Journalism of Courage

Robust in terms of asset quality,loan growth and operational efficiency

NIM moderates 10bp q-o-q led by decline in yield on loans: NII (net interest income) grew 7% quarter-on-quarter and 27% year-on-year to R37.3 bn. However,it included a one-off dividend income of R1 bn from mutual fund. Adjusted for which,NII was in line with the estimate. This was neutral on profitability as the bank booked a loss on investment of a similar magnitude.

Reported margins declined 10bp q-o-q to 4.2%,was led by a 20bp (basis point) q-o-q contraction in yield on loan (on the back of reduction in base rate),while deposits declined by just 10bp q-o-q. Continued traction in retail liabilities,superior CASA (current and savings account) ratio and higher share of fixed rate retail loans would help HDFCB maintain superior margins,going forward.

Reported margins declined 10bp q-o-q to 4.2%,was led by a 20bp (basis point) q-o-q contraction in yield on loan (on the back of reduction in base rate),while deposits declined by just 10bp q-o-q. Continued traction in retail liabilities,superior CASA (current and savings account) ratio and higher share of fixed rate retail loans would help HDFCB maintain superior margins,going forward.

Fee income performance remains impressive

Non-interest income stood at R13.4 bn (18% below our estimate) due to a loss on sale of investment of R1.1 bn and moderation in forex income (R2.4 bn compared to R3.1 bn in Q1FY13 and R2.2 bn in Q2FY12). Fee income growth was strong at 5% q-o-q and 22% y-o-y vs 19% y-o-y for FY12.

Impeccable asset quality; credit cost contained at 30bp

GNPAs (gross non-performing assets) in absolute terms increased just 2% q-o-q. In percentage terms,GNPA declined further to 0.9%,compared to 1% a quarter ago,while NNPAs (net NPAs) were flat q-o-q. PCR (provision coverage ratio) improved to 82% (vs 81% q-o-q). Benign asset quality in the retail segment and lower exposure to stressed sectors in the corporate segment are leading to consistently strong asset quality performance,thus keeping credit cost under check.

During the quarter,provisions stood at R2.9 bn,of which R750m is towards floating provisions. Outstanding pool of floating provision stood at R17.5 bn (R7.5/share). Specific provision related to credit cost stood at 30bp vs reported 34bp in Q4FY12 and 24bp in Q2FY12 and the gross restructured loan in percentage terms was stable q-o-q at 0.3%.

Strong loan growth; proportion of retail loans increases to 53%

Reported loans grew 8.6% q-o-q and 23% y-o-y to R2.3 trillion. Growth was strong in both retail (+10% q-o-q) and non-retail segment (+7% q-o-q),while on a y-o-y basis,the growth in retail segment (+33%) outpaced the non-retail segment (+13%). Hence,the share of retail loans in overall loans increased to 53.1% vs 49.3% a year ago (52.4% a quarter ago).

The management mentioned that while the sequential growth in non-retail loans looks strong,it remains tepid on a y-o-y basis due to loans sell-off in Q4FY12. The bank reported strong growth in CV/CE (commercial vehicle/construction equipment) loans (+14% q-o-q,+45% y-o-y),business banking (+10% q-o-q and 28% y-o-y) and housing loan (+14% q-o-q and 26% y-o-y),led by a portfolio buyout of R25 bn.

Traction in gold loan remained strong (+15% q-o-q,+86% y-o-y) and its share in the overall portfolio increased to 1.7% v/s 1.1% in Q2FY12 and 1.6% Q1FY13. Growth in unsecured loan–retail credit card (+12% q-o-q) and personal loan (+7% q-o-q) continued to show an impressive growth as well. Auto loans grew at a pace of 5% q-o-q and 18% y-o-y. The only laggards in the retail segment were two-wheeler loans and loan against shares (flat q-o-q).

Cost to core income ratio declines marginally q-o-q

Opex (operational expenditure) grew 3% q-o-q and 26% y-o-y to R25 bn. Employee expenses declined q-o-q as the base of Q1 had some one-off provisions. Adjusted for which,employee expenses would have been flat. Thus,the cost to core income declined to 48.3%,compared to 49.2% a quarter ago and 48.8% a year ago. HDFCB added 56 branches and 607 ATMs during the quarter. Cumulatively,it has added 470 branches and 3,796 ATMs in last one year.

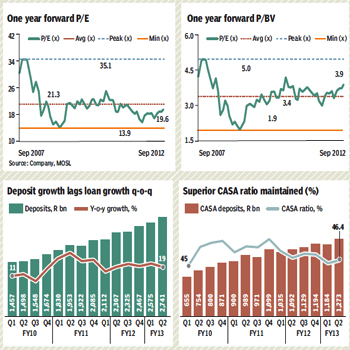

Healthy SA deposit growth; CASA ratio stable q-o-q

SA (savings account) deposits growth was healthy at +3% q-o-q and +15% y-o-y,despite the competitive intensity post-deregulation in savings deposit rates. CA deposits grew (+15% q-o-q and 20% y-o-y) and included a one-off float at the quarter-end; adjusted for which,the CA growth was 8% q-o-q and 12% y-o-y. Core CASA ratio was stable q-o-q at 46%.

Valuation and view

HDFCB is best placed in the current environment,with (i) CASA ratio of 46%,(ii) growth outlook of 1.3x the industry growth,(iii) improving operating efficiency,(iv) expected traction in income due to strong expansion in branch network and (v) best in the class asset quality. The bank has effectively utilised excess profits in the past quarters to create a buffer. HDFCB has been able to consistently deliver margins of 4.2%+ despite an increase in the cost of funds. In a falling interest rate scenario,the higher proportion of fixed rate loan and CASA deposits would provide a cushion to margins.

A third of HDFCBs branches are less than 24 months old; further,a large part of branch expansion happened outside top nine cities. Going forward,this expansion in hinterland shall not only help customer acquisition and product penetration,but also help achieve priority sector targets.

We expect EPS CAGR (earnings per share,compound annual growth rate) of 27% over FY12-14,against 25% over FY07-12. HDFCB also carries a floating provision of R17.5 bn created in the past two years to smooth the strong earnings growth led by better-than-factored credit cost on retail loans.

Though we remain positive on the banks business,we believe valuations are rich. Over FY07-12,peak one-year forward P/BV (price-to-book value) was 5x (times) and average one-year forward P/BV was 3.4x. The stock trades at 4.2x FY13e (estimates) and 3.6x FY14e BV and P/E (price-earnings ratio) of 22.1x FY13e and 17.7x FY14e. Maintain Neutral.

MOSL