© The Indian Express Pvt Ltd

Unfinished construction by China Evergrande in Dongguan, Guangdong Province, China, Sept. 28, 2021. (Gilles Sabri/The New York Times)

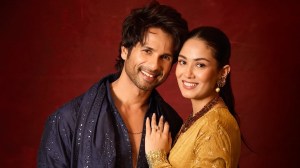

Unfinished construction by China Evergrande in Dongguan, Guangdong Province, China, Sept. 28, 2021. (Gilles Sabri/The New York Times)On Monday (August 25), shares of the property developer Evergrande, which was once one of the biggest companies in China, were delisted from the Hong Kong Stock Exchange.

In 2018, Evergrande became the world’s most valuable real estate company, which also had interests in a wide range of other businesses.

By 2021, it had collapsed in spectacular fashion – both the symptom of changes underway in China’s economy, as well as the reason for the downturn in several allied industries.

At the time of its collapse, Evergrande had more than 1,300 incomplete projects spread across 280 cities in China. The Evergrande stock has lost almost its entire value since the crisis began.

What led to the rise and fall of Evergrande, why do its problems matter, and what impact might the stock exchange delisting have? In an interview with The Indian Express, Lizzi C. Lee, a Fellow at the Center for China Analysis, Asia Society Policy Institute, Washington DC, explains.

Evergrande’s story is intertwined with China’s urbanisation boom. The founder of the company, Hui Ka Yan, who is now 66 years old, rose from poverty to ride a once-in-a-generation wave in the country’s real estate sector.

The boom was driven by massive migration from the countryside to the cities, an unprecedented demand for housing, and a policy environment that rewarded aggressive expansion.

According to data from the World Bank, from 1960 to 1980, the share of the urban population in China’s total population grew from around 16% to 20%. By 1990, it stood at 26%, by 2000 at 36%, and by 2024 around 66%. Another frequently quoted statistic is that China used more cement between 2011 and 2013 than the United States did in the entire 20th century.

Evergrande stepped into this context, and perfected the high-leverage, high-turnover model: buy land at scale, pre-sell apartments, use cash flow to fund the next wave.

Later on, the company diversified into everything from health care to finance, and even sports, buying the Guangzhou Football Club. At its peak in 2017, Evergrande was valued at nearly HK$400 billion (around $51 billion), symbolising China’s real estate-driven growth model.

The unravelling was years in the making. The Chinese government introduced a “three red lines” policy in 2020 as an attempt to discipline overleveraged developers by making the conditions for borrowing stricter. That policy was the proximate trigger, cutting off the cheap credit that Evergrande and other developers depended on.

But the deeper problems were structural. Demand for housing had been slowing as demographics shifted to an ageing population, and many urban households already owned multiple properties.

Evergrande relied on perpetual pre-sales, where it would use the money to immediately start developing the next project. In addition to the thin cash buffers, this made it uniquely vulnerable once credit became tighter and sales softened, partially due to macroeconomic headwinds.

Today, there is a glut of millions of empty homes, as well as many unfinished projects across China.

Collapse does not mean liquidation overnight; it has been a drawn-out process. Evergrande defaulted on its offshore debt, saw its chairman investigated for fraud, and has been under court-ordered liquidation.

The Hong Kong Stock Exchange delisting, after 18 months of suspended trading, is symbolic: it marks the end of Evergrande as a publicly traded company.

However, its obligations remain enormous. Debt restructuring is ongoing, liquidation managers are pursuing asset recovery, and lawsuits are mounting. According to a Reuters report, liquidators say they have sold $255 million of the firm’s assets 18 months into the liquidation process, but received creditor claims totalling $45 billion.

The government’s role has been selective: ensuring “housing delivery” for ordinary buyers while leaving creditors, especially foreign ones, to absorb losses. The delisting underscores that Evergrande is now only a debtor in managed unwinding.

Is Evergrande the first domino to fall in China’s real estate crisis? What have been the spillover effects on the Chinese economy as a whole?

Evergrande wasn’t the only domino, but it was the biggest piece to fall with spectacular scale. Other major companies, including Country Garden which is usually seen as better managed, have also stumbled.

A model in the sales office of Country Garden’s Ten Mile Bay project in Nantong, China on Aug. 19, 2023. (Qilai Shen/The New York Times)

A model in the sales office of Country Garden’s Ten Mile Bay project in Nantong, China on Aug. 19, 2023. (Qilai Shen/The New York Times)

What is critical is the way in which the property sector’s downturn has bled into the broader economy: construction slowdowns hurt steel and cement, local governments lost vital land-sale revenue, and household wealth tied up in property has eroded confidence.

Today, policymakers are trying to stabilise the sector, shifting focus to completing unfinished projects, and easing mortgage rules – but they are not reviving the old model of perpetual expansion.

Even in the most optimistic scenario, the bottoming out of property market prices will not materialise until late next year. And with the sector shrinking, an era of China’s growth has definitively ended.

The Lehman comparison captures the drama but misses key differences. Lehman’s collapse triggered a global financial meltdown because of the way its debts were interwoven with the global banking system.

Evergrande, by contrast, has been managed through a slow-motion, state-guided unwinding. The appointment of Alvarez & Marsal, veterans of Lehman’s restructuring, shows the complexity of the case, but Beijing has worked to firewall systemic contagion.

So far, it has worked. China’s banking system remains stable, and the crisis has been largely ringfenced within the country (as opposed to escalating into a global financial shock).

The Evergrande episode is less a “Chinese Lehman moment” and more a reckoning with the limits of China’s debt-fueled, property-centric growth model. It is a sobering lesson that China’s old growth playbook has run out of road, but the challenge to transition into a healthier and more sustainable path is extremely daunting.