© IE Online Media Services Pvt Ltd

Journalism of Courage

The company has been consistent in stating that 70-75% of its total enquiries come organically. (Photo Credit: Facebook)

The company has been consistent in stating that 70-75% of its total enquiries come organically. (Photo Credit: Facebook)Over the past few years, IndiaMART has established itself as a digital platform that is profitable, generates free cash flow consistently, and boasts EBITDA margins above 30%.

In a tech world where growth is often subsidised by cash burn, IndiaMART’s business model — monetising verified business enquiries through subscriptions — has looked steady, predictable, and scalable (to a large extent).

But after a strong run between 2018 and 2021, both operational metrics and the stock have entered a different phase.

Revenue continues to grow in double digits, ARPU is rising, and margins remain healthy. Yet net additions of paying suppliers have flattened, and the share price has struggled to break out meaningfully over the past 18 months.

Q1 FY26 numbers reinforce this split.

Revenue rose 12% YoY, deferred revenue grew 16%, and net profit margin was 33%. Collections were up 13%, showing robust cash flows. However, the net supplier addition of only 1.5K, representing just 1%, in the quarter was again muted, following several quarters of low additions.

This creates a pivotal narrative.

IndiaMART has strong pricing power, a cash chest of over Rs 2,700 crore, and a dominant position in B2B discovery. But can it translate all of this into a fresh growth cycle? Or is the business entering a more mature phase, where higher monetisation from a stable base becomes the primary lever and not expansion?

As investors watch the stock hover well below its 2021 highs despite strong financial performance, the real question is whether IndiaMART can start operating with momentum in a market that is still largely offline, price-sensitive, and slow to convert.

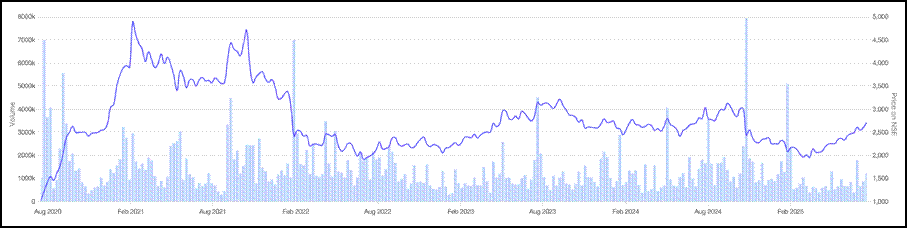

Stock Price Movement for IndiaMART InterMESH. (Source: Screener.in)

Stock Price Movement for IndiaMART InterMESH. (Source: Screener.in)

Business model, moat, and what the financials say

IndiaMART operates on a simple but high-margin model: it connects buyers with suppliers across more than 100,000 product categories. The buyers list their requirements. The suppliers, mainly SMEs, pay for verified leads through subscription plans.

This makes IndiaMART a discovery platform and not a transactional one. It does not hold inventory, manage logistics, or provide payment gateways. Instead, it charges for visibility. That positioning has helped the company maintain asset-light operations, steady margins, and healthy cash flows for over a decade.

But with over 185,000 paying suppliers already on board and limited net additions in the last few quarters, the growth challenge is no longer one of coverage. It is more about deepening monetisation and creating more value per user.

Where the moat lies: Data, depth, and trust

IndiaMART’s competitive edge is more than just a tech stack. The real moat lies in the three below-mentioned points:

● Massive database of over 70 lakh listed suppliers and 10 crore product SKUs

● Lead generation engine fine-tuned over years

● High organic traffic with deep keyword penetration across industrial and B2B verticals.

The company has been consistent in stating that 70-75% of its total enquiries come organically. This reduces dependence on paid acquisition and keeps cost of acquisition (CAC) low.

The trust moat is also significant: IndiaMART has been around since 1999. In many Tier-2 and Tier-3 cities, it is the default first stop for small business owners looking to get discovered online.

Q1 FY26: High efficiency, muted expansion

Financially, Q1 FY26 is an example of operating discipline with restrained expansion:

|

Metric |

Q1 FY26 |

YoY Growth |

QoQ Growth |

|

Consolidated Revenue |

₹308 Cr |

12% |

4% |

|

Collections |

₹323 Cr |

15% |

7% |

|

Deferred Revenue |

₹825 Cr |

14% |

2% |

|

Net Profit |

₹102 Cr |

21% |

3% |

|

EBITDA Margin |

39% |

– |

– |

|

Paying Supplier Additions |

+1,500 net adds |

Flat |

Flat |

The biggest positive here is operating leverage. While revenue grew 12%, net profit rose 21%. That means the company is squeezing more out of each rupee earned without resorting to aggressive spending.

The EBITDA margin of 39% is among the highest in India’s listed digital business universe. The Rs 2,700+ crore cash balance, with minimal debt, gives the company a wide runway to experiment or even acquire, if it chooses.

However, the 1,500 net supplier additions, a repeat of the same number in Q4, raise valid questions. With so many small businesses still offline or unlisted, why is net user growth so stagnant?

Management tone: Cautiously optimistic

The management’s commentary during the results and last conference call suggests the company is working to address this:

● They acknowledged that supplier churn remains a key focus area, especially among first-year subscribers.

● IndiaMART has been refining its onboarding journey with simplifying dashboards, improving enquiry quality, and lowering the number of suppliers per lead to boost conversions.

● The company reduced the average number of suppliers per lead from ~6 to ~4, aiming to improve ROI for paying users.

● There is also continued investment in adjacent services (Busy Accounting, Livekeeping, Legistify, etc.) that could unlock deeper monetisation in FY26 and FY27.

But management also reiterated that growth spending would remain calibrated.

Valuation, market expectations, and the road ahead

After peaking in 2021, the share price has remained largely range-bound, currently hovering around Rs 2,600.

At current levels, the stock trades at around 25 times trailing earnings and over 10 times sales. These are not cheap multiples, especially for a company with muted user growth and modest top-line expansion. But they reflect investor confidence in the business model’s durability, free cash flow visibility, and optionality around platform extensions.

For the market to re-rate the stock meaningfully, two things likely need to happen:

Faster net addition of paying suppliers without compromising churn and ARPU

Demonstrated monetisation from value-added services like CRM, invoicing, SaaS tools, and compliance tech, which are currently under-penetrated

So far, IndiaMART has resisted the temptation to burn capital or force growth. That makes sense, given its subscriber-first model and long renewal cycles.

But as digital adoption accelerates in smaller cities and formalisation deepens, the opportunity to convert more suppliers remains real, if executed well.

The long view

IndiaMART’s core thesis remains intact:

● It solves a real discovery problem for SMEs

● It monetises through a stable, high-margin subscription model

● It enjoys high trust and organic visibility in a fragmented market

But like any maturing digital business, it now faces the challenge of growing deeper, not just wider. The Rs 2,700 crore cash reserve gives it room to try. The brand recall gives it an edge in retention. What remains to be seen is whether IndiaMART can shift gears from a compounding cash machine to a reinvention engine.

For now, it is doing many things right. But the next Rs 1,000 crore in revenue will likely come slower and require more innovation than the last.

Note: This article relies on data from annual and industry reports. We have used our assumptions for forecasting.

Parth Parikh has over a decade of experience in finance and research and currently heads the growth and content vertical at Finsire. He holds an FRM Charter and an MBA in Finance from Narsee Monjee Institute of Management Studies.

Disclosure: The writer and his dependents do not hold the stocks discussed in this article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.