© The Indian Express Pvt Ltd

Journalism of Courage

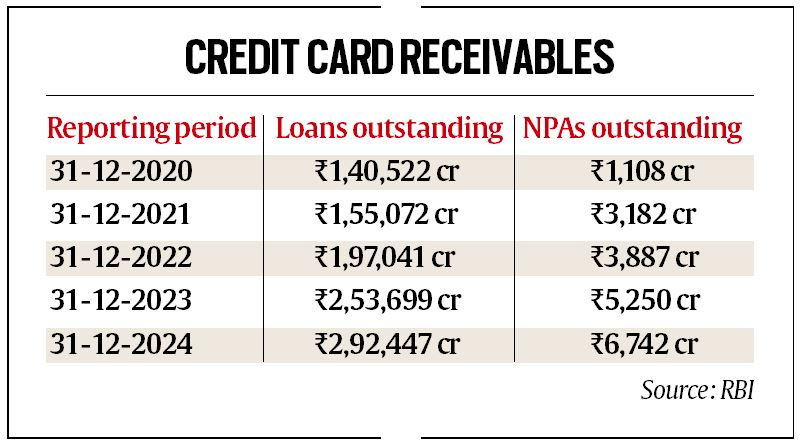

Credit card NPAs have shot up by over 500 per cent from Rs 1,108 crore as of December 2020.

Credit card NPAs have shot up by over 500 per cent from Rs 1,108 crore as of December 2020.Credit card usage has gone up significantly in the last three years, driven by increased consumer spending and the growing popularity of digital payments. However, non-performing assets (NPAs), or the amount defaulted by customers, in the credit card segment have also risen by 28.42 per cent to Rs 6,742 crore during the 12-month period ended December 2024, according to the latest Reserve Bank of India data.

The RBI data shows that gross NPAs rose from Rs 5,250 crore in December 2023 to the current level, a rise of nearly Rs 1,500 crore, amid a slowdown in the economy. This works out to 2.3 per cent of the gross loan outstanding of Rs 2.92 lakh crore in the credit card segment of commercial banks in December 2024 as against 2.06 per cent of Rs 2.53 lakh crore credit card outstanding in the previous year.

Credit card NPAs have shot up by over 500 per cent from Rs 1,108 crore as of December 2020, according to the reply to the RTI request filed by The Indian Express. This has happened at a time when banks managed to bring down overall gross NPAs from Rs 5 lakh crore (2.5 per cent of advances) in December 2023 to Rs 4.55 lakh crore (2.41 per cent) by December 2024.

While Indian banks have succeeded in reducing NPAs, or loans defaulted by borrowers, over the past two years, a closer look reveals a significant rise in NPAs within the personal loan and credit card segments. This spike coincides with an increase in borrower indebtedness, casting a shadow over the sector’s progress.

Credit card outstanding is unsecured in nature and carry high interest rates. A loan account becomes an NPA when the interest or principal instalment is more than 90 days overdue. When a customer delays repayment of his credit card bill beyond the billing cycle, the bank charges a high interest rate of 42-46 per cent interest per annum on the outstanding dues and his credit score also plummets.

Card outstanding is the amount due from customers after the interest-free period offered by banks.

What has lured customers to the credit card segment are incentives like rewards on higher spending, loan offers and lounge benefits. “Customers should realise that if they keep card dues beyond the interest-free period, they end up paying an interest rate of up to 42 per cent in some cases. It will put them in a debt trap,” said a bank official.

In November 2023, the RBI had increased risk weight on the exposure of banks towards consumer credit, credit card receivables and non-banking finance companies (NBFCs) by 25 per cent up to 150 per cent. The move was aimed to address build-up of any risks in these segments. “Even as inquiry volumes remain robust, the impact of increase in risk weights on certain segments of consumer credit pulled down the rate of growth in overall consumer credit, especially personal loans and credit cards,” the RBI’s FSR report said.

Credit card use is rising rapidly in the country, if the customer spends through this route are any indication. The value of credit card transactions tripled in the last three years to Rs 18.31 lakh crore during the year ended March 2024 from Rs 6.30 lakh crore in March 2021 with the economy emerging from the pandemic and consumer confidence increasing over the past several quarters. Credit card transactions were Rs 1.84 lakh crore in the month of January 2025, up sharply from Rs 64,737 crore in January 2021. The number of credit cards issued by banks also rose rapidly to 10.88 crore as of January 2025 from 9.95 crore in January 2024 and 6.10 crore in January 2021, RBI data shows.