© IE Online Media Services Pvt Ltd

Journalism of Courage

While IGI has always been a dominant player in natural diamond certification, its biggest growth engine in recent years has been LGDs. (IGI India website)

While IGI has always been a dominant player in natural diamond certification, its biggest growth engine in recent years has been LGDs. (IGI India website)Whether it’s a wedding, an investment, or just a fashion statement, jewellery has always been an emotional and financial asset for Indians. But beyond tradition, lie the numbers, which tell a bigger story.

India makes up 20% of the global jewellery market, and it’s growing at a rapid 11-13% CAGR, making it one of the biggest and fastest-expanding consumer bases worldwide. While gold has historically dominated, diamonds, especially lab-grown diamonds (LGDs), are now making inroads.

Figure 1: Consumption of jewellery by top countries. (Source: IGI DRHP)

Figure 1: Consumption of jewellery by top countries. (Source: IGI DRHP)

However, unlike gold, where pricing is transparent and purity is standardised, buying diamonds is an entirely different game. Prices can vary significantly based on cut, clarity, and whether the diamond is natural or lab-grown.

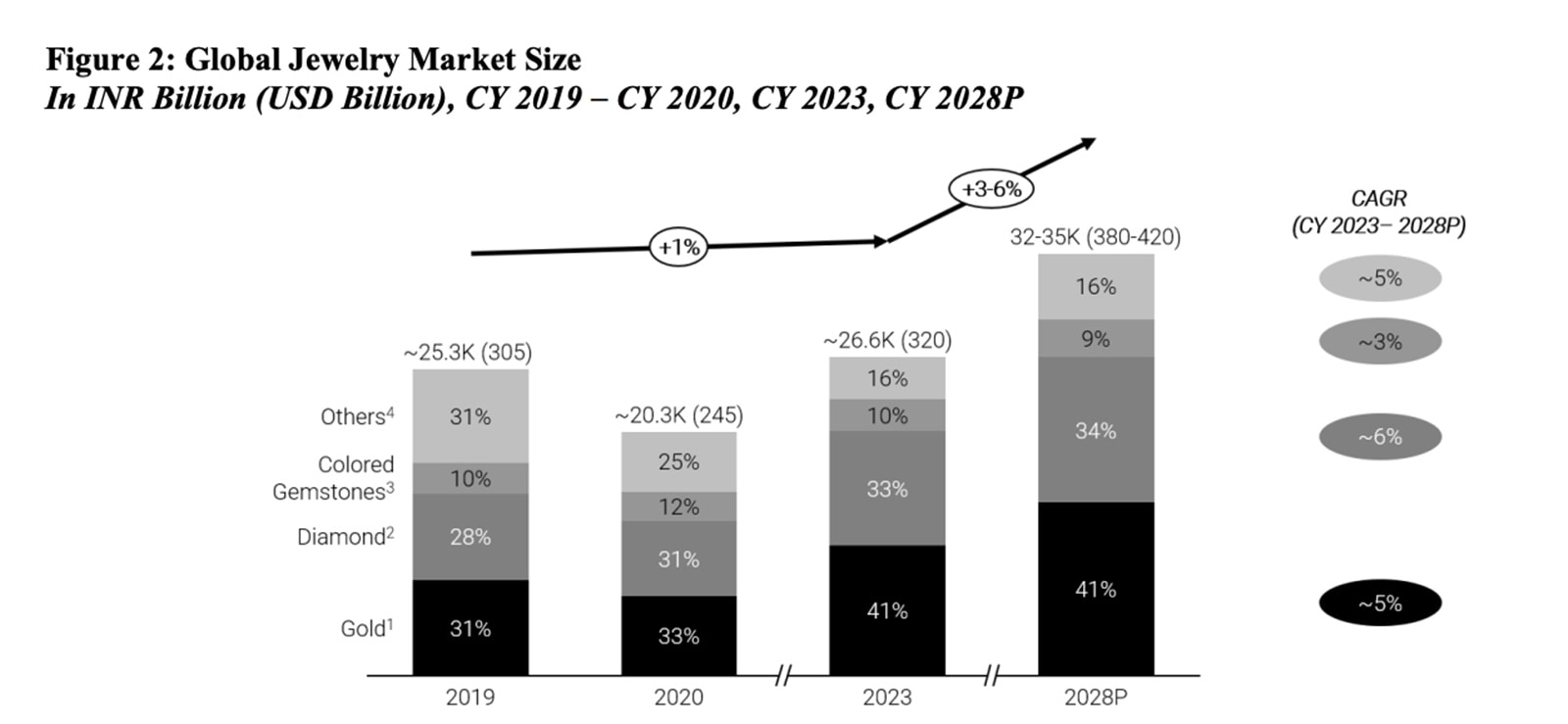

Figure 2: Global Jewellery Market Size. (Source: IGI DRHP)

Figure 2: Global Jewellery Market Size. (Source: IGI DRHP)

This creates a massive trust gap in the market, where consumers struggle to understand whether they are getting a fair deal.

That’s exactly where IGI (International Gemological Institute) comes in.

IGI holds 65% of the LGD certification market, 42% of the studded jewellery certification market, and a 50% market share in India’s overall diamond certification industry.

In simple terms, if someone is buying a certified diamond in India, there’s a high chance IGI had a role in verifying it. What makes IGI different from jewellery retailers like Titan or Kalyan Jewellers is that it doesn’t need to sell jewellery to make money. Instead, it earns from every piece that requires authentication — whether it’s a Rs 50,000 solitaire or a Rs 50 lakh necklace.

But the real game-changer for IGI is LGDs.

LGDs are growing at an explosive 22% CAGR, and their affordability has made them a hit, especially in the US, which accounts for 80-90% of global LGD demand. This trend has been a windfall for IGI, with LGD certification jumping from 35% of its revenue in 2021 to 59% in 2024.

The big question now is: Can IGI continue riding this wave? If LGDs keep growing and certification remains essential, IGI could be one of the smartest ways to play in India’s jewellery boom. But if LGDs become mass-market fashion accessories with fewer buyers demanding certification, the company’s growth could hit a ceiling. With its strong market position and high-margin business, IGI offers an interesting alternative to traditional jewellery investments.

But is there enough upside left, or has the stock already priced in the opportunity?

That’s what we need to find out.

Diamonds aren’t just luxury items; they are a global industry worth billions of dollars, built on perception, exclusivity, and, most importantly, trust.

Unlike gold, where purity is measured in karats and prices are standardised, diamonds are far more complex. Two stones that appear identical to the naked eye can have vastly different values based on cut, clarity, colour, and carat weight — collectively known as the 4Cs of diamonds.

Figure 3: 4Cs of Diamond. (Source: IGI DRHP)

Figure 3: 4Cs of Diamond. (Source: IGI DRHP)

For most buyers, especially those unfamiliar with the intricacies of diamond valuation, the biggest concern is whether they are getting a fair deal or being overcharged. This is where certification becomes critical. A third-party certification not only verifies a diamond’s authenticity but also assigns it a grade that determines its market value. It acts as a seal of trust between the seller and the buyer.

But here’s the catch — not all diamond certification bodies are created equal. Some are internationally accepted, while others hold little credibility. Over time, two organisations have dominated this space: IGI (International Gemological Institute) and GIA (Gemological Institute of America). These two institutions control nearly 80% of the global diamond certification market, making them the de facto authorities in the industry.

Imagine you’re buying a one-carat diamond ring. You see two seemingly identical diamonds — one priced at Rs 3 lakh, the other at Rs 5 lakh.

Why the difference? The answer lies in grading. Even a small variation in clarity, cut, or colour can push a diamond’s price up or down by 20-50%. Certification ensures that consumers are paying for what they’re actually getting, rather than relying solely on a seller’s claims.

And then there’s the issue of natural versus lab-grown diamonds. Lab-grown diamonds are chemically identical to natural ones, making it nearly impossible for an untrained eye (or even many jewellers) to tell the difference.

Without certification, a buyer could unknowingly pay natural diamond prices for an LGD. Given that natural diamonds can cost 3-5 times more than their lab-grown counterparts, this makes certification even more essential.

This is why IGI has built a business that isn’t just necessary but indispensable to the entire diamond ecosystem. It ensures transparency in pricing, maintains confidence in transactions, and ultimately makes sure buyers and sellers are on the same page.

Building a certification business isn’t like starting a new jewellery brand — it’s a game of credibility and legacy. You can’t just set up a lab and start grading diamonds overnight.

IGI has been in the business for over 45 years, making it one of the oldest and most recognised certification bodies worldwide. Jewellers, wholesalers, and retailers trust IGI-graded diamonds because they know that its grading standards are consistent and globally accepted. For a new competitor to challenge IGI’s dominance, it would take years, if not decades, of trust-building, scientific validation, and industry adoption.

Retailers also prefer to work with a well-established certifier because they know customers recognise and trust these certificates. If a jeweller tried to sell a diamond certified by an unknown company, buyers would likely hesitate, leading to lost sales and lower trust in the brand.

This is what gives IGI a competitive edge that is difficult to replicate.

While IGI has always been a dominant player in natural diamond certification, its biggest growth engine in recent years has been LGDs. It was one of the first certification bodies to start grading lab-grown diamonds in 2005, long before they became widely accepted.

This early adoption has paid off massively. Today, IGI holds a 65% market share in the LGD certification segment, making it the undisputed leader in a category that is growing at a 22% CAGR from 2023 to 2028.

LGDs have been reshaping the diamond industry because they are:

📌 More affordable (costing 60-70% less than natural diamonds)

📌 Ethically sourced (no concerns about “blood diamonds”)

📌 Chemically identical to natural diamonds

But the big challenge with LGDs is that many consumers still don’t fully understand them. Since they look and feel just like natural diamonds, certification becomes even more important to differentiate the two categories. IGI’s dominance in this segment means that as LGDs continue to gain popularity, its revenue from certification will keep rising.

Already, LGD certification has become IGI’s biggest revenue driver, accounting for 59% of its total revenue in 2024, up from just 35% in 2021. And with 12 million LGDs expected to be certified annually by 2028, this segment is expected to power IGI’s next growth phase.

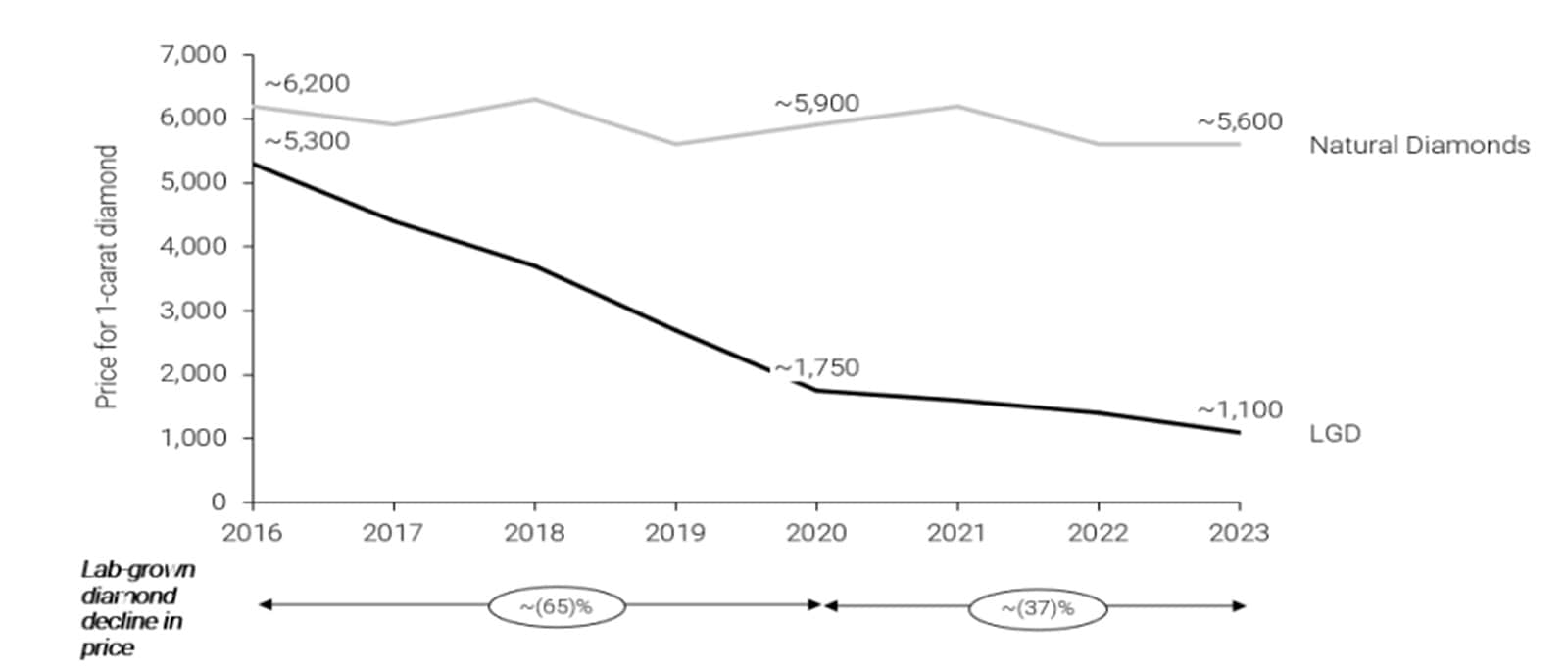

Figure 4: Retail Pricing Benchmark of LGD vs Natural Diamonds In USD. (Source: IGI DRHP)

Figure 4: Retail Pricing Benchmark of LGD vs Natural Diamonds In USD. (Source: IGI DRHP)

One of the biggest advantages of being a market leader in a duopoly is that you control pricing. Since IGI competes with only a handful of major players (primarily GIA), it has the ability to charge premium rates for certification without facing significant price pressure.

This is reflected in its strong financial performance: EBITDA margins are expected to grow from 54.6% in 2024 to 58.8% in 2028 (as per analyst estimates), highlighting how profitable the business is. Certification costs are negligible compared to the value of a diamond, meaning buyers don’t resist paying for it.

Since IGI doesn’t deal in inventory (it only certifies diamonds), it has no exposure to commodity price fluctuations, unlike jewellery brands.

In essence, IGI runs an asset-light, high-margin business where demand is structurally built into the industry itself.

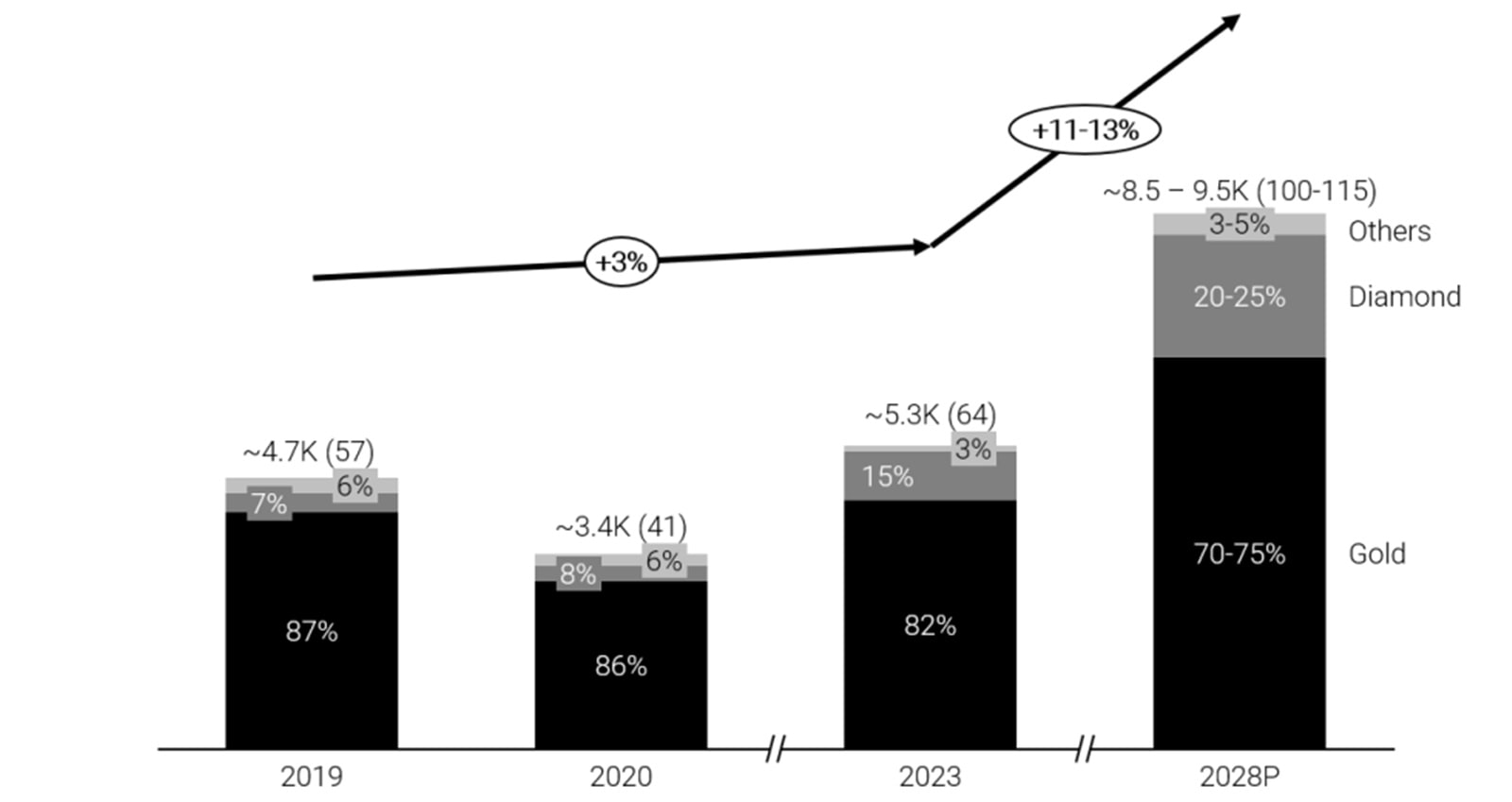

Figure 5: Indian Jewelry Market Size – by Value. (Source: IGI DRHP)

Figure 5: Indian Jewelry Market Size – by Value. (Source: IGI DRHP)

IGI’s dominance isn’t just global — it is also deeply rooted in India, the world’s largest diamond processing hub. India cuts and polishes 95% of the world’s diamonds, making it a natural headquarters for IGI’s operations. The company holds a 50% market share in India’s diamond certification industry, and nine of the top 10 jewellery chains in the country work with IGI.

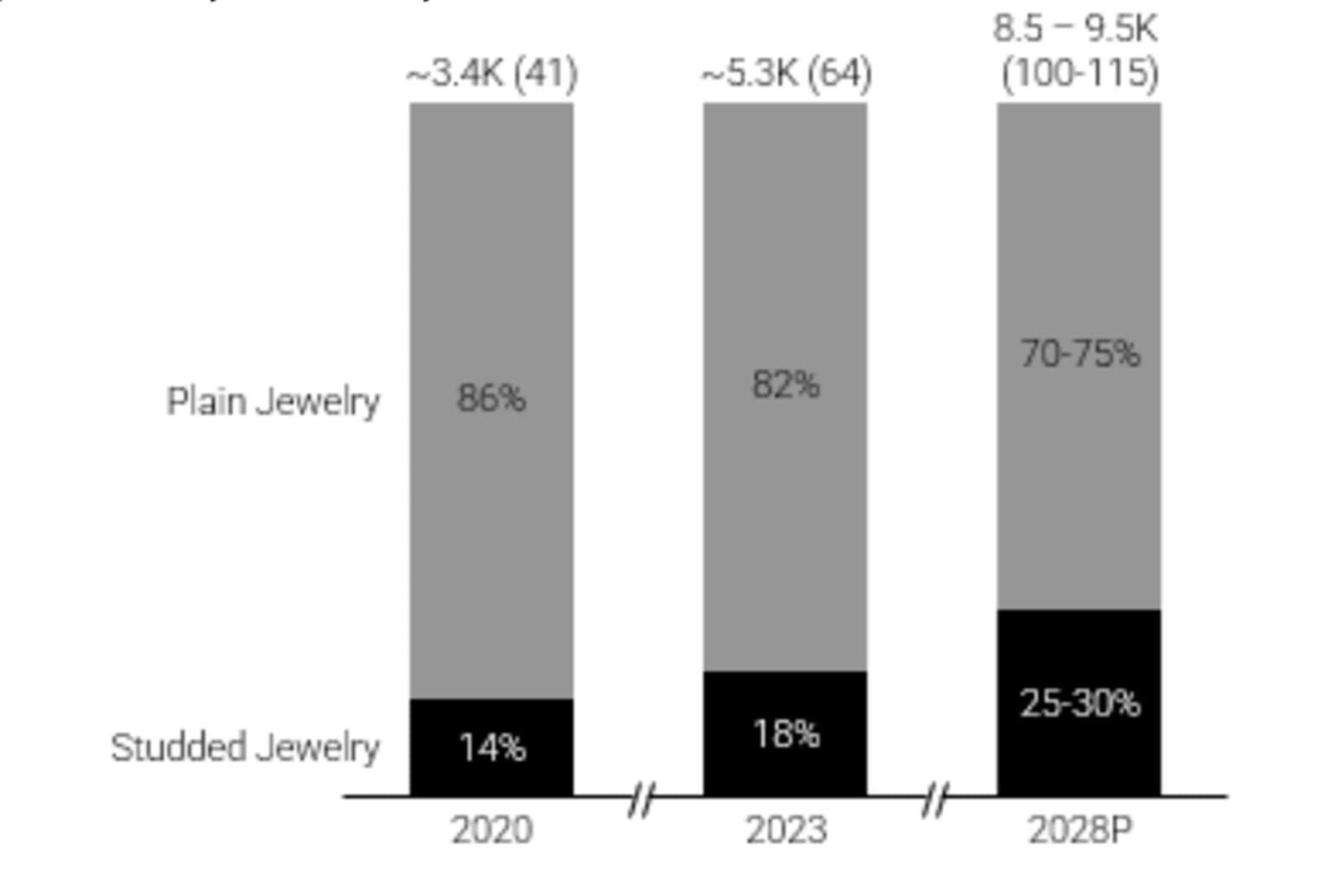

Figure 6: Indian Jewelry Market Size – by Studded vs Plain Jewelry. (Source: IGI DRHP)

Figure 6: Indian Jewelry Market Size – by Studded vs Plain Jewelry. (Source: IGI DRHP)

To further cement its leadership, IGI is investing in ‘IGI Island’, a 214,000 sq. ft. state-of-the-art facility in Surat, which will allow it to expand certification capacity and strengthen its research capabilities.

With India’s jewellery market growing at 11-13% CAGR, IGI’s market share in the country is only expected to increase further.

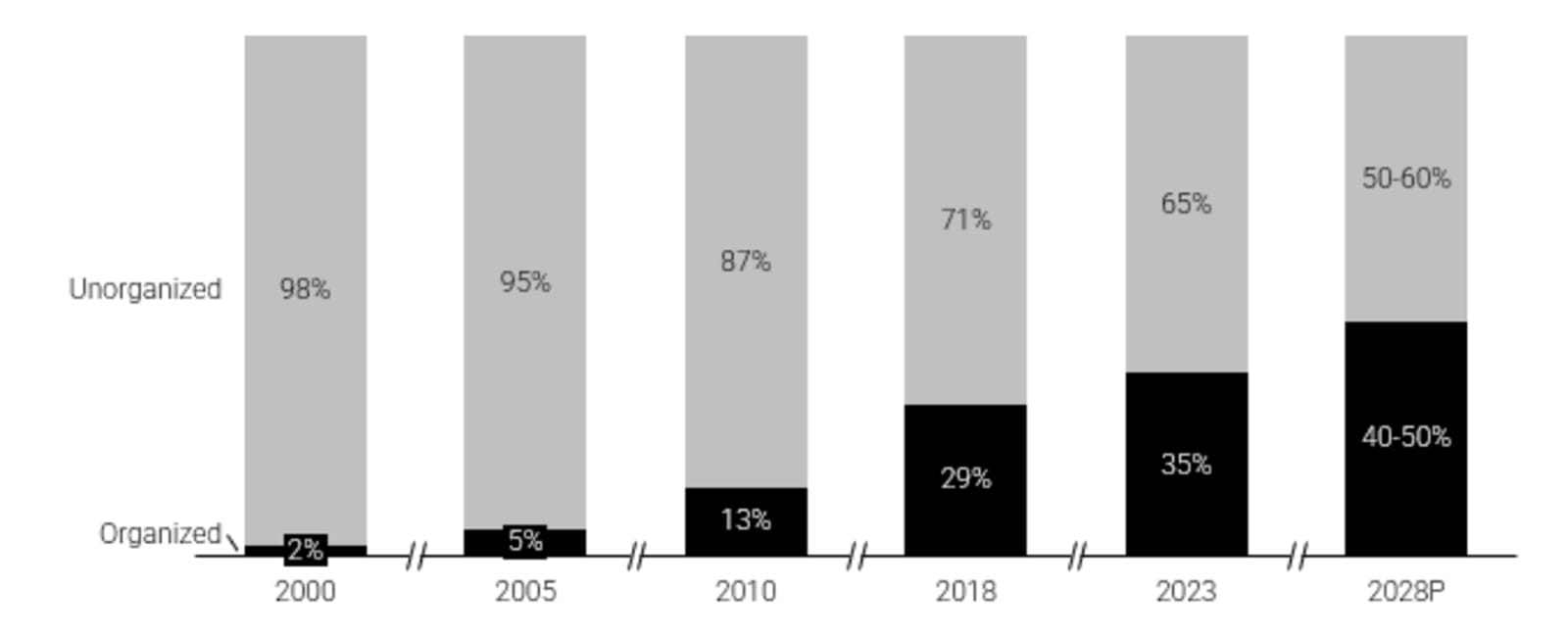

Figure 7: Indian Jewelry Market by Market Structure. (Source: IGI DRHP)

Figure 7: Indian Jewelry Market by Market Structure. (Source: IGI DRHP)

IGI has built a business that is fundamental to the diamond industry. Whether it’s natural diamonds, LGDs, or studded jewellery, every transaction that involves certification contributes to IGI’s revenue. Unlike jewellery brands that rely on consumer spending cycles, IGI benefits from consistent and recurring certification demand.

Its high margins, duopoly position, and strong pricing power make it one of the most resilient and profitable businesses in the diamond ecosystem.

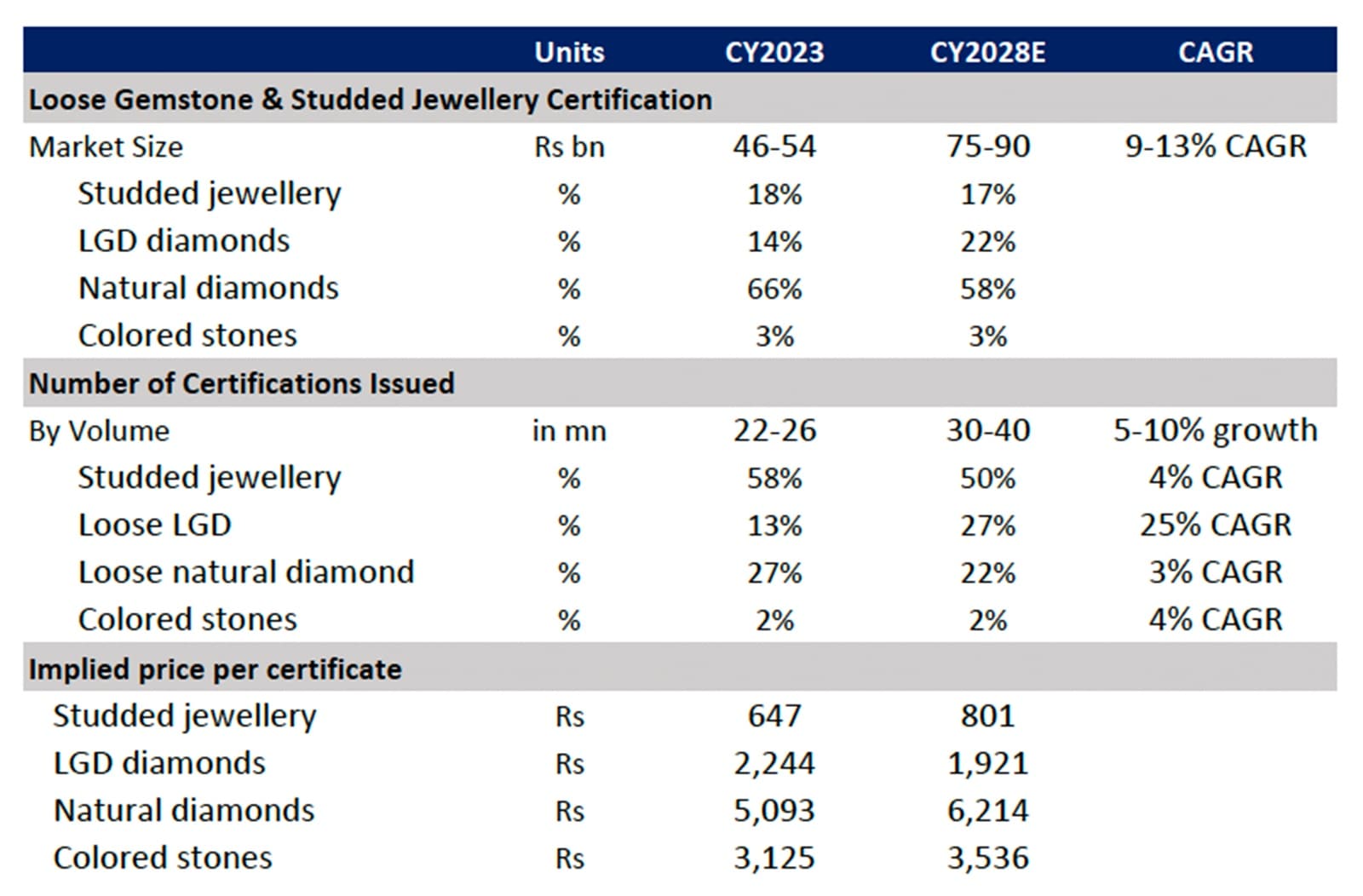

Figure 8: Implied price per certificate. (Source: Morgan Stanley Research)

Figure 8: Implied price per certificate. (Source: Morgan Stanley Research)

However, the real test will be how LGDs evolve. If they continue gaining mainstream acceptance, IGI’s certification volumes will surge, driving revenue growth. But if LGDs become mass-market fashion accessories, the need for certification may decline over time.

For now, IGI remains one of the strongest and most underappreciated players in the jewellery industry. It profits from every diamond transaction, without carrying any inventory risk. And that’s a rare and valuable moat.

IGI isn’t just another company in the jewellery ecosystem — it’s the invisible but essential player that sits at the heart of every diamond transaction. It doesn’t matter whether someone is buying a natural solitaire, a diamond-studded necklace, or a LGD — if it’s certified, IGI is likely involved. And that’s exactly what makes its financial story so compelling. Unlike jewellers who are exposed to changing fashion trends, commodity prices, and inventory risk, IGI runs an asset-light, high-margin business that thrives on trust and standardisation.

Right now, the company is in the middle of a strong growth phase. But where exactly is this growth coming from? The answer lies in three major trends shaping the industry.

If there’s one segment that’s driving IGI’s business forward, it’s LGDs. Just a few years ago, LGDs were a niche category, accounting for only 35% of IGI’s revenue in 2021. But since then, things have changed drastically.

Today, LGD certification makes up 60% of IGI’s revenue, and it’s growing at more than 50% CAGR. Lab-grown diamonds are expected to contribute significantly to IGI’s total certification revenue, making it the company’s biggest growth driver.

Why? Because LGDs are fundamentally changing how people buy diamonds. They are:

📌 Far more affordable than natural diamonds (costing 60-70% less).

📌 Ethically sourced with no concerns about conflict diamonds.

📌 Visually and chemically identical to natural diamonds, making certification even more critical.

Figure 9: Revenue Split across Segments. (Source: IGI DRHP)

Figure 9: Revenue Split across Segments. (Source: IGI DRHP)

But here’s the catch — LGDs need certification even more than natural diamonds. Since they look and feel exactly the same, consumers need third-party verification to differentiate between the two. That’s where IGI has locked in its advantage.

With a 65% market share in LGD certification, it is the go-to name for authenticity in this fast-growing segment.

This is the reason why 12 million LGDs are expected to be certified annually by 2028. And every single one of those requires IGI (or GIA) to step in.

While LGDs are stealing the spotlight, natural diamonds still form the backbone of IGI’s business. Unlike LGDs, which are growing rapidly, the natural diamond market is mature and growing at a modest 14% CAGR.

But that doesn’t mean it’s slowing down. Certification is a mandatory part of that process, ensuring that IGI has a steady flow of business, regardless of global economic conditions.

More importantly, natural diamonds still hold premium value, especially in luxury markets. Whether it’s a high-end engagement ring in the US or a custom-crafted piece from an Indian jeweller, consumers demand certification to validate their purchase. IGI’s dominance in this segment means it benefits from both high-volume mass-market sales and ultra-premium diamonds requiring top-tier grading.

Beyond diamonds, IGI has a steady stream of revenue from studded jewellery and coloured stones (rubies, sapphires, emeralds, etc.). While this segment isn’t growing as fast, it still contributes 27% of total revenue and is expected to grow at a 3% CAGR.

The reason? While individual diamond sales can be cyclical, jewellery sales as a whole remain steady, driven by weddings, gifting, and long-term wealth preservation. As long as people continue to buy jewellery, IGI will continue certifying it.

Here’s what makes IGI’s growth story even more impressive — it’s not just about revenue; it’s about margins.

Unlike jewellers who need to worry about gold price fluctuations, inventory management, and customer demand, IGI runs a pure service-based business. That means:

✅ No inventory risk. IGI doesn’t own or sell diamonds, it only certifies them.

✅ No raw material costs. Unlike jewellers, IGI’s expenses aren’t tied to commodity prices.

✅ Recurring revenue model. Every new diamond or jewellery piece that gets sold needs certification.

As a result, EBITDA margins are projected to increase from 55.2% in CY23 to close to 60% in CY28. That’s a huge margin profile for a business of this size, putting IGI in the same category as some of the most profitable financial and analytics firms.

Figure 10: Margin Profile. (Source: IGI DRHP)

Figure 10: Margin Profile. (Source: IGI DRHP)

What’s more, pricing power remains strong. Since IGI operates in a duopoly with GIA, it can charge premium rates for certification services without much competitive pressure. Unlike industries where companies are forced to slash prices to compete, IGI has long-term pricing stability, which protects its profitability.

At ~55x CY25 earnings, IGI’s valuation places it alongside high-margin, niche financial and analytics service businesses. The company’s asset-light model, industry positioning, and role in certification services contribute to its premium multiple. However, whether this valuation remains sustainable depends on how IGI’s business model compares to similar companies, its ability to maintain pricing power, and industry demand for certification services over time.

The closest comparables for IGI are CRISIL, CAMS, and Kfin Technologies, all of which operate in industries where trust, certification, and verification services are crucial. These companies, like IGI, benefit from recurring revenue, limited direct competition, and strong pricing power due to the critical nature of their services.

CRISIL, which operates in credit ratings and risk assessment, trades at 50-55x earnings due to its strong market positioning and regulatory importance.

CAMS (Computer Age Management Services), which provides mutual fund registrar services, trades at 35-40x earnings, reflecting its recurring revenue model and essential role in India’s financial ecosystem.

Kfin Technologies, which operates in fund management and data administration, trades at 45-50x earnings, though its multiple fluctuates due to evolving competition in its segment.

IGI shares several characteristics with these businesses — high-margin services, limited reliance on commodity cycles, and a business model built on standardisation and reputation rather than volume growth. However, one key difference is that CRISIL, CAMS, and Kfin operate in financial services, where regulation often creates artificial demand, whereas IGI’s business relies on consumer preference for certification.

Morgan Stanley also recently initiated coverage on IGI with ~15% upside, suggesting that the stock is largely fairly valued, with some potential for further gains. This implies that while IGI benefits from strong industry positioning, further re-rating would depend on the pace of international expansion, pricing power in LGD certification, and sustained demand for third-party verification services.

Note: This is not a prediction of where the stock price could head. It’s just an if-then calculation for academic purposes.

While IGI has built a moat around trust and credibility, certain risks could impact its long-term growth trajectory.

The biggest uncertainty in IGI’s future is how the LGD market develops. Right now, LGDs are gaining acceptance as an alternative to natural diamonds, but if consumer perception shifts and they are treated as disposable fashion jewellery, the demand for certification could decline. Certification is crucial when buyers perceive a diamond as an investment; however, in a world where LGDs are mass-produced at lower costs, buyers may not feel the need for third-party validation.

While IGI currently dominates LGD certification, GIA is making aggressive moves to capture more of this segment. If GIA starts pricing certifications lower or introduces new differentiation strategies, IGI may lose some of its pricing power. Given that certification services are not a volume-driven business but a margin-driven one, even small pricing adjustments could impact IGI’s profitability in the long run.

IGI’s core business in India is highly profitable, but its international operations, particularly in Belgium and the US, are still evolving. IGI Belgium has struggled with profitability, recording negative EBITDA margins in 2023 (-14.5%), though there are expectations of a turnaround by 2028. If IGI fails to expand its certification footprint in key global markets, revenue diversification could be impacted, leading to overdependence on India and Asia.

While IGI is somewhat insulated from direct consumer spending trends, the jewellery market remains cyclical. A slowdown in discretionary spending due to macroeconomic conditions could indirectly impact certification volumes, particularly in the luxury segment of natural diamonds. IGI’s business model is robust, but it still relies on a healthy demand for certified diamonds and jewellery worldwide.

At current valuations, market expectations already reflect IGI’s strong financial performance and future growth prospects. The company’s ability to maintain its pricing power, expand in international markets, and sustain growth in LGD certification will be key factors influencing its trajectory. Investors will likely monitor how competition, certification pricing, and consumer trends in diamonds evolve before making long-term investment decisions.

For now, IGI’s role as a critical enabler in the diamond ecosystem remains clear, but its future valuation will depend on how well it executes its growth strategy in an evolving market.

Note: We have relied on data from the annual report and industry reports for this article. For forecasting, we have used our assumptions.

Parth Parikh has over a decade of experience in finance and research, and he currently heads the growth and content vertical at Finsire. He has a keen interest in Indian and global stocks and holds an FRM Charter along with an MBA in Finance from Narsee Monjee Institute of Management Studies. Previously, he has held research positions at various companies.

Disclosure: The writer and his dependents do not hold the stocks discussed in this article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.