© The Indian Express Pvt Ltd

Tags:

Last year was terrible for the global economy. By the time 2022 came to a close, observers across the world believed that several key economies would witness a recession in 2023.

But by the time the most influential policymakers, CEOs and economists met at the World Economic Forum (WEF) in Davos earlier this month, the mood had started to shift.

There is a growing sense that a global recession may not happen, and that some of the biggest economies, such as the US and the Euro-zone countries, may achieve a soft-landing.

What was the picture before WEF?

Between 2020 and 2021, governments and central banks across the world, especially in the richer developed countries, had used a loose fiscal policy (governments spending lots of money) and loose monetary policy (cheaper credit/loans) to contain the economic downturn during Covid. This policy prescription had not only set the world economy up for a period of elevated inflation, but also made it more vulnerable to unexpected supply shocks.

This shock came early in 2022 when Russia invaded Ukraine. The invasion disrupted global supply chains, which had barely recovered from the Covid-induced lockdowns, and spiked commodity (crude oil, fertilisers and foodgrains) prices so sharply that the whole world witnessed historic surges of inflation.

This, in turn, forced central banks to rapidly raise interest rates in a bid to contain inflation by dragging down overall demand. Governments, on their part, pulled back excess spending.

But these policy u-turns essentially meant that economic growth would plummet across the board. With lower growth, it was expected that unemployment would also rise.

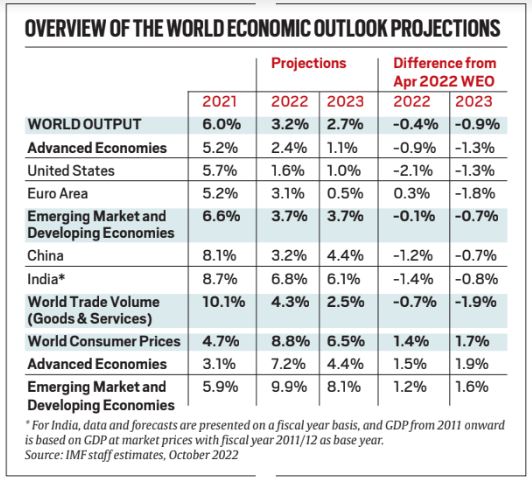

Unsurprisingly, all manners of growth forecast were revised down right through 2022. The International Monetary Fund’s World Economic Outlook (WEO), the benchmark for such forecasts, downgraded global growth outlook thrice during 2022.

In the last WEO published in October, the IMF warned the following: “More than a third of the global economy will contract this year or next, while the three largest economies—the United States, the European Union, and China—will continue to stall. In short, the worst is yet to come, and for many people 2023 will feel like a recession.”

What changed?

The WEF had a panel discussion on global economic growth outlook moderated by a CNBC anchor, who said the following in a bid to capture the sentiment at the end of the summit: “Investors and CEOs are increasingly bullish but they are not optimistic.”

What explains this contradiction was the answer by IMF’s Managing Director Kristalina Georgieva in the same discussion.

“It (global economic growth outlook) is less bad than we feared two months ago but ‘less bad’ doesn’t quite mean ‘good’.”

She further listed four factors that led to such an assessment.

First, the world over, inflation has fallen off its historic peak and is consistently trending downwards.

Two, China, the world’s second largest economy, has seen its growth prospects improve. In 2022, thanks to its Zero Covid policy, China’s growth rate fell below the global average growth rate — the first time in 40 years. However, with China opening to business, its economy is expected to rebound and, in the process, boost global growth.

Three, it was widely expected that as central banks raised interest rates, unemployment levels would rise in the developed countries. But this has not happened to the extent policymakers and economists apprehended. In fact, the developed countries continue to enjoy historically low levels of unemployment.

The fourth and closely related factor is the sustained consumer demand. Georgieva said the strength of labour markets (read low levels of unemployment) in countries such as the US has kept consumer demand robust.

Larry Summers, former Secretary of US Treasury and currently President Emeritus at Harvard, explained the change in sentiment more succinctly: “We are experiencing some exhilaration of relief in Davos”.

“Hyper populists have lost elections, Europe has not frozen, recession hasn’t come, China has adjusted its policies and inflation has decelerated. Those are the reasons why we all feel better now than a few months ago,” said Summers.

Will the world avoid recession?

A more exact answer will be available on January 31, when the IMF provides its next WEO update. But as things stand, policymakers are advising caution.

“Relief must not become complacency,” warned Summers. In his view, inflation was down because of the same transitory factors that contributed to its spike.

“The greatest tragedy would be if central banks were to lurch away from a focus on assuring price stability prematurely and we were to have to fight this battle twice,” said Summers.

Georgieva outlined three key factors that could deflate the fledgling confidence.

One, it is unclear whether inflation will continue to trend downwards. For instance, China’s likely recovery, being seen as a positive factor, could also imply higher prices for crude oil and gas, pushing up inflation across the board. Energy prices remain high as it is.

Two, while labour markets have held up well until now, given the fact that central banks are not yet done with raising rates, it is quite possible that higher interest rates will finally begin to bite and lead to more unemployment. Dealing with the cost of living crisis in developed countries with historically low unemployment is one thing, but if there are widespread job losses, consumption will fall rapidly and with it, economic growth.

Lastly, the fact is that the Ukraine conflict is still unresolved and as such, continues to pose a risk for investors across the world.