Journalism of Courage

A key bone of contention is the RBI’s instruction to recognise loan default from day one and to initiate steps for resolution. (Express Photo by Pradip Das)

A key bone of contention is the RBI’s instruction to recognise loan default from day one and to initiate steps for resolution. (Express Photo by Pradip Das)

The Reserve Bank of India (RBI) has not yet acceded to the banks’ demand asking the regulator to reconsider withdrawal of flexible restructuring of loan schemes, banking industry sources said. The central bank, through a notification on February 12, has done away with all its earlier instructions dealing with resolution of stressed assets and replaced them with a revised framework.

A key bone of contention is the RBI’s instruction to recognise loan default from day one and to initiate steps for resolution.

“The IBA (Indian Banks’ Association) has written to the RBI for relaxation of its February 12 circular. Though it is aimed at speeding up resolution of stressed assets, in some cases, it may actually hamper it,” a banking industry source said. “We have so far not heard from the RBI on our request,” the source said. Bankers argue that recognition of default from day one and initiation of resolution steps immediately may affect loan accounts especially in the infrastructure and core sectors. Since borrowers receive lumpy payments in these sectors, many a time they have loan installments pending but these are typically cleared within say 30-60 days, another banker said.

“As soon as there is a default in the borrower entity’s account with any lender, all lenders — singly or jointly — shall initiate steps to cure the default. The resolution plan (RP) may involve any actions / plans / reorganisation including, but not limited to, regularisation of the account by payment of all over dues by the borrower entity, sale of the exposures to other entities/investors, change in ownership, or restructuring,” the RBI had said in its February 12 circular.

The IBA has also sought clarity from the central bank on whether if a company secures satisfactory rating, it is necessary to make provision for loss in diminution of value, due to lower interest rate on loans. Banks usually charge lower rates to companies with better credit rating, which may reduce their interest income. The RBI announced the revised framework to align it with the Insolvency and Bankruptcy Code (IBC), which is now a key resolution platform for the lenders. The RBI now requires banks to implement a resolution plan within 180 days and in case of non-implementation, lenders are required to file an insolvency application.

While issuing the revised framework for resolution of loans, the RBI withdrew all its earlier instructions on resolution of stressed assets such as Framework for Revitalising Distressed Assets, Corporate Debt Restructuring Scheme, Flexible Structuring of Existing Long Term Project Loans, Strategic Debt Restructuring Scheme (SDR), Change in Ownership outside SDR, and Scheme for Sustainable Structuring of Stressed Assets (S4A). The Joint Lenders’ Forum as an institutional mechanism for resolution of stressed accounts has also been discontinued.

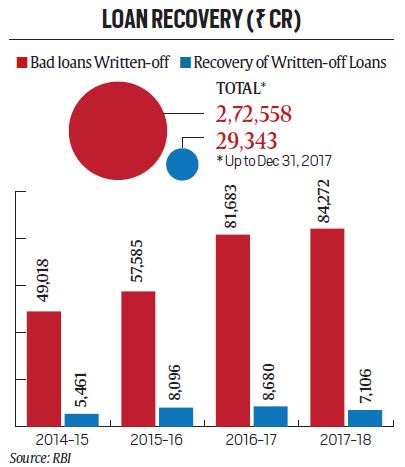

The central bank has issued new rules to ensure faster recovery of bad loans, as banks could recover only Rs 7,106 crore of written-off loans till December 31, 2017 while a total of Rs 84,272 crore worth of bad loans were written-off during the same period.