Journalism of Courage

The second quarter earnings season could throw up sharply divergent trends in earnings. While export-driven sectors are seen benefitting from the depreciation in the rupee,domestic demand-driven sectors and heavily indebted companies may sink further in terms of performance.

While the aggregate financial performance of India Inc during the quarter ending September 2013 may be helped by export-driven sectors,earnings downgrades for FY14 and maybe even FY15 are more than likely,say analysts.

For IT,healthcare and metal companies,earnings may be supported by a year-on-year (y-o-y) fall of 12.5% in the rupee along with a pick-up in global growth,say analysts.

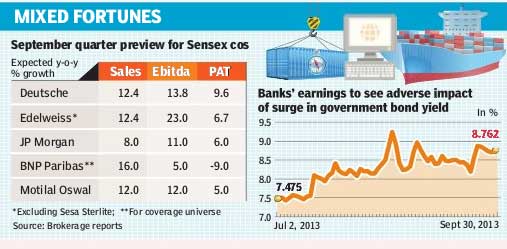

Global recovery and rupee depreciation are set to be the strong over-riding catalysts driving a rebound in revenues, said Deutsche Bank in an earnings preview report. The foreign brokerage expects y-o-y top line growth of 12.4% for Sensex companies and 16.9% for its coverage universe of 105 companies for the September quarter.

Edelweiss and Motilal Oswal Securities also expect the September quarter revenue growth of Sensex companies near 12%,compared with last year,while JPMorgan is looking at a moderate rise of 8%.

Among bluechips,recent stock outperformers like Sun Pharma,Tata Consultancy Services (TCS) and Tata Motors are seen driving Sensex earnings.

Analysts appear particularity upbeat over Tata Motors,which realises nearly 75% of its consolidated revenues from its global operations,even as the auto major’s domestic commercial vehicle business is expected to slowdown further.

Analysts expect Tata Motors to report strong profits on the back of a 21-25% sales growth based on strong performance at the Jaguar Land Rover (JLR) unit.

For FMCG companies,while quarterly earnings are expected to be steady,the Street is expecting volume growth to trend lower,especially in the discretionary categories. While Tata Global beverages and Marico may post strong profit growth,volume growth at Hindustan Unilever and ITC is seen softening further.

The big drag on second quarter profitability is seen coming from the banking,capital goods and telecom sectors. Besides a challenging economic environment that has pushed up non-performing assets across the banking sector,a sudden rise in bond yields during the quarter on account on liquidity tightening measures from the RBI are expected to hit investment portfolios and therefore,net earnings of banks.

The quarter could also see margins coming under pressure due to higher input costs stemming from a weaker rupee. Higher interest costs could also take a toll on the net profits of Indian companies. As a result,downgrades are likely to persist during the earnings season.

According to BNP Paribas,though consensus estimates showed an improvement in the recent past due to the weakening rupee,the trend of downgrades is likely to return.

Since the medium-term direction of the market tends to be governed by the direction of earnings estimates,and at a 14.1x FY14E consensus PE and 2.2x P/BV (10-15% discounts to long-term averages),the risk of earnings downside does not seem fully factored in, it observed in a note.

However,JPMorgan believes that the linkage between the earnings growth expectations and equity market performance has weakened considerably since late 2012. It anticipates further downward revision to the consensus FY14 earnings outlook of 10% growth due to weaker performance in the September quarter.

That said,we believe weak corporate performance may itself not precipitate a sharp sell-off in equity markets, adds the brokerage house in a recent report.