Opinion How NFHS data can help craft policy for women’s financial inclusion

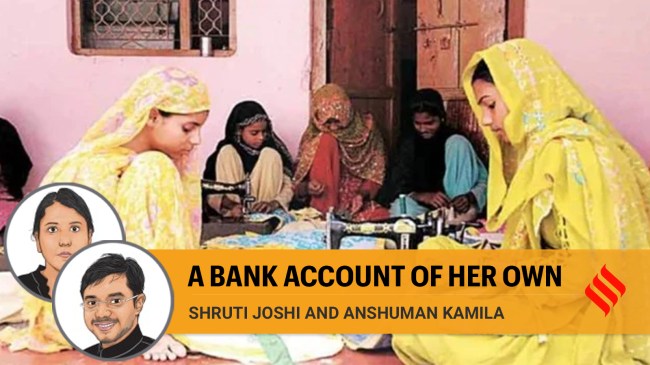

Financial inclusion awareness programmes must give special attention to women in households not headed by women

Financial inclusion awareness programmes must give special attention to women in households not headed by women. (Representational Image)

Financial inclusion awareness programmes must give special attention to women in households not headed by women. (Representational Image)

Financial inclusion is essential for a nation’s sustained development and growth. Its importance in building a sustainable and inclusive future is evident from the significance attached to financial inclusion in the UN’s Sustainable Development Goals (SDGs). Financial inclusion is seen as an enabler of eight out of the 17 SDGs. India has a below-average score in economy in the Global Gender Gap Report 2023 — health, education and politics are the other criteria in this report. The criteria on economy also deal with the gender gap in economic participation and opportunity — this is measured in terms of labour force participation rate and estimated earned income, inter alia. Financial inclusion of women helps to close these gaps. Therefore, taking stock is imperative.

As per the World Bank’s Global Findex Database 2021, adult ownership of bank accounts or regulated institutions such as a credit union, microfinance institutions or a mobile money service provider has increased globally by 50 percentage points between 2011 to 2020. The increase in India has also been impressive, with a jump of 42 percentage points in this period. Moreover, the gender gap in account ownership has also closed substantially in India. In this context, the Pradhan Mantri Jan Dhan Yojana, launched in 2014, made a significant impact in enabling the opening of basic savings bank accounts, inter alia, for over 28 crore women (as of January 2024). Further, financial inclusion has received a fillip through steps taken to boost the participation of women in the economy – these include the Deendayal Antyodaya Yojana, the National Rural Livelihood Mission (DAY-NRLM), skill training under Skill India Mission, Mission Shakti and social protection schemes such as the Pradhan Mantri Awas Yojana and Pradhan Mantri Matru Vandana Yojana.

Using multiple rounds of the National Family Health Survey (NFHS), we have found more dimensions of steady progress in the financial inclusion of women in India. It is heartening that in crucial criteria such as sovereignty over a certain sum of money, possessing a self-operated bank account, awareness about micro-credit programmes and availing of micro-credit schemes, women have clocked gains over the past two decades.

NFHS data also reveal several individual and household characteristics that have an impact on women’s access to financial services. Using NFHS 5 data, collected during 2019-21 for 5.44 lakh women respondents in rural India, we identified the drivers of ownership and usage of accounts at a formal financial institution, usage of mobile phones for digital modes of payment and knowledge and utilisation of micro-credit programmes.

We found that education, skills (particularly digital skills), occupation, access to electronic media and age were significant drivers of financial inclusion among women. For instance, we found that educated women were more likely to know about the micro-credit schemes in their locality. Women with primary and secondary education were more likely to take a loan from these programmes, whereas women with higher education were less likely to use these programmes as opposed to women with no education. This is reasonable because although women with higher education are likely to be aware of and have the wherewithal to access formal channels of credit and lending, micro-credit schemes typically target women with low levels of education – such women find it hard to negotiate formal banking relationships even though they are creditworthy in terms of their entrepreneurial ability.

We found that working women in general — irrespective of their occupation group — were more likely to know about these loan programmes and avail them. Educated, digitally skilled, young and employed women were more likely to use digital modes of transaction. We also found that the gender of the head of the household and the assets and wealth he or she has, influences access to micro-credit.

This study throws up some important learnings to fine-tune our approach and increase financial inclusion. NFHS data suggests that women in women-headed households are favourably placed in owning and using a bank account, in using their mobile phone for digital financial transactions and in accessing micro-credit. Therefore, financial inclusion awareness programmes must give special attention to women in households not headed by women.

Similarly, since skills and education positively impact financial inclusion, it would be advisable to incorporate modules on financial awareness in education and skill development frameworks. Given the shifting sands and novel developments in the financial sector, such modules must be updated regularly. The increasing use of digital financial transactions among the youth has lent greater urgency to the need to disseminate awareness about cyber safety and safe digital banking practices, especially so given the rising trend of financial cyber-crimes and frauds.

Joshi is with the Reserve Bank of India and Kamila is with the Indian Economic Service. Views are personal