© The Indian Express Pvt Ltd

Journalism of Courage

Brainbees Solutions is the parent company of popular baby and kids brands FirstCry and Babyhug. (Credit: firstcry.com)

Brainbees Solutions is the parent company of popular baby and kids brands FirstCry and Babyhug. (Credit: firstcry.com)Brainbees Solutions, the parent company of popular baby and kids brands FirstCry and Babyhug, went public in August 2024, raising Rs 4,200 crore.

Since then, both the Nifty 500 and Brainbees Solutions stock have corrected, with the latter now trading nearly 50% below its listing price.

So, is it a value buy, or just another ‘broken IPO’? Let’s take a closer look.

Brainbees Solutions operates across four business segments, but the online stores of FirstCry, along with hundreds of physical stores for brands such as Babyhug, make up the largest segment.

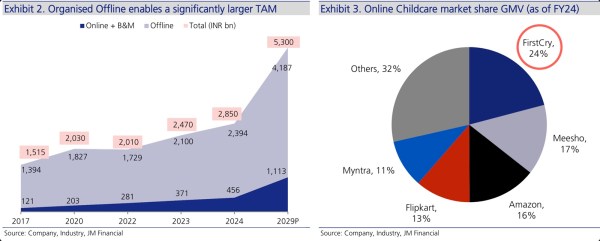

According to a JM Financial Report, FirstCry has the largest market share in the online childcare segment at 24%.

The outlook for the segment is supported by two large trends: a shift from unorganised to organised, and a presumably better value proposition offered by FirstCry versus competitors.

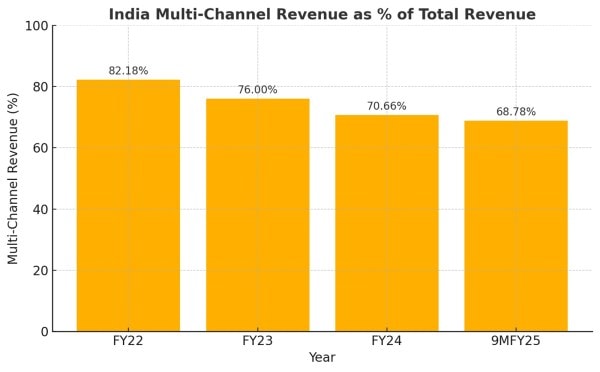

For the nine months ending December 31, 2024, this segment contributed 68.78% to the total revenue. However, in percentage terms, this segment is gradually declining.

This is because of faster revenue growth from other segments, such as GlobalBees, a Thrasio-styled D2C brand “roll-up” engine, and expansion into the Middle East kidswear business.

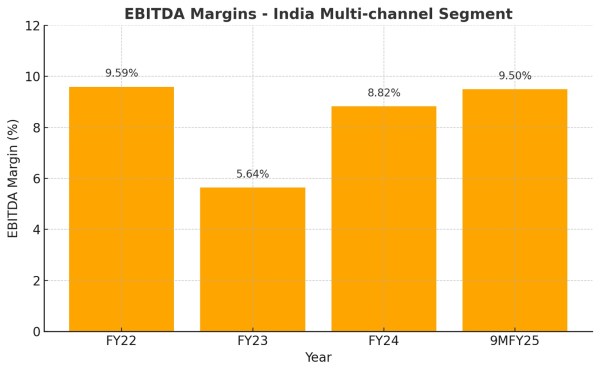

Brainbees Solutions reports adjusted EBITDA (Earnings Before Interest, Tax, Depreciation & Amortisation) margin or operating profit margin. Barring FY23, when the adjusted EBITDA margin for the segment dipped to 5.6%, it has remained around 9-10% on a YoY basis. The adjustment is basis adjustment (addition) of ESOP expenses, which are a non-cash charge on the P&L statement. However, this must be taken with a pinch of salt. While ESOP expenses represent a notional non-cash charge on a quarterly basis, they are costs to the shareholder in the form of equity dilution that shows up later.

With this segment contributing a lion’s share of revenue, the question is: What could be the steady-state EBITDA margin for this business?

Since a majority of the sales come from clothing, one possible comparable set would be listed apparel manufacturers and retailers.

An evaluation of cotton textile players on screener.in reveals a ballpark of 15% median EBITDA margin. This is subject to fluctuations year to year.

We could argue that infant wear enjoys a slight premium compared to adult clothing. It is also believed that it is relatively inelastic to pricing and immune to economic slowdown.

Kitex garments, one of the leading suppliers of kids’ clothing to US retailers such as Walmart, boasts a margin of around 20%. Page Industries, perhaps a gold standard in innerwear, also a sub-segment of apparel/clothing, boasts a margin of around 20%.

Based on these observations, we can broadly estimate that FirstCry’s India business could be anywhere between 15% and 20% on a steady-state basis, subject to yearly fluctuations.

If revenue growth is 15% over FY24 revenue of Rs 4,579 crore, we can estimate FY25 revenue to be Rs 5,266 crore.

A 20x EBITDA multiple would not be a steep multiple for a market leader in the infant wear category in India with both online and offline presence. This would peg Brainbees’ valuation to Rs 16,000 crore.

Compared to its current market cap of around Rs 17,600 crore and based on the above back-of-the-envelope calculations, this would entail that the business is trading around fair value.

JM Financial, which was also the book-running lead manager to Brainbees’ IPO, forecasts EBITDA margin to be 14% by FY29 and 15% by FY34.

Two other larger segments include GlobalBees and the international kidswear business in the UAE and Saudi Arabia.

In the nine months of FY25, GlobalBees accounted for 20.5% of revenue and reported an adjusted EBITDA margin of 1.6%.

During the same period, the international kidswear business accounted for 11.4% of revenue and an adjusted EBITDA loss of 17%.

Steady-state estimates of EBITDA margins in these businesses are difficult to estimate at this point because both are in the investment phase and not profitable.

With nearly 30% of the total revenue coming from these businesses, any analyst would ask: What is the rationale for expanding GlobalBees and international kidswear?

Some of the reasons provided in the Red Herring Prospectus and JM financial report include:

Capitalising on the D2C market boom

Leveraging operational synergies

Diversifying product portfolio

Achieving economies of scale

This raises some questions: Is the company so dominant in the Indian baby and mothercare segment that it is flush with free cash that it can’t possibly reinvest in the existing business?

With cash PAT for 9M FY25 being Rs 140 crore, it is empirically difficult to say the above holds.

If the infant wear business was doing well, with excellent prospects and a “moat” that is well entrenched, why would the company look to “diversify” its product portfolio? Would it not be better to invest capital and resources in its core business?

One of the rationales highlighted for GlobalBees’ existence is “leveraging operational synergies”. As of March 2024, GlobalBees owned 21 brands. These brands absorbed hundreds of crores in investments and are not in the same niche as the existing baby and mothercare segment.

So, what operating efficiencies is the company hoping to leverage?

The RHP outlines that the effort with this segment would be to ‘diversify’ away from the baby and mothercare segment.

Could a case not be made that investing the same resources within the infant wear business, where it has a “moat”, be a smarter albeit boring move?

Similarly, the rationale behind expansion in the Middle East is that the company “wants to replicate its Indian multi-channel playbook” in that market. On a 9-month FY25 basis, cash PAT of just Rs 140 crore on revenue of Rs 5,729 crore.

Would it not be more constructive to first ensure that the core business is profitable?

Based on our earlier estimates, a 15% EBITDA margin in the core business could be highly remunerative for the core business if it can achieve the 15% mark. The timeline for the same appears to be a few years away.

The remaining businesses – GlobalBees and international business – are in the investment phase with no steady state EBITDA margins or profitability estimates.

Firstcry.in’s pre-school segment is profitable with a 20%+ EBITDA margin, but with a revenue of just Rs 35 crore on a 9-month FY25 basis, contributes almost nothing to the overall valuation.

Therefore, the business deserves a re-rating only if core business EBITDA margins improve faster than expected because the other segments are either unlikely to add significantly to profitability or cash flows or are too small in the overall pie to drive valuations.

In the absence of timely improvement in the core segment, it is unlikely that the stock will get re-rated. For the 1.15 lakh retail shareholders as of December 2025, patience may be the only strategy.

Note: We have relied on data from http://www.Screener.in and http://www.tijorifinance.com throughout this article. Only in cases where the data was not available have we used an alternate, but widely used and accepted source of information.

Rahul Rao has helped conduct financial literacy programmes for over 1,50,000 investors. He also worked at an AIF, focusing on small and mid-cap opportunities.

Disclosure: The writer or his dependents Hold shares in the securities/stocks/bonds discussed in the article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources, and only after consulting such independent advisors as may be necessary.