© IE Online Media Services Pvt Ltd

Journalism of Courage

A Tanishq store in New Delhi. (Express Archives: Amit Mehra)

A Tanishq store in New Delhi. (Express Archives: Amit Mehra)Over the past year, gold prices have surged nearly 40%, briefly crossing Rs 100,000 per 10 grams in India, a level that typically puts jewellery demand on the defensive. For most jewellers, that’s a headwind: rising prices often push consumers toward lighter, lower-value products or delay purchases altogether.

But Titan isn’t just any jeweller.

Despite muted momentum in studded jewellery and softer average ticket sizes, the company managed to close FY25 with a 22% revenue jump and healthy operating margins, thanks to its expanding footprint, disciplined hedging strategy, and strong showings from watches, eyewear, and CaratLane.

And yet, the stock has barely moved.

Even with buyers returning, international revenues doubling, and new store additions across verticals, Titan trades below its peak, weighed down by concerns over margins, consumer mix, and whether the company’s near 90x earnings multiple still has room to stretch.

The question now isn’t whether Titan can grow, it’s whether that growth can justify its valuation in a tougher pricing and demand environment.

Share Price Movement of Titan Ltd. (Source: Screener.in)

Share Price Movement of Titan Ltd. (Source: Screener.in)

Titan’s business is growing. But so are its headwinds

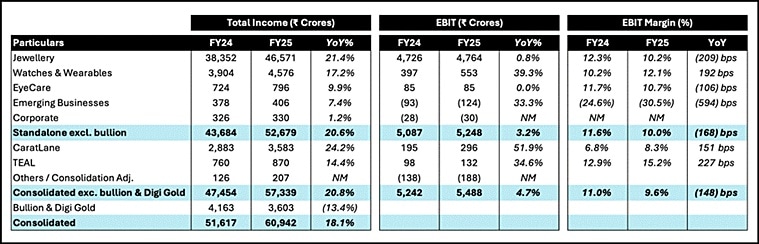

Titan’s core strength, which is consistent growth across product lines and geographies, remained evident in FY25.

The company clocked Rs 57,339 crore in revenue (excluding bullion and digital gold), marking a 20.8% year-on-year increase, with strong performances during both the festive and wedding quarters.

In Q4 alone, total income grew over 21% YoY, led by a 24.8% jump in jewellery sales. The number of buyers rose across segments, underscoring the resilience of Titan’s customer base even in a high-price environment.

Despite the solid top line, net profit for FY25 was flat at Rs 3,337 crore, revealing a growing strain on profitability. While Q4’s jewellery EBIT margin came in at 11.9%, it was propped up by gains from gold hedging and international contango, elements management itself flagged as partly one-off. On a structural basis, the business saw margin compression driven by product mix and softer ASPs.

Titan has always aimed to steer consumers toward high-margin studded jewellery. But in FY25, especially Q4, that shift went into reverse.

Studded jewellery grew just 12% YoY in Q4, while plain gold jewellery rose 27%, and gold coins surged 64%. Even CaratLane, Titan’s digital-first growth engine, saw far stronger growth in plain gold (+44%) than in studs (+19%). The net result: Titan’s studded share dropped 190 basis points year-on-year, eroding blended gross margins.

Part of this is structural: with gold prices hovering near Rs 100,000, consumers opted for lower karatage pieces (18k, 14k, even 9k), smaller sizes, and more affordable designs. Titan noted that buyer numbers were up, but average ticket sizes declined, shifting the revenue mix toward lower-margin offerings.

While Titan maintained its brand premium and expanded its store network, regional rivals like Kalyan and Malabar continued to undercut on price and scale up rapidly. These brands appeal to the same middle-income buyers who, in FY25, led Titan’s volume growth, particularly in entry-level gold. Titan now walks a fine line: defend margins and risk losing share, or adapt pricing and dilute premium positioning.

CaratLane: A digital darling, now a margin contributor

If there’s one business within Titan that embodies both opportunity and evolution, it’s CaratLane. Once known primarily for modern diamond jewellery sold online, the brand has steadily become a key revenue engine, especially among young, urban buyers.

In FY25, CaratLane’s revenue grew 26% year-on-year to Rs 3,583 crore, and in Q4 alone, it rose 23% YoY to Rs 883 crore.

But here, too, the product mix is telling a deeper story.

In Q4, plain gold jewellery grew 44% YoY, while studded jewellery lagged at 19%. The broader market shift where affordability trumps aspiration is playing out even within CaratLane’s core customer base.

High gold prices pushed buyers to downshift toward simpler, more accessible pieces. Titan’s commentary notes this clearly: the company saw more buyers in studded jewellery, but their ticket sizes were smaller, pulling down overall contribution.

Despite the mixed headwinds, CaratLane has quietly become more efficient.

In Q4FY25, it posted an EBIT margin of 7.9%, up from 7.2% a year earlier. For the full year, EBIT rose 51% to Rs 296 crore, signalling that scale, cost discipline, and a maturing supply chain are starting to pay off. This is a critical development. For years, CaratLane was a growth story with thin margins. Now, it’s emerging as a self-sustaining unit that contributes meaningfully to Titan’s overall profitability.

CaratLane’s gross margins are still lower than Tanishq’s, given its leaner product lines and price-sensitive positioning. But the improvement in operating margins signals stronger unit economics — a significant shift in the narrative.

The other noteworthy development is CaratLane’s push into international markets. In FY25, the brand opened its first store in the US (New Jersey), building on Tanishq’s broader global ambitions. While still early, the company views the Indian diaspora, particularly in the US and GCC, as a high-potential audience that aligns well with CaratLane’s design sensibility and price point.

As international operations scale, CaratLane could serve a dual purpose: grow Titan’s global footprint, and hedge against any future softness in domestic premium jewellery demand.

Beyond jewellery: Watches and eyewear are quietly compounding

While jewellery continues to dominate Titan’s topline, the watches and wearables division has quietly become a reliable growth and margin contributor.

In FY25, the segment posted Rs 4,576 crore, up 18% year-on-year. Q4FY25 alone saw revenue grow 19% year-on-year to Rs 1,126 crore.

What’s particularly noteworthy is the margin trajectory.

In Q4, the watches business delivered Rs 133 crore in EBIT, up 66% YoY, with margins expanding from 8.5% to 11.8%. This sharp improvement came from two levers: stronger performance in analog watches (led by the Titan and Fastrack brands) and the premiumisation strategy through Helios Luxe, Titan’s luxury watch retail channel.

Unlike wearables, which faced some saturation and competitive pressure in FY25, analog watches benefited from steady demand and better pricing power. Titan’s long-standing brand recall, expansive retail presence, and hybrid distribution model helped it capture both urban gifting occasions and everyday utility buyers.

The eyewear division continues to be Titan’s smallest vertical but also one of its steadiest.

In FY25, revenue grew 9.9% YoY to Rs 796 crore, while EBIT stayed stagnant. Q4FY25 maintained that trajectory, with 16% revenue growth and an EBIT margin of over 10%, driven by strong volume growth and a surprise standout in sunglasses, which grew 52% year-on-year in the quarter.

Titan Eye+ remains the primary growth channel, but the company is also investing in better customer experience, including digital eye testing, premium lenses, and a wider range of fashion-forward frames. While still a small contributor to overall profits, eyewear helps Titan strengthen its everyday consumer connect, diversify its revenue, and gain scale in a highly fragmented industry.

Valuation and the road ahead: What’s priced in?

Titan’s business remains robust, but its stock continues to price in near-flawless execution.

As of early FY26, the company trades at a market cap of over Rs 3.2 lakh crore, with an implied trailing P/E of around 85-90x based on FY25 net profit of Rs 3,337 crore. Even after a modest stock correction from its peak, Titan is still one of the most expensive names in Indian consumer retail.

These multiples are not new, as investors have long rewarded Titan for brand equity, steady compounding, and a diversified growth model. But with FY25 profits flat and margins under pressure, the gap between narrative and numbers has widened.

The core of the issue lies in profitability.

While revenue grew 22% in FY25, net profit growth was flat. Jewellery margins, though steady in Q4 at 11.9%, benefited from one-time hedging gains, and management has guided for a cautious 11-11.5% band going forward. With studded jewellery mix down 190 bps for the year, and buyers trading down to 14k and even 9k designs, Titan’s product mix is skewing toward lower-margin SKUs, even as footfalls rise.

In other words, growth is increasingly volume-led, not margin-led, a dynamic that makes 85-90x earnings harder to justify without clear signs of operating leverage or premiumisation.

That said, Titan is far from overvalued in a vacuum. The company continues to:

If studded demand rebounds, international operations scale, and new verticals like fragrances and handbags gain traction, Titan can still grow into its multiple. Analysts projecting 15-20% CAGR in earnings over the next three years may find those assumptions realistic, especially if margins stabilise and discretionary spending recovers.

The verdict: A great business, but no room for error

Titan remains a rare business, brand-led, capital-efficient, and diversified. But at these valuations, it’s also priced like nothing can go wrong. FY25 showed us that even Titan isn’t immune to gold price shocks, margin volatility, or a cautious consumer.

The case remains strong for long-term holders. But for new investors, Titan today looks less like a breakout trade and more like a patient compounding story that needs earnings to catch up with the price.

Note: This article relies on data from annual and industry reports. We have used our assumptions for forecasting.

Parth Parikh heads the growth and content vertical at Finsire. He holds an FRM Charter and an MBA in Finance from Narsee Monjee Institute of Management Studies.

Disclosure: The writer and his dependents do not hold the stocks discussed in this article.

The website managers, their employees(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.