© The Indian Express Pvt Ltd

“We have been assured by our IT team that the reporting system will be developed before June 30. We will be ready to launch it on July 1,” a private sector lender said. “We have to see how foolproof the system is going to be as there are certain exemptions and thousands of low value transactions. As it’s a tax issue involving the government, the RBI has not come out with any clarification,” said another bank official who didn’t want to be named.

“We have been assured by our IT team that the reporting system will be developed before June 30. We will be ready to launch it on July 1,” a private sector lender said. “We have to see how foolproof the system is going to be as there are certain exemptions and thousands of low value transactions. As it’s a tax issue involving the government, the RBI has not come out with any clarification,” said another bank official who didn’t want to be named.

With the 20 per cent tax on Liberalised Remittances Scheme (LRS) of the Reserve Bank of India set to kick off from July 1, banks are gearing up to get ready with the systems to track the spends on international cards and mobilise the tax collected at source (TCS) on outward remittances.

Banks were finding the going tough in assessing and collecting TCS on exemptions while using credit and debit cards outside India, banking sources said. The Reserve Bank of India (RBI), on the other hand, has left it to the banks to fend for themselves to collect the tax imposed by the government in the FY23-24 budget.

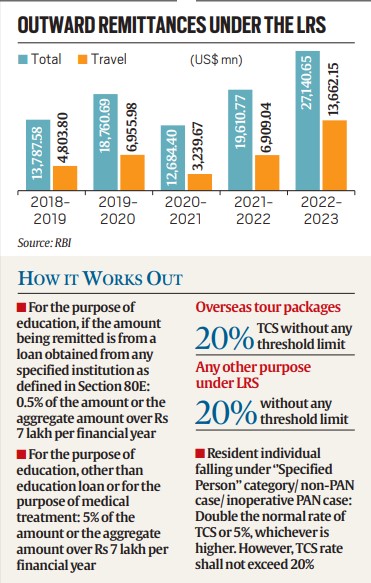

“Deducting TCS is not a hassle. The hassle is where you have certain exemptions and how to fit those exemptions into the system. The exemption of up to Rs 7 lakh created some confusion but the government gave enough time to address it. Our system (for reporting international card spends) is ready,” said a senior official of a bank. Under the RBI’s LRS scheme, a resident individual can take out $ 250,000 (around Rs 2.05 crore) every financial year. On February 1, 2023, the government decided to impose 20 per cent tax on foreign remittances except for overseas education and medical treatment. There was an outflow of $ 27.14 billion (over Rs 2.22 lakh crore) under the LRS route in FY23.

“We have been assured by our IT team that the reporting system will be developed before June 30. We will be ready to launch it on July 1,” a private sector lender said. “We have to see how foolproof the system is going to be as there are certain exemptions and thousands of low value transactions. As it’s a tax issue involving the government, the RBI has not come out with any clarification,” said another bank official who didn’t want to be named.

With credit cards now coming under LRS, if a person spends $10,000 (Rs 8,20,000) through credit cards abroad, he will have to shell out $2,000 (Rs 1,64,000) as tax.

Indians are now increasingly using credit and debit cards abroad instead of taking travellers cheques or forex cards. While there is no estimate of money spent through cards abroad, banks are worried about the logistical requirement.

When contacted for clarifications, the Indian Banks Association did not respond to The Indian Express.

At a 20 per cent tax, the government would have earned a TCS of Rs 22,400 crore on overseas travel expenses of Rs 1.12 lakh crore ($13.66 billion) – a jump of 185 per cent from $4.8 billion in FY2019– by Indians in FY2023. However, bankers are estimating that use of credit cards, gift, and maintenance of relatives abroad are likely to come down in the near-term due to the 20 per cent tax. Earlier, use of credit cards for making payments during travel outside India was not included in the LRS limit.

The Budget 2023-24 had proposed hiking the TCS rate to 20 per cent from 5 per cent above Rs 7 lakh threshold for all purposes other than education and medical treatment. Also, for overseas tour packages, the government had proposed hiking the TCS rate to 20 per cent from 5 per cent, without any threshold, with effect from July 1. On May 16, the Centre amended rules under the Foreign Exchange Management Act (FEMA), bringing international credit card spends under the LRS. As a consequence, spending on international credit cards would have then attracted a higher rate of TCS at 20 per cent from July 1. However, on May 19, the government clarified that any payments by an individual using their international debit or credit cards up to Rs 7 lakh per financial year will be excluded from the LRS limits and hence, will not attract any TCS.

TCS can be adjusted against the overall tax liability. It can be claimed as an income tax refund or a person can avail of credit while filing the ITR or calculating the advance taxes. The new system will enable the government to track high-value overseas transactions and will not apply on the payments for purchase of foreign goods and services from India.

“PAN should be valid and operative from July 1, 2023… the bank will check validity of PAN in terms, whether Aadhaar is linked to PAN or not. In case PAN is inoperative, TCS would be charged at the rate applicable to non-PAN case,” HDFC Bank said in a communication to its customers. In non-PAN case or inoperative PAN, TCS will be double the normal rate or 5 per cent, whichever is higher. However, TCS rate will not exceed 20 per cent.