© IE Online Media Services Pvt Ltd

Journalism of Courage

Food delivery remains the bedrock of Zomato’s operations, but its contribution as a percentage of total revenue is gradually stabilising. (Source: Freepik)

Food delivery remains the bedrock of Zomato’s operations, but its contribution as a percentage of total revenue is gradually stabilising. (Source: Freepik)Zomato has always been a stock that sparks strong opinions.

From its high-flying IPO in 2021 to its rollercoaster journey through sharp declines and stunning recoveries, the food-tech giant has kept investors on edge.

Just a month ago, Zomato was riding high, delivering a stellar 130% return over the past year and trading at a valuation even higher than DMart’s. It was hailed as a symbol of India’s digital consumption boom, expanding aggressively across verticals like quick commerce and entertainment.

But the last 30 days have been a stark reminder of how quickly markets can turn.

The stock has tumbled 30% from its peak, slashing its one-year return to 60%. For investors who joined at the top, the decline is even more painful.

This sudden shift has reignited questions about Zomato’s ability to sustain its ambitious growth narrative. Is this a short-term correction for a high-growth company or a sign of cracks in its broader strategy? With the company still juggling profitability pressures, stiff competition, and the costs of scaling its new ventures, the answer remains as complex as the business itself.

But one thing is certain — Zomato’s journey remains as unpredictable as ever. The question now is whether the stock can stage another comeback or if its growth engine is finally running out of fuel.

Stock price movement of Zomato Ltd. (Source: Screener.in)

Stock price movement of Zomato Ltd. (Source: Screener.in)

Zomato’s business has evolved into a carefully curated buffet of offerings, catering to the changing tastes of India’s urban population.

While food delivery remains its core dish, the company’s entry into quick commerce through Blinkit has added a spicy new flavour to its menu. Together, these segments are driving Zomato’s growth story, but how sustainable is this multi-course strategy?

In a market that has matured into a duopoly between Zomato and Swiggy, Zomato has managed to pull ahead with a 55% market share compared to Swiggy’s 42%.

The 13% gap underlines Zomato’s stronger foothold, but also keeps the competition alive.

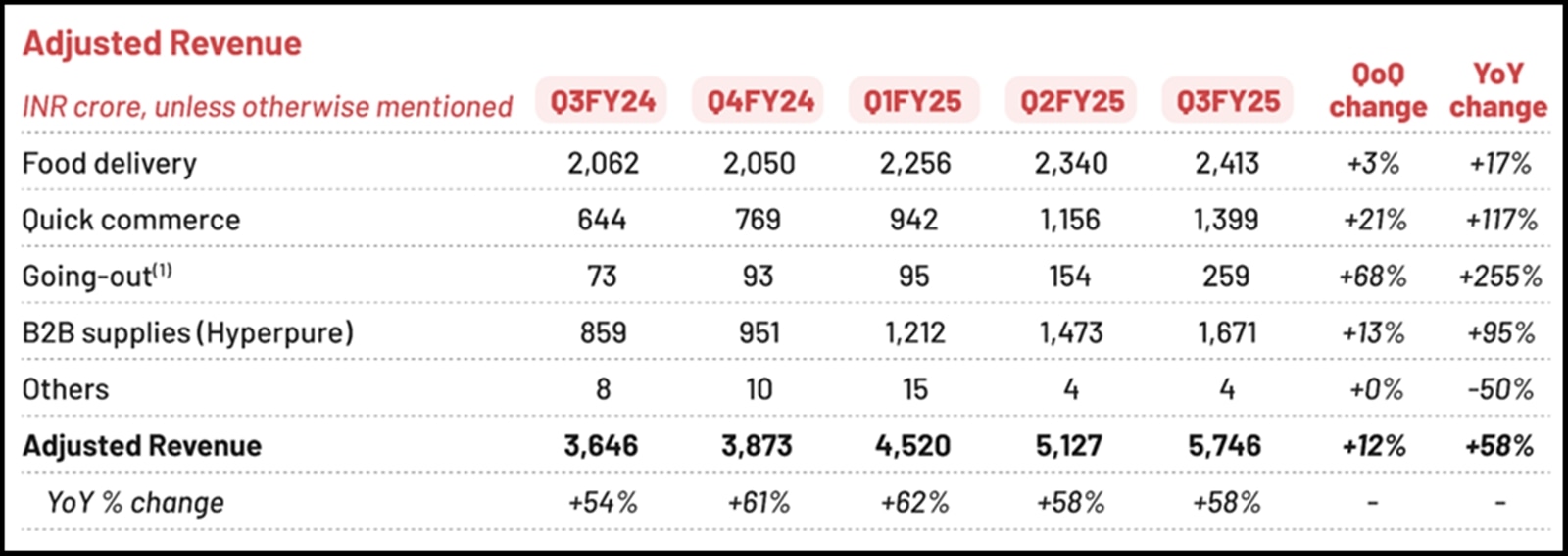

Food delivery remains the bedrock of Zomato’s operations, but its contribution as a percentage of total revenue is gradually stabilising.

This isn’t a sign of stagnation — in fact, the business continues to grow at a healthy rate of around 20% year-on-year. Instead, the shift reflects the rise of other fast-growing verticals, such as quick commerce (via Blinkit), which are expanding rapidly and diversifying Zomato’s revenue streams.

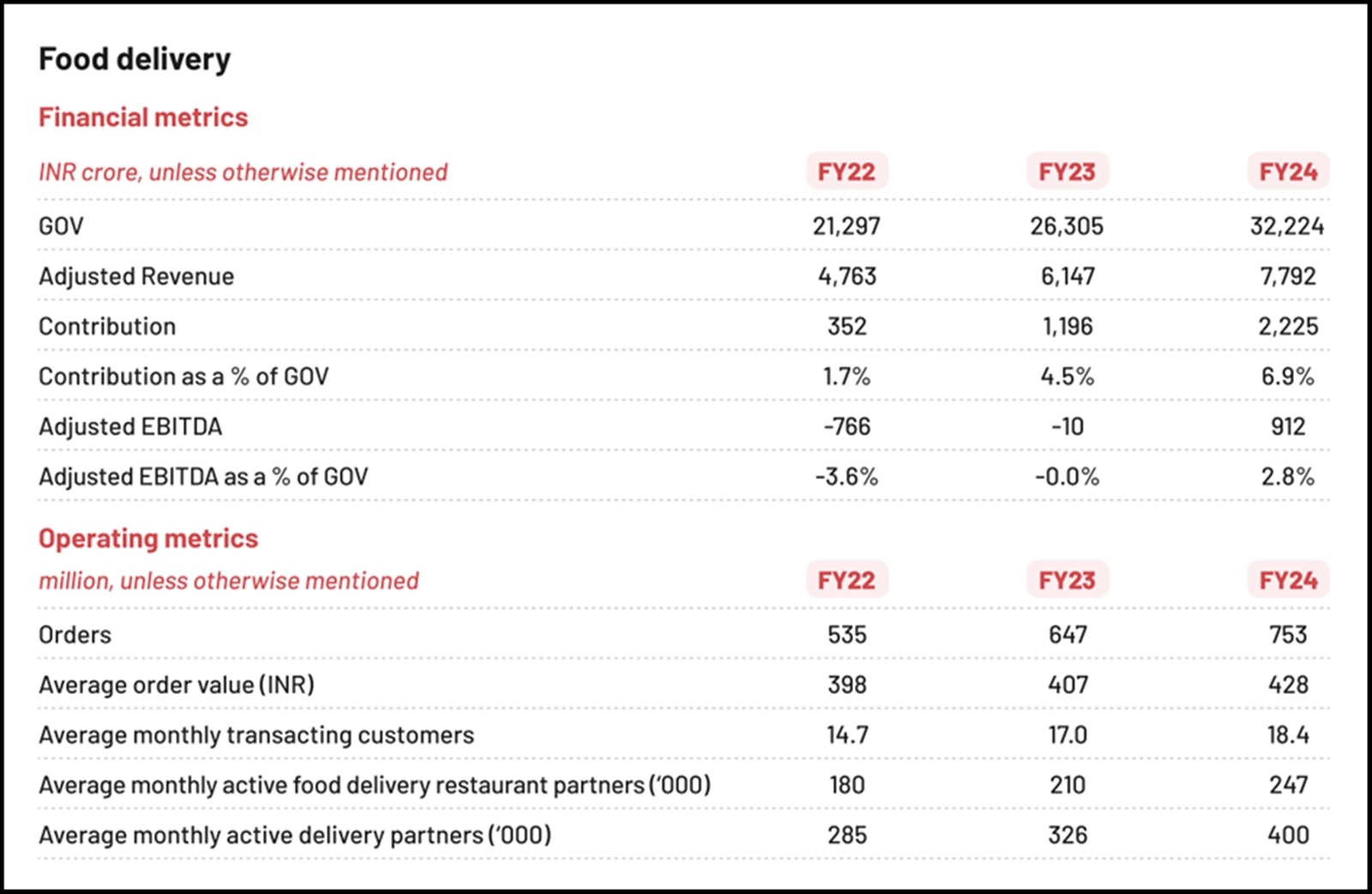

Between FY24 and the first nine months of FY25, Zomato’s gross order value (GOV) in food delivery grew by 20%, with adjusted revenues following suit. This growth underscores the robustness of the segment, even as newer businesses begin contributing more significantly to the company’s top line.

The platform recorded an average monthly transacting user base of 20.5 million in Q3FY25, supported by curated restaurant partnerships and an average order value (AOV) of ₹440.

| Year | Zomato’s Revenue | Food Service Revenue | Food Service Revenue as a % of Total Revenue |

| FY 22 | 5,541 | 4,763 | 86% |

| FY 23 | 8,693 | 6,147 | 71% |

| FY 24 | 13,545 | 7,792 | 58% |

| 9M FY 25 | 15,395 | 7,009 | 46% |

Zomato’s Food Delivery Business. (Source: Zomato’s Annual Report FY24)

Zomato’s Food Delivery Business. (Source: Zomato’s Annual Report FY24)

Zomato’s Revenue. (Source: Source: Zomato’s Q3FY25 Report)

Zomato’s Revenue. (Source: Source: Zomato’s Q3FY25 Report)

Zomato’s food delivery business has transitioned from rapid expansion to profitability. In Q3FY25, consolidated adjusted EBITDA grew a remarkable 128% YoY to ₹285 crore. The adjusted EBITDA margin, measured as a percentage of GOV, rose to 4.3% in Q3FY25 from 3.0% in the same quarter a year ago.

This improvement was driven by:

Platform Fee Optimisation: A modest increase in customer platform fees contributed to improved margins.

Cost Efficiencies: Better logistics, lower delivery costs, and reduced operational overheads added to profitability.

The company has projected that adjusted EBITDA margins could stabilise at around 5% in the next few quarters, signaling continued focus on efficiency.

Zomato is not content with its existing playbook. It recently launched two new services:

Quick restaurant delivery: Restaurants listed on Zomato are now being enabled to deliver select menu items in under 15 minutes, leveraging curated menus and dedicated fleets. This service is currently live in select cities, with plans for gradual scaling.

Bistro by Blinkit: Targeting corporate offices, Bistro aims to address the untapped market for quick snacks, beverages, and meals. This initiative is a strategic step into a market traditionally served by vending machines and onsite vendors.

These innovations highlight Zomato’s focus on addressing niche markets while enhancing customer convenience.

The short answer: highly unlikely. Here’s why:

Steep capital barriers: The food delivery market has already seen over ₹56,000 crore ($7 billion) in investments, primarily between Zomato and Swiggy. Matching this scale requires a risk appetite that few new entrants possess.

Network effects: Zomato’s relationships with 300,000+ restaurants and 200,000+ delivery partners create a competitive moat that would take years to replicate.

Customer loyalty: Zomato’s widespread adoption, driven by loyalty programmes like Zomato Gold, makes it difficult for new players to lure customers away.

For now, Zomato and Swiggy’s dominance seems unassailable, solidifying their positions as the only major players in India’s food delivery ecosystem.

The Indian food delivery market, valued at ₹60,000 crore in FY24, is projected to grow to ₹2 lakh crore by 2030, representing a compound annual growth rate (CAGR) of 20%. If Zomato maintains its current market share, it could generate revenues of ₹27,000 crore by 2030, assuming the take rate holds steady at 24%.

More importantly, EBITDA could scale 10x from current levels to ₹5,500 crore, driven by operational efficiencies, higher AOVs, and optimised delivery costs.

While the food delivery market in metros is maturing, Tier-2 and Tier-3 cities represent the next frontier for growth. Although these markets come with challenges — lower AOVs and higher delivery costs — they hold immense potential as digital adoption deepens across India.

Zomato’s foray into quick commerce (Q-commerce) through Blinkit is one of the boldest bets in India’s fast-evolving consumption landscape. Q-commerce emerged as a solution to the inefficiencies of traditional grocery delivery, where delayed timelines and fragmented supply chains left much to be desired.

Source: Swiggy’s IPO Filing Document (DRHP)

Source: Swiggy’s IPO Filing Document (DRHP)

Blinkit has taken the market by storm, delivering extraordinary growth, but profitability remains the elephant in the room. The real question is: Can Blinkit transform into a habit-forming, profitable business model?

The growth in Blinkit’s numbers is undeniable.

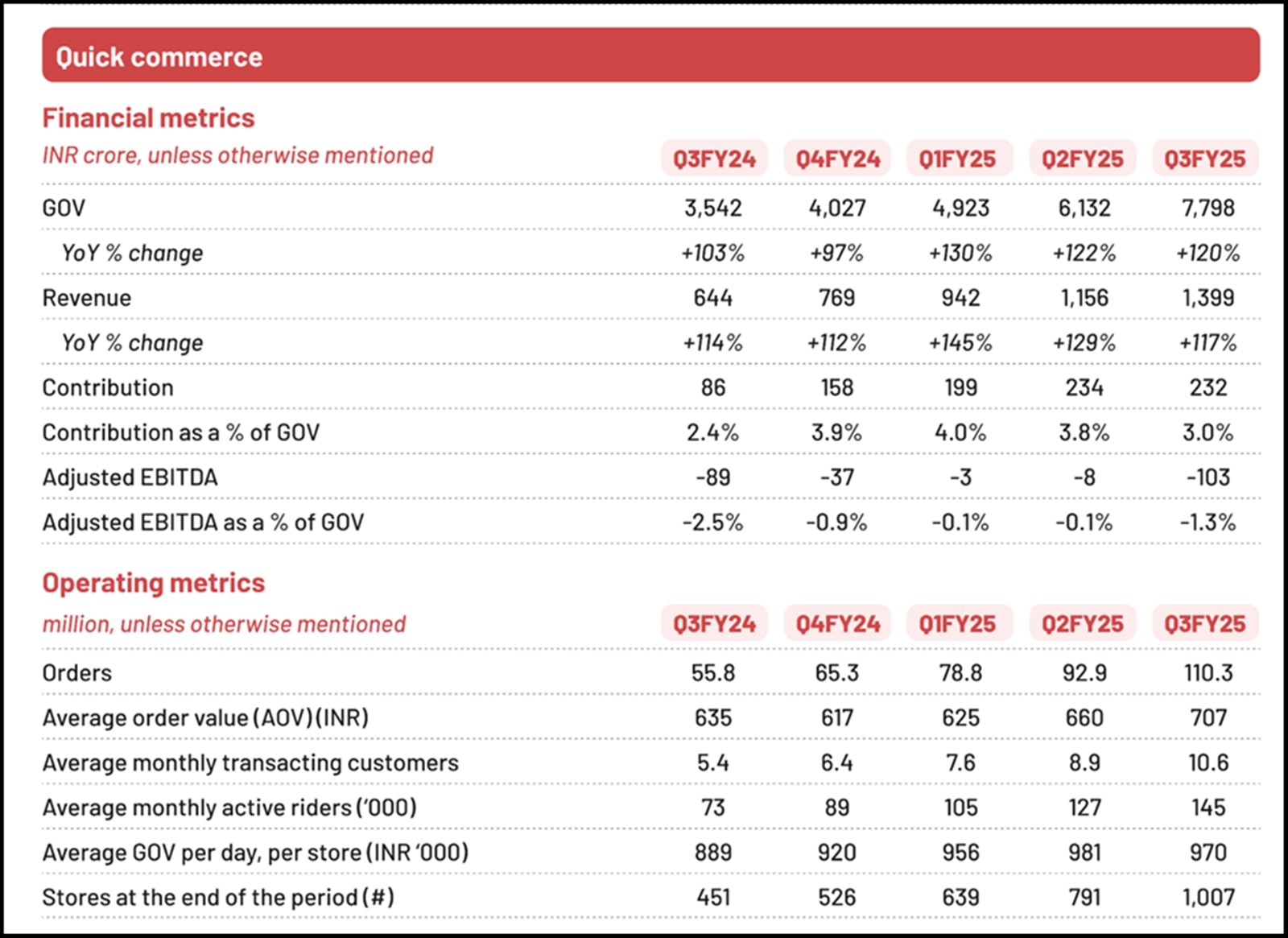

GOV leaped from ₹12,469 crore in FY24 to ₹18,853 crore in just the first nine months of FY25.

By the end of FY25, Blinkit is projected to close the year at nearly ₹26,000 crore in GOV — a remarkable 124% annual growth rate. This trajectory has been powered by an aggressive expansion of dark stores, which serve as the backbone of its operations.

As of Q3FY25, Blinkit had 1,007 dark stores, and the company has already revised its target of reaching 2,000 stores by December 2025 — a full year ahead of earlier guidance.

Source: Zomato’s Q3FY25 Report

Source: Zomato’s Q3FY25 Report

What makes Q-commerce so compelling is its ability to address pain points that traditional grocery delivery could not.

Blinkit has leveraged centralised dark stores, streamlining sourcing and reducing delivery times. This strategy, combined with India’s cost-effective labour market, has enabled it to achieve delivery speeds that were previously unheard of.

Customers not only value speed but are also starting to view Blinkit as a reliable platform for everyday essentials, reinforcing a habit that could drive future growth.

However, it’s not all smooth sailing.

While Blinkit is growing exponentially, profitability remains elusive. Contribution margins have turned positive, meaning the business is covering its variable costs, but adjusted EBITDA remains in the red.

In Q3FY25, the adjusted EBITDA margin stood at -1.3% of GOV, a fall from earlier quarters due to the addition of new stores. While 30% of Blinkit’s stores are already contribution-margin positive and contribute over 50% of GOV, the newer stores are dragging down overall profitability.

Source: Source: Zomato’s Q3FY25 Report

Source: Source: Zomato’s Q3FY25 Report

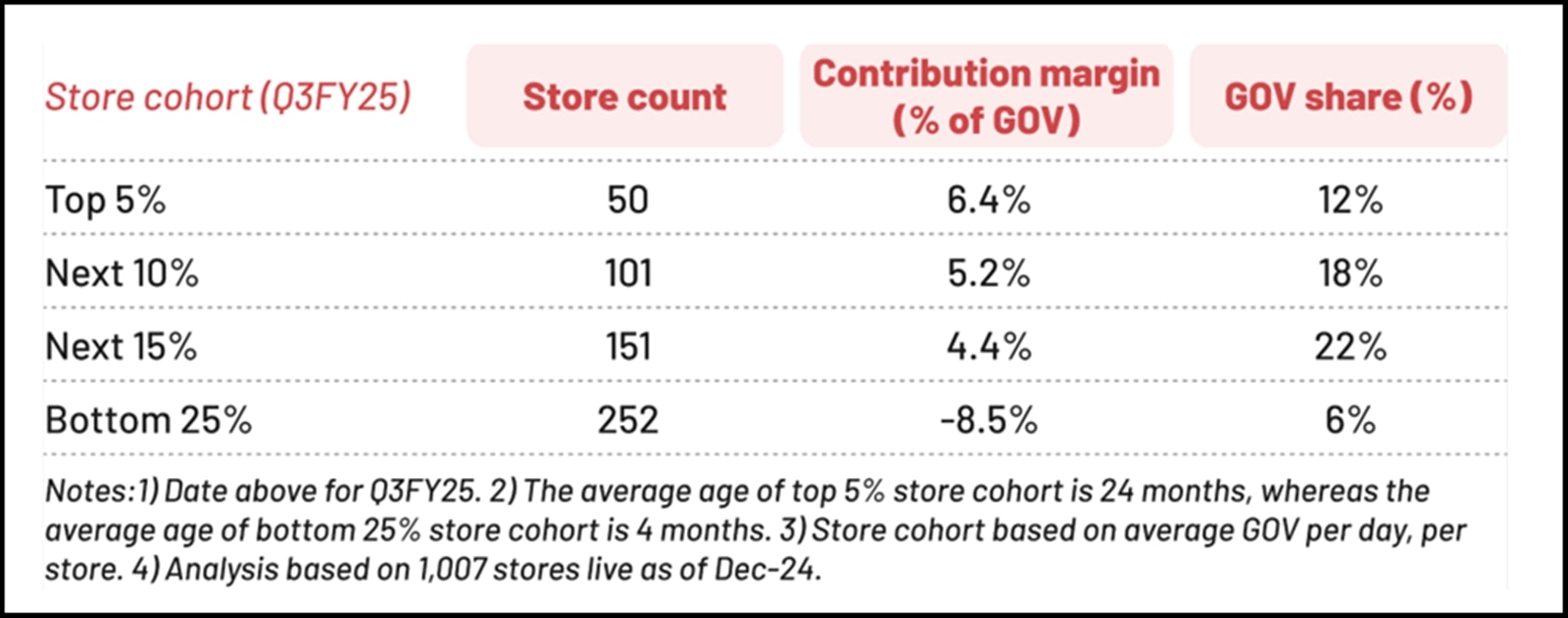

The nuances of Blinkit’s store cohort analysis reveal an interesting pattern.

Older stores are highly profitable, with the top 30% generating 52% of GOV and contribution margins ranging from 4.4% to 6.4%.

These stores have had time to mature, optimise operations, and build a loyal customer base. In contrast, the bottom 25% of stores, which are newer and less established, operate at negative margins of -8.5%. This disparity underscores the challenge of scaling Q-commerce while maintaining financial discipline.

Yet, it also hints at the potential for profitability if newer stores can replicate the performance of older cohorts.

The business’s user metrics further highlight its promise.

Blinkit’s GOV retention rate is an astonishing 144%, meaning that the same users are spending more over time. AOV has risen from ₹625 in Q1FY25 to ₹707 in Q3FY25, signaling that customers are not only ordering frequently but are also placing higher-value orders.

This behavioural shift suggests that Q-commerce is transitioning from a convenience-driven novelty to a deeply ingrained habit.

The competitive landscape, however, is heating up.

While Blinkit and Swiggy Instamart have dominated the market, players like Zepto, Flipkart, Amazon, and Reliance Retail are aggressively entering the fray.

Despite this, Blinkit has managed to outpace its competitors in terms of revenue growth. Its revenues are 2.5x those of Instamart, owing to faster dark store expansion and a more aggressive investment strategy.

But the market is not without limits. HDFC Securities estimates that India can accommodate 7,500 dark stores, and with the top players already operating close to 6,000, the window for new entrants is rapidly closing.

While challenges remain, the road to profitability is not entirely out of reach.

If Blinkit’s existing trends hold — especially its high user retention, rising AOV, and the maturation of newer store cohorts — the business could achieve EBITDA profitability within six to eight quarters. This is a crucial milestone that would solidify Blinkit’s place as a key pillar of Zomato’s ecosystem.

What stands out most is how Blinkit has managed to foster habit formation among its users. With customers returning frequently and spending more, Q-commerce is no longer just a solution to a problem; it is becoming a way of life.

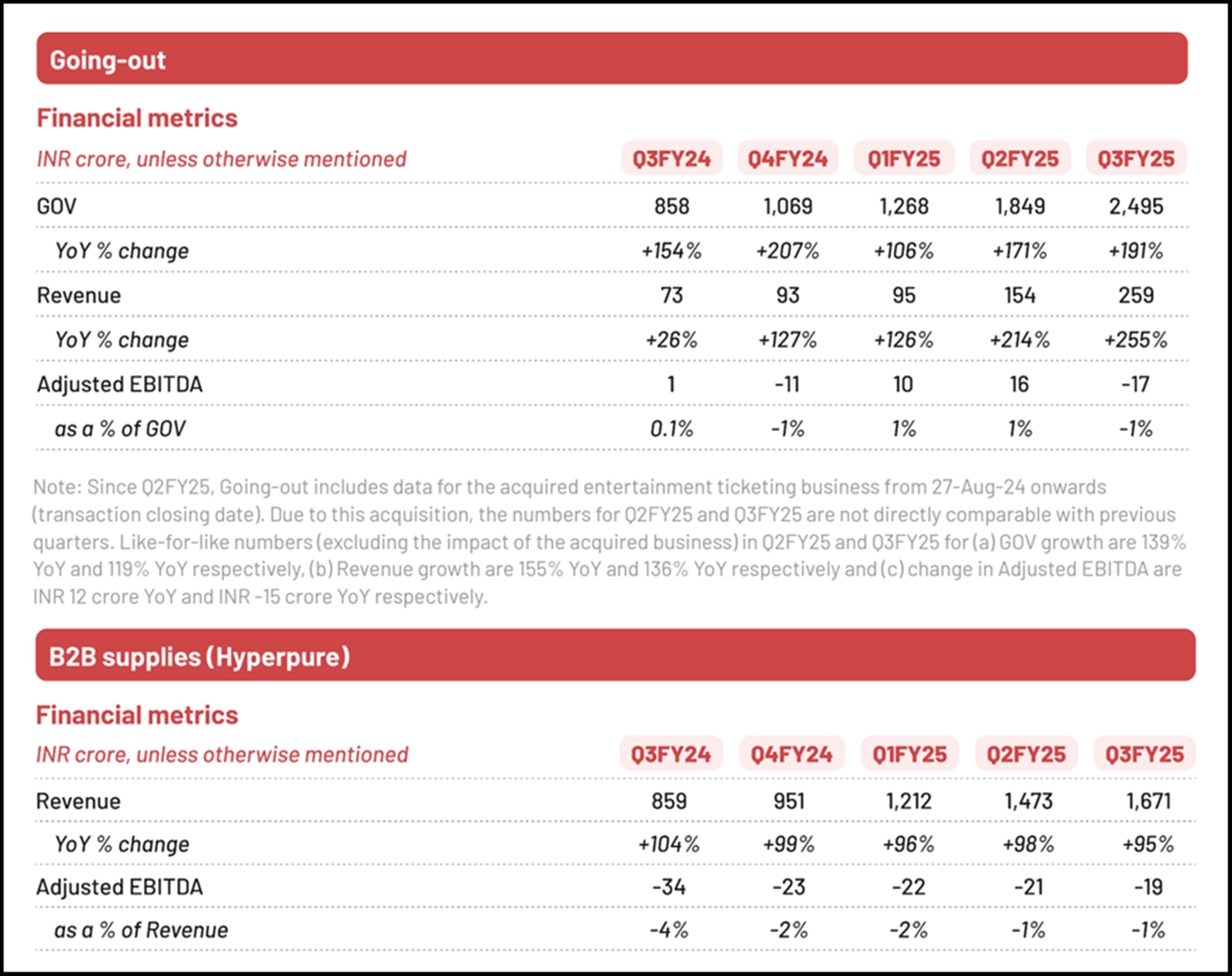

Zomato’s ongoing diversification has extended its reach into two promising verticals — its Going-Out Business and B2B Supplies. While still in their early days, these segments hold unique potential to create complementary ecosystems around Zomato’s core food delivery platform.

Launched in November 2024, the District app is Zomato’s bold attempt to consolidate India’s fragmented going-out market.

By integrating services like dining-out, event ticketing, and entertainment discovery under a single platform, Zomato hopes to redefine how Indians engage with nightlife and cultural events. Early signs are promising, with over 6.5 million downloads within weeks of launch.

This initiative, however, comes with significant challenges.

As Zomato transitions its going-out customers from platforms like Paytm, Insider, and TicketNew to District, the focus remains on seamless user migration and improved engagement.

The company aims to expand the platform’s selection, bringing world-class experiences to Indian audiences while ensuring smooth discovery through intuitive tech.

The financials tell a story of rapid growth paired with heavy investment.

In Q3FY25, the going-out vertical generated a GOV of ₹2,495 crore, marking a 191% YoY increase. Revenue for the segment jumped 255% YoY to ₹259 crore. However, adjusted EBITDA fell to ₹-17 crore for the quarter, driven by expenses related to District’s development, marketing, and team expansion.

While profitability is not expected in the near term, the core going-out business remains profitable outside of these investments. Zomato is betting that the enhanced customer experience on District will pay dividends over time, establishing it as a one-stop destination for all going-out activities in India.

Zomato’s Going-out, Hyperpure Business. (Source: Zomato’s Q3FY25 Report)

Zomato’s Going-out, Hyperpure Business. (Source: Zomato’s Q3FY25 Report)

Zomato’s B2B Supplies business has a simpler narrative: it exists to support restaurants, primarily by providing essential goods and services.

As India’s restaurant landscape grows, this vertical naturally benefits from increased demand for kitchen supplies, raw materials, and operational tools.

Although it is unlikely to rival the scale of Zomato’s other businesses, B2B supplies play a vital role in strengthening the company’s relationship with restaurants. By streamlining procurement, Zomato helps its partners reduce costs, improve efficiency, and focus on delivering quality dining experiences.

This symbiotic relationship not only bolsters the restaurant ecosystem but also reinforces Zomato’s position as a key enabler in the food industry.

For now, the segment is expected to remain small but resilient. Its growth will mirror the rise of new restaurants, making it a complementary, if understated, part of Zomato’s overall strategy.

Zomato’s current market capitalization hovers around ₹2 lakh crore after a recent rerating over the past two weeks.

With a Price-to-Sales (P/S) ratio of approximately 9x based on trailing 12-month revenue, the stock is trading at a premium compared to global peers in the food and delivery space. This premium is largely driven by Zomato’s strong market share in food delivery (55%), its leadership in quick commerce through Blinkit, and its ability to sustain revenue growth even as competition intensifies.

For FY24, Zomato reported total revenue of ₹13,545 crore, representing a 56% YoY growth. Analysts project revenues to surpass ₹25,000 crore by FY26, driven by continued expansion in food delivery and quick commerce.

Assuming Zomato maintains its current valuation multiple, the market capitalization could see a potential upside of 50% from current levels, driven by its strong growth trajectory and expanding verticals.

However, profitability remains the key concern.

While the company’s adjusted EBITDA turned positive for its core food delivery business, the heavy investments in Blinkit and the District app have weighed on consolidated profitability.

Blinkit, for instance, is projected to achieve EBITDA profitability within the next six to eight quarters, with an expected revenue contribution of over ₹20,000 crore by FY30. Similarly, the going-out business is poised to grow at a 40%+ CAGR over the next few years, albeit with near-term losses as District scales.

With a strong balance sheet and no immediate need for additional capital, Zomato is well-positioned to fund these expansions. However, the transition from growth to profitability will require disciplined execution. Any misstep — whether in scaling new verticals or maintaining customer loyalty in food delivery — could weigh heavily on the stock’s valuation.

Zomato’s story is one of transformation and ambition.

It has successfully diversified its business while maintaining leadership in its core operations. The company’s focus on creating an integrated ecosystem, combined with its strong execution track record, makes it an exciting prospect for growth-oriented investors.

However, the stock’s premium valuation leaves little room for error.

While the long-term growth potential is evident, the journey to sustainable profitability and the ability to fend off intensifying competition will determine its ultimate success. Investors should weigh the growth opportunities against the execution risks and consider their own risk tolerance before making any decisions.

As Zomato navigates its next phase of growth, it remains a company to watch — both for its strategic moves and its ability to redefine India’s digital consumption landscape.

Note: We have relied on data from the annual reports throughout this article. For forecasting, we have used our assumptions.

Parth Parikh has over a decade of experience in finance and research, and he currently heads the growth and content vertical at Finsire. He has a keen interest in Indian and global stocks and holds an FRM Charter along with an MBA in Finance from Narsee Monjee Institute of Management Studies. Previously, he has held research positions at various companies.

Disclosure: The writer and his dependents do not hold the stocks discussed in this article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary