© The Indian Express Pvt Ltd

Prestige Estates’ evolution from a Bengaluru-based residential developer to a pan-India real estate conglomerate has been characterised by a deliberate expansion into multiple verticals: residential, office spaces, retail, hospitality, and asset management. (Source: https://www.prestigeoakville.info/about-prestige-group)

Prestige Estates’ evolution from a Bengaluru-based residential developer to a pan-India real estate conglomerate has been characterised by a deliberate expansion into multiple verticals: residential, office spaces, retail, hospitality, and asset management. (Source: https://www.prestigeoakville.info/about-prestige-group)Prestige Estates Projects Ltd closed FY24 with its best-ever sales performance. Rs 21,040 crore in bookings, up 63 per cent year-on-year. It has rapidly scaled its operations beyond its Bengaluru base, building a 197 million sq ft pipeline across high-stakes markets such as Mumbai, NCR, Pune, and Hyderabad. It is now one of the largest listed real estate developers in India by sales, trailing only Macrotech Developers.

And yet, the stock has fallen 40 per cent over the past seven to eight months.

Prestige Group’s scale of business. Source: Prestige Annual Report FY24.

Prestige Group’s scale of business. Source: Prestige Annual Report FY24.

That disconnect between record operating performance and steep stock correction is what investors are grappling with.

The company has been clear in its ambition: move from a regional leader to a pan-India powerhouse with growing annuity income and premium project positioning. It is also deploying capital at scale, with ~₹14,000 crore earmarked for commercial, retail, and hospitality assets.

But the market’s reaction suggests concerns around execution, valuation, and financial leverage are now front and centre.

So is this simply a healthy correction after a runaway rally? Or is it the market pricing in risks that have not yet appeared in the financials? To answer that, we need to look deeper into the business model, the shifting revenue dynamics, and the road Prestige has chosen to take.

Prestige Estates Projects Ltd. share price chart (April 2024-April 2025) Source: Screener

Prestige Estates Projects Ltd. share price chart (April 2024-April 2025) Source: Screener

Inside Prestige: A vertical-by-vertical breakdown of India’s emerging real estate giant

Prestige Estates’ evolution from a Bengaluru-based residential developer to a pan-India real estate conglomerate has been characterised by a deliberate expansion into multiple verticals: residential, office spaces, retail, hospitality, and asset management.

Each vertical not only contributes to revenue in distinct ways but also reflects a strategic intent to build a full-stack, future-ready real estate business. Let’s break down the company’s performance and ambition across each of these pillars.

1. Residential: The revenue engine

The residential segment remains Prestige’s core business and biggest growth driver. It accounts for more than ~65 per cent of the company’s overall sales value, and is the segment where the brand enjoys the deepest consumer trust, particularly in South India.

Prestige Group’s residential business. Source: Prestige Annual Report FY24

Prestige Group’s residential business. Source: Prestige Annual Report FY24

Prestige has sold over 127 million sq ft in residential space to date, with marquee projects in Bengaluru, Hyderabad, Chennai, and increasingly in Mumbai and NCR.

FY24 was its most successful year yet, with Rs 5,105 crore in revenue and over 10,000 units sold.

The company is now clearly pivoting upmarket.

While it once dominated the affordable and mid-income segment in Bengaluru, Prestige is now selling premium projects in Mumbai (Prestige Ocean Towers in BKC), NCR (Bougainvillea Gardens, Ghaziabad township), and Hyderabad (Prestige City).

This shift is reflected in the company’s average selling price, which rose to ₹10,400 per sq ft, an 18 per cent increase year-over-year. Going forward, Prestige is expected to focus heavily on township-style developments under the ‘Prestige City’ brand, with large-format launches planned in Mumbai, Noida, Hyderabad, and Pune. These townships offer scale, long-term cash flow visibility, and brand stickiness, positioning Prestige to dominate the premium mass-market segment in metro cities.

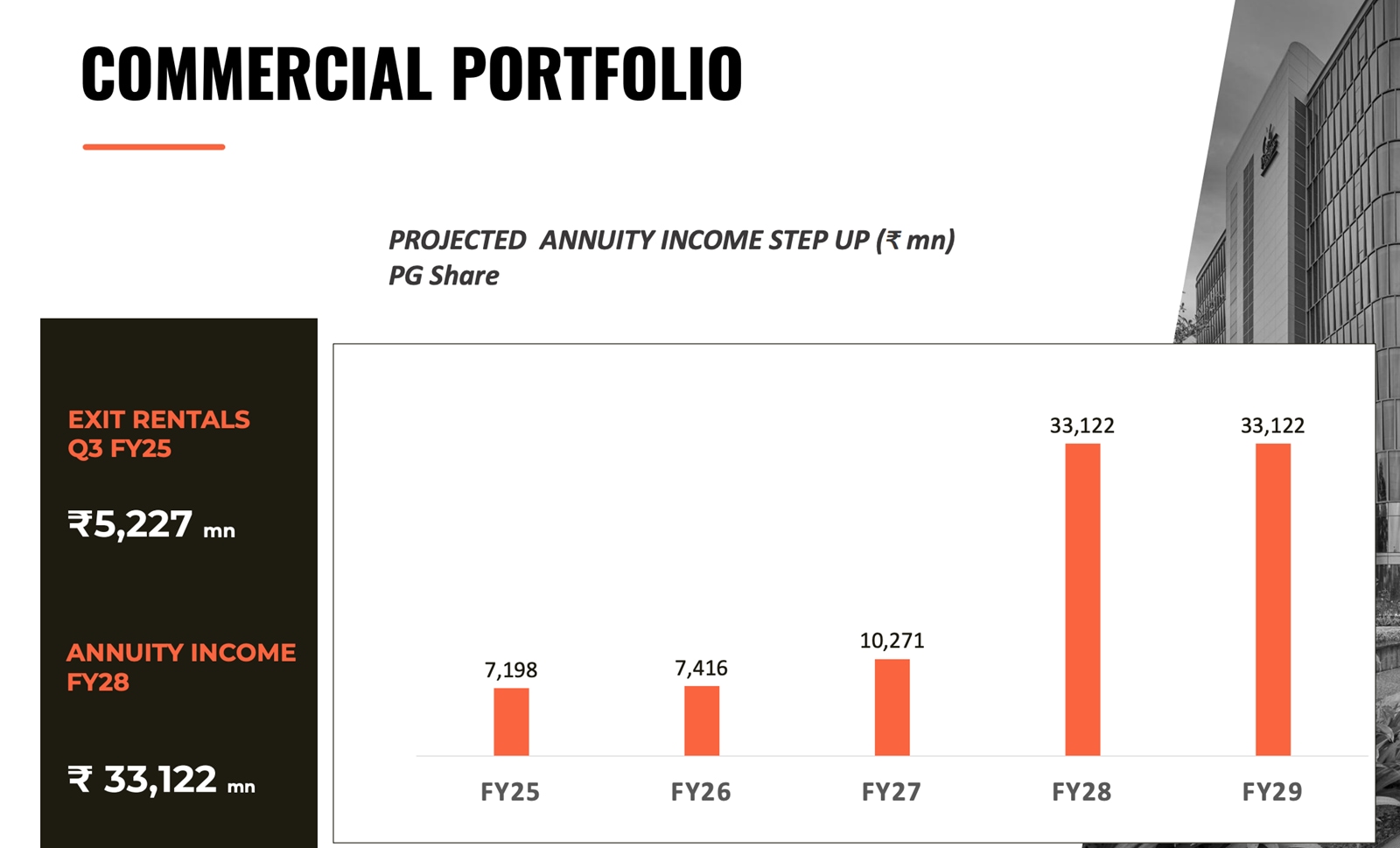

2. Commercial office: the emerging annuity core

Prestige has quietly built one of the strongest office development businesses among listed peers, second only to DLF in terms of potential scale.

In FY25, office assets are likely to generate Rs 719 crore in rental income. The company has a pipeline of 24 million sq ft under construction or in planning, with the goal of generating over Rs 2,000 crore in office rentals over the next three to five years.

Prestige Group’s commercial business. Source: Prestige Quarterly Report December 25

Prestige Group’s commercial business. Source: Prestige Quarterly Report December 25

The existing office portfolio includes flagship developments like Prestige Tech Park and Prestige Falcon City in Bengaluru, with expanding footprints in Chennai and Hyderabad. However, the next phase of growth is focused on the Mumbai Metropolitan Region (MMR) and NCR, with the company actively acquiring land and building pre-leased assets in Tier 1 office corridors.

Unlike some of its peers, who adopt asset-light or joint-venture-led models, Prestige is pursuing a develop-and-hold strategy, betting on the long-term income stability of office leasing, especially with the rising demand for high-quality, integrated business parks.

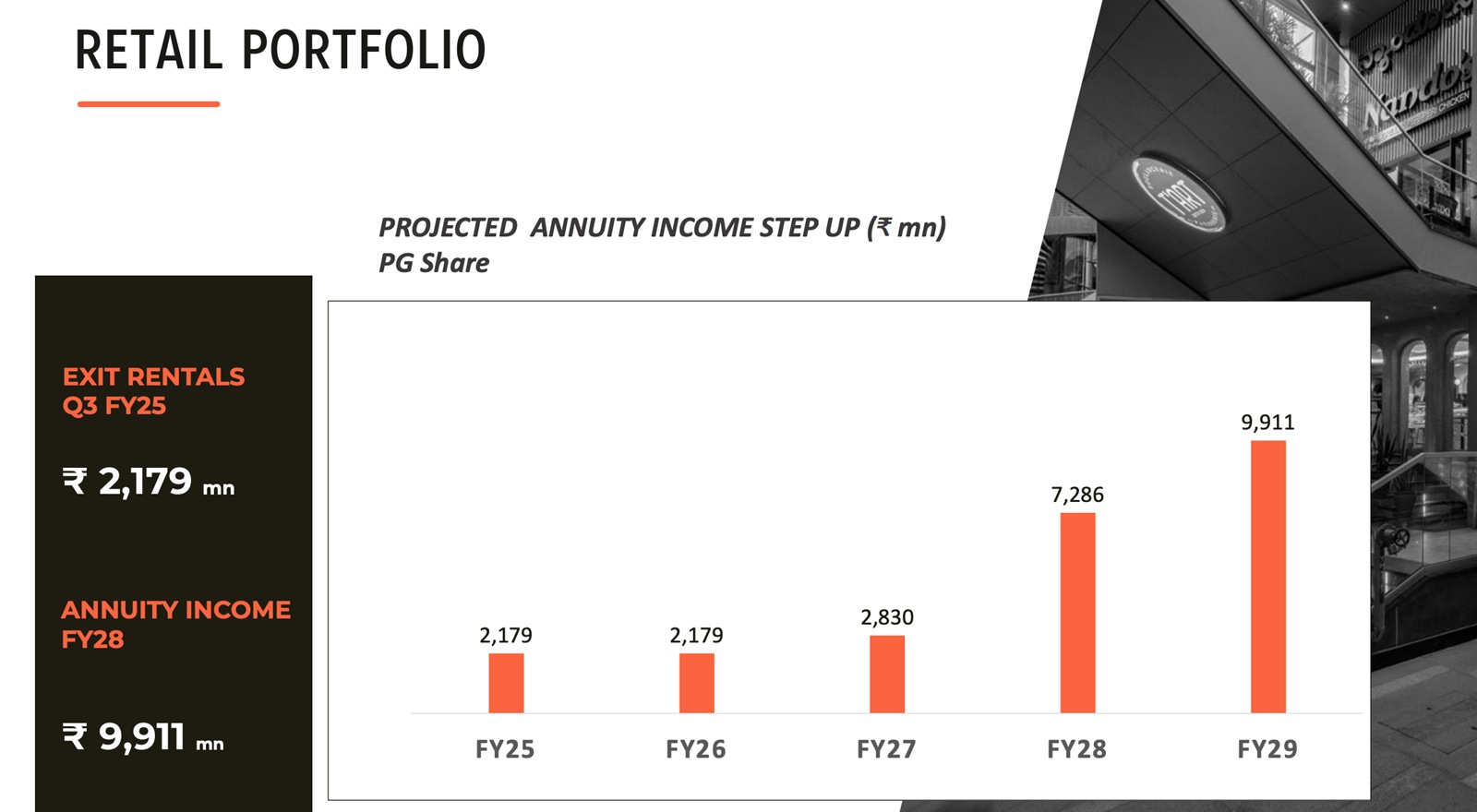

3. Retail: Forum returns as a national mall brand

Retail has long been a Prestige stronghold as its Forum Mall brand was among the earliest modern retail formats in India. While the segment experienced muted activity during the COVID-19 pandemic, it is now a central focus again.

Prestige currently operates approximately 10 million sq ft of retail space and has a pipeline of 12 million sq ft planned across various cities.

In 9MFY25, retail rentals were included in the Rs 217 crore annuity income figure, which also includes office rentals. However, the company expects its retail rental income to exceed Rs 1,000 crore by FY27, driven by the upcoming malls in Bengaluru (Forum Mall at Prestige Falcon City), Chennai, Kochi, and Hyderabad.

Prestige Group’s retail business. Source: Prestige Quarterly Report Dec 25

Prestige Group’s retail business. Source: Prestige Quarterly Report Dec 25

What sets Prestige apart in retail is its integration of retail into township developments, as malls are not standalone but act as lifestyle anchors within mixed-use ecosystems. This strategy enhances foot traffic, boosts residential pricing in adjacent towers, and improves customer loyalty.

4. Hospitality: a bet on premium brand tie-ups

Prestige’s hospitality business is relatively smaller in terms of revenue but strategically valuable.

The company currently operates eight hotels with 1,477 rooms, under management agreements with global brands such as Marriott, Hilton, Sheraton, and Conrad.

In FY24, hospitality revenue stood at Rs 240 crore, with earnings before interest, taxes, depreciation, and amortisation (EBITDA) margins expected to improve as room rates normalise post-pandemic.

With an additional 3,000 keys under development, Prestige aims to more than double its hospitality portfolio by FY27, with an estimated income potential of Rs 2,500 crore at full maturity. Most new hotels are part of larger mixed-use developments, especially in MMR and NCR, allowing Prestige to extract higher returns on land while retaining strategic control of property operations.

The company views this vertical not just as a cash flow driver, but also as a brand play. Premium hotels enhance brand visibility, elevate project positioning, and aid in pricing residential and commercial assets within the same development.

5. Asset Management and monetisation: laying the REIT road

While Prestige has not yet listed a real estate investment trust (REIT), it has taken steps toward creating a REIT-ready annuity portfolio.

The Rs 9,100 crore asset sale to Blackstone in 2021 was the first major monetisation, allowing the company to deleverage and reinvest in growth.

With a targeted ~Rs 4,000 crore annuity EBITDA by FY28, Prestige could be among the next in line for a multi-asset REIT listing, especially if rental assets in retail and office stabilise as planned.

Moreover, Prestige has signed structured investment deals with global investors like ADIA and Kotak AIF, raising ₹2,001 crore in FY24 for project-level partnerships across Bengaluru, Goa, Mumbai, and NCR. These co-investment structures allow Prestige to share risk while retaining development upside—an increasingly preferred model among institutional-grade developers.

Financials, valuation, and what retail investors should watch

If Prestige Estates’ Rs 21,000 crore in FY24 pre-sales was a headline grabber, the company’s financial performance underneath reveals a more complex narrative.

Revenue vs bookings: the accounting mismatch

Prestige reported Rs 7,877 crore in consolidated revenue in FY24, down 5 per cent year-over-year. At first glance, that might seem inconsistent with its record pre-sales.

But this disconnect is an accounting feature of the real estate industry: revenue is recognised only when construction milestones are met and possession begins, not when units are booked.

That said, what matters for medium-term earnings visibility is the company’s collection efficiency and execution pipeline.

Prestige collected Rs 11,950 crore in FY24, a 22 per cent increase from the previous year, providing a solid buffer for construction outlays and interest servicing. More importantly, this amount is nearly 1.5x its recognised revenue, indicating a clear earnings buildup for the next 12–24 months.

The FY24 EBITDA stood at Rs 2,498 crore, representing a 20 per cent year-over-year growth, with margins expanding to approximately 32 per cent. This operational improvement, despite slower revenue growth, suggests better pricing discipline and cost efficiency.

Profitability under transition

Prestige reported a net profit of Rs 1,629 crore in FY24. However, there was a one-time income of Rs 851 crore as a part of the gain on the disposal of the joint venture. Excluding that, the net profit was flat year-over-year.

This plateau in net earnings is primarily due to higher interest costs, continued reinvestment into new projects, and subdued revenue recognition despite surging bookings.

What is worth tracking is the company’s profitability trajectory over FY25–26, when several large township and commercial projects are expected to reach handover stages.

Retail investors should therefore not just look at trailing earnings, but also the backlog of booked-but-unrecognised revenue, which will convert into P&L numbers as projects cross delivery thresholds.

Valuation: from euphoria to equilibrium

After touching a peak of Rs 2,070 in early 2024, Prestige’s stock has corrected to around Rs 1,170–1,200 levels.

At its peak, the stock was trading at ~85x trailing P/E and nearly 4x book value, which was unsustainably high. The correction brings it back to a more reasonable 3x book value and ~35x forward earnings, based on estimated FY26 profits.

Note: This does not predict where the stock price could head. It’s just an if-then calculation for academic purposes.

Prestige’s price-to-sales ratio (~2.4x FY24 revenue) and enterprise value-to-EBITDA (~6x) are now closer to large-cap peers like DLF and Godrej Properties, especially when accounting for the annuity income pipeline. In other words, the valuation today reflects future execution, not a deep value play, but also no longer priced for perfection.

Key financial specifics to track

For retail investors evaluating Prestige as a long-term investment, here are the key metrics that matter:

1. Pre-sales to revenue conversion rate: Prestige booked Rs 21,000 crore in FY24 but recognised only Rs 7,877 crore. The pace at which this backlog converts into revenue will determine future earnings growth.

2. Debt levels and servicing: As of 9MFY25, net debt stood at ~Rs 6,000 crore, with a net debt-to-equity ratio of ~0.4x. While manageable, any delay in collections or project execution could strain the balance sheet, especially with ₹15,000 crore of planned capex over the next few years.

3. Capital efficiency and ROE: Prestige’s return on equity (ROE) stood at ~12% in FY24, higher than peers, but lower than DLF due to lower rental contribution. Sustained ROE improvement will depend on better capital turnover and timely monetisation.

4. Land bank monetisation: The company holds 772 acres of land, one of the largest among listed peers. Efficient use of this inventory, either via joint development or outright monetisation, will significantly impact margins and return ratios.

The bottom line: execution needs to catch up with ambition

Prestige today stands at a strategic inflection point. Its valuation has reset from exuberant to realistic. Its financials are healthy, but earnings are still in transition. The company’s booked revenue is building a base for future growth, but that growth will now be closely scrutinised for timeliness, discipline, and cash flow impact.

Retail investors need to recognise that Prestige is not a high-dividend, low-volatility play as it is a growth-focused real estate bet, with exposure to both the upside of India’s urban expansion and the downside risks of overextension and market cyclicality.

For investors with a three to five year horizon, Prestige offers a compelling mix of scale, brand, and visibility. But it is not a “buy it and forget it” stock. It is one that needs to be tracked, quarter by quarter, city by city, and vertical by vertical.

Note: This article relies on data from the annual report and industry reports. We have used our assumptions for forecasting.

Parth Parikh has over a decade of experience in finance and research and currently heads the growth and content vertical at Finsire. He has a keen interest in Indian and global stocks and holds an FRM Charter along with an MBA in Finance from Narsee Monjee Institute of Management Studies. Previously, he held research positions at various companies.

Disclosure: The writer and his dependents do not hold the stocks discussed in this article.

The website’s managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.