© The Indian Express Pvt Ltd

Workers at the Posta wholesale market area in Kolkata in 2021. (Express photo by Partha Paul)

Workers at the Posta wholesale market area in Kolkata in 2021. (Express photo by Partha Paul) Dear Readers,

Many of you are regular readers of ExplainSpeaking, which is a weekly explanatory column on economy and policy issues. From today we are expanding ExplainSpeaking to all weekdays. As such, apart from the regular piece that is published on Monday, The Indian Express website will also carry ExplainSpeaking — nota bene, a quicker take on some of the key issues dominating the news cycle.

Here’s the first edition.

Earlier this week, India’s Ministry of Statistics and Programme Implementation released the provisional estimates of GDP growth for the financial year that ended in March 2023. As it happened, India’s overall economic growth in the fourth quarter (January to March) surprised on the upside and this meant that India’s GDP growth rate for FY23 was pegged at 7.2%, marginally higher than the previously anticipated 7%.

However, this improved performance seems to have led to further polarisation among Indians with regard to how they view the Indian economy. For instance, Raghuram Rajan, the former RBI Governor, has been trending on Twitter and was being pilloried for having expressed his apprehensions of the sustainability of India’s growth momentum in the past. He was particularly criticised for stating that India’s GDP growth rate was tending towards the so-called Hindu Rate of Growth.

To be sure, three months ago, in an interview to PTI, Rajan had stated: “The key question is what Indian growth will be in fiscal 2023-24. I worried earlier that we would be lucky if we hit 5% growth. The latest Oct-Dec Indian GDP numbers (4.4% on year ago and 1% relative to the previous quarter) suggest slowing growth from the heady numbers in the first half of the year. My fears were not misplaced. The RBI projects an even lower 4.2% for the last quarter of this fiscal. At this point, the average annual growth of the Oct-Dec quarter relative to the similar pre- pandemic quarter 3 years ago is 3.7%. This is dangerously close to our old Hindu rate of growth! We must do better.”

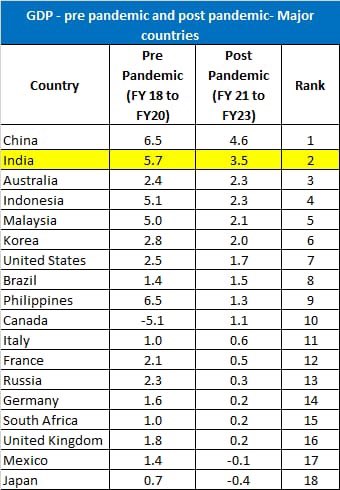

Many experts have pointed out that India has done better than almost all major economies. For instance, Soumya Kanti Ghosh, the Group Chief Economic Adviser, State Bank of India, tweeted stating: “Even as India has registered a 7.2% growth in GDP, the narrative/ story as usual has shifted to average growth rates across countries pre and post pandemic. Even on this count, India stands second across all countries! Waiting now for the next narrative!” (See Table 1).

Table 1: How fast did India grow?

Table 1: How fast did India grow?

As Table 1 shows, if one were to take the GDP growth rates in three years before and three years after the Covid pandemic, India is ranked the second-fastest growing among this list of major economies.

However, while the numbers mentioned in this table are true, Table 1 gives an incomplete picture. Look at Table 2, which incorporates GDP per capita (in current US dollar terms).

Table 2: How fast does India need to grow?

Table 2: How fast does India need to grow?

A quick look shows how far behind India is when compared to the other countries mentioned in the list. In fact, India’s per capita income is the lowest among all the countries mentioned in Table 1.

This single addition completely alters the way Table 1 is read. The gap in per capita GDP (or per capita income) essentially implies that India must grow faster in any given year if it wants to bridge the gap between itself and other major economies. In other words, while it is a good thing that India is growing at a faster clip than the rest, it is also worth noting that doing so is almost a necessity for India, not a choice.

The question is: How fast must India’s per capita GDP grow?

The second last column of Table 2 tries to calculate the number of years required for India to catch up if the GDP per capita of all these countries stops growing while that of India continues to grow at 15% annually. We have taken a growth rate of 15% because the per capita GDP (or income) mentioned here is in nominal US dollar terms while the GDP growth rates are in real terms. In nominal terms, India’s per capita income grew by 15% in FY23 when overall GDP grew by 7.2% in real terms. That is why we have taken 15% as the growth rate for per capita GDP.

What the calculations show is that while we can be happy that India is “ranked” 2nd in this list of major economies, India has a long distance to cover before reaching a point of prosperity.

For instance, India would take a good 12 years to overhaul China (even when China’s per capita GDP does not grow at all and ours grows by 15% annually). Similarly, in per capita GDP terms, it will take India 21 years to overhaul the UK, an economy India has just overtaken in GDP terms.

In fact, India would have to wait for 20 years to overtake 9 of the 17 countries mentioned here. And that is when these countries are presumed to not grow at all.

In other words, even though India is ahead of many countries in GDP terms, what matters more for gauging prosperity is the GDP per capita. And it is here that it becomes clear why growing faster than the rest of the world for years on end is not a matter of choice but a necessity for India.

Hope you like this effort. Please share your suggestions, queries and views at udit.misra@expressindia.com

See you next week,

Udit