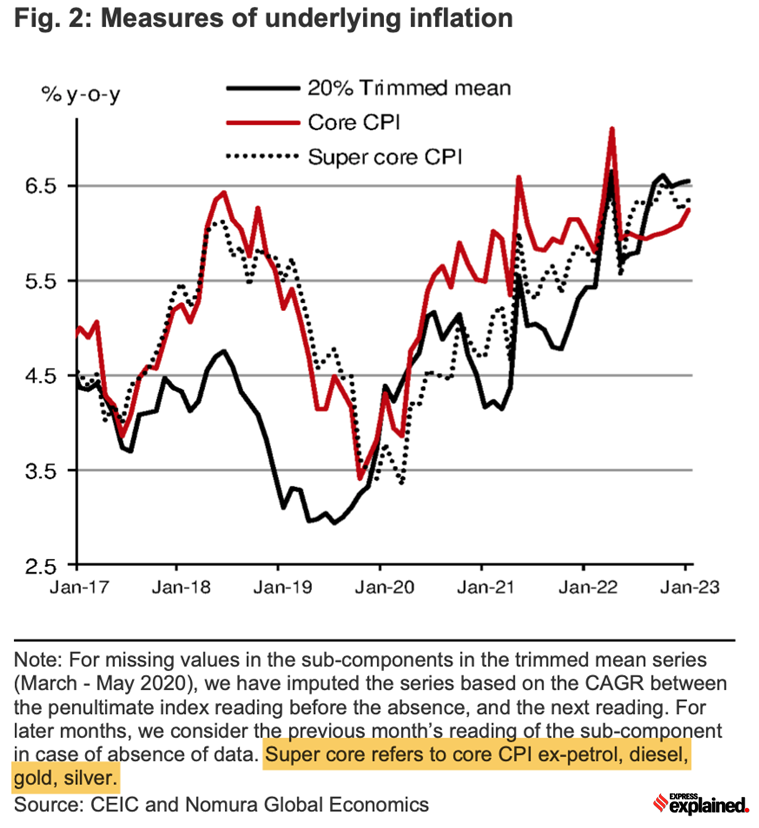

Two, core inflation has inched up. Core inflation is a measure of inflation arrived at by removing the prices of food and fuel. Since food and fuel prices fluctuate massively, often looking at core inflation provides a sense of how the broader economy is doing. Even stricter measures of core inflation such as super core inflation (calculated by Nomura Research) too has gone up in January. Super core inflation is calculated by removing gold and silver price inflation from core inflation. According to Nomura, core inflation rate has inched to 6.2% from 6.1% in December and super core inflation rate has gone up to 6.3% from 6.2% (see Chart 1).

Chart 1: Core inflation rate has inched to 6.2% from 6.1% in December

Why is India’s inflation turning out to be sticky?

Inflation being sticky essentially means that inflation is taking longer than expected to fall. Essentially, higher food and fuel prices have seeped into the broader economy and made other things costlier.

“A deeper dive into the core inflation basket suggests that firms continued to pass on higher input costs to consumers, while inflation is moderating in the services sector. Core goods inflation continued to inch up to 7.6% y-o-y in January from 7.5% in December and 7.1% six months back. Core services inflation, by contrast, has progressively been moderating from 5.5% in September to 5.0% in January,” the Nomura Research paper written by Sonal Varma and Aurodeep Nandi.

In a paper titled “Anatomy of Inflation’s Ascent in India”, published in December 2022, RBI Deputy Governor Michael Debabrata Patra and others provide a broader explanation:

Story continues below this ad

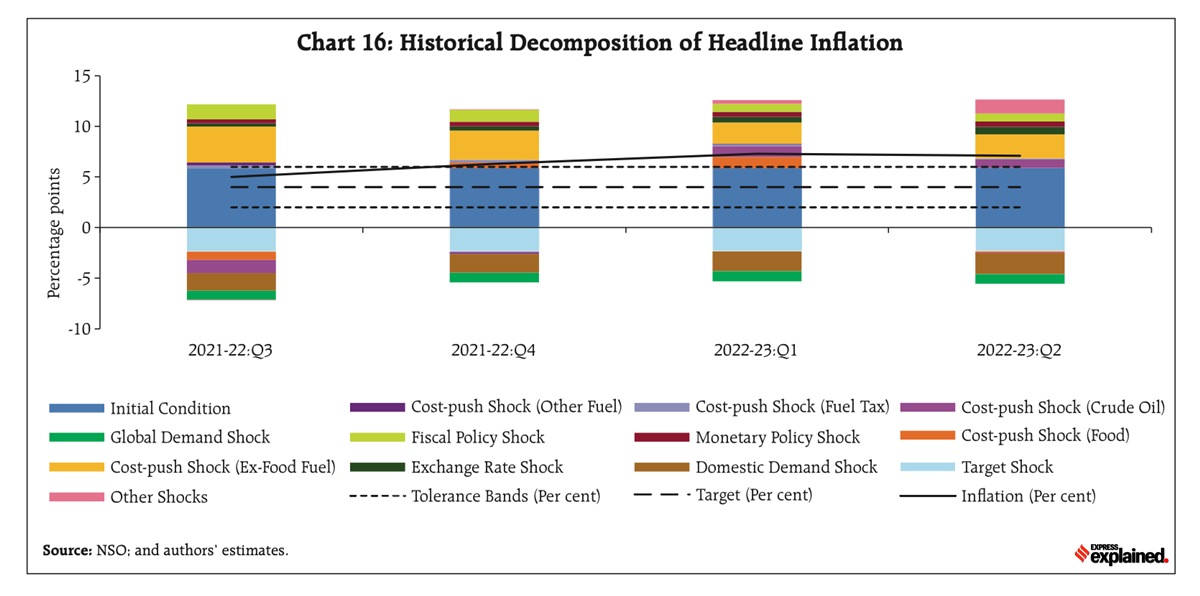

“What started as a shock to food and fuel prices got increasingly generalised over ensuing months. This was reflected in highly elevated and sticky core inflation. Unprecedented input cost pressures got translated to output prices, particularly goods prices, in spite of muted demand conditions and pricing power. As the direct effects of the conflict waned and international commodity prices softened, the strengthening domestic recovery and rising demand enabled pass-through of pent-up input costs, especially in services, adding persistence to elevated inflationary pressures.” (See Chart 2)

Chart 2: Historical Decomposition of Headline Inflation

However, for what it is worth, India is not the only country facing sticky inflation; many others — such as the US and countries in the euro zone — are also struggling to extricate themselves from sticky inflation.

Share your views and queries at udit.misra@expressindia.com

Udit Misra is Senior Associate Editor at The Indian Express. Misra has reported on the Indian economy and policy landscape for the past two decades. He holds a Master’s degree in Economics from the Delhi School of Economics and is a Chevening South Asia Journalism Fellow from the University of Westminster.

Misra is known for explanatory journalism and is a trusted voice among readers not just for simplifying complex economic concepts but also making sense of economic news both in India and abroad.

Professional Focus

He writes three regular columns for the publication.

ExplainSpeaking: A weekly explanatory column that answers the most important questions surrounding the economic and policy developments.

GDP (Graphs, Data, Perspectives): Another weekly column that uses interesting charts and data to provide perspective on an issue dominating the news during the week.

Book, Line & Thinker: A fortnightly column that for reviewing books, both new and old.

Recent Notable Articles (Late 2025)

His recent work focuses heavily on the weakening Indian Rupee, the global impact of U.S. economic policy under Donald Trump, and long-term domestic growth projections:

Currency and Macroeconomics:

"GDP: Anatomy of rupee weakness against the dollar" (Dec 19, 2025) — Investigating why the Rupee remains weak despite India's status as a fast-growing economy.

"GDP: Amid the rupee's fall, how investors are shunning the Indian economy" (Dec 5, 2025).

"Nobel Prize in Economic Sciences 2025: How the winners explained economic growth" (Oct 13, 2025).

Global Geopolitics and Trade:

"Has the US already lost to China? Trump's policies and the shifting global order" (Dec 8, 2025).

"The Great Sanctions Hack: Why economic sanctions don't work the way we expect" (Nov 23, 2025) — Based on former RBI Governor Urjit Patel's new book.

"ExplainSpeaking: How Trump's tariffs have run into an affordability crisis" (Nov 20, 2025).

Domestic Policy and Data:

"GDP: New labour codes and opportunity for India's weakest states" (Nov 28, 2025).

"ExplainSpeaking | Piyush Goyal says India will be a $30 trillion economy in 25 years: Decoding the projections" (Oct 30, 2025) — A critical look at the feasibility of high-growth targets.

"GDP: Examining latest GST collections, and where different states stand" (Nov 7, 2025).

International Economic Comparisons:

"GDP: What ails Germany, world's third-largest economy, and how it could grow" (Nov 14, 2025).

"On the loss of Europe's competitive edge" (Oct 17, 2025).

Signature Style

Udit Misra is known his calm, data-driven, explanation-first economics journalism. He avoids ideological posturing, and writes with the aim of raising the standard of public discourse by providing readers with clarity and understanding of the ground realities.

You can follow him on X (formerly Twitter) at @ieuditmisra

... Read More