© The Indian Express Pvt Ltd

Journalism of Courage

Listed in November 2023, Blue Jet Healthcare saw its stock remain stagnant for six months before surging from June 2024. (Photo: bluejethealthcare.com)

Listed in November 2023, Blue Jet Healthcare saw its stock remain stagnant for six months before surging from June 2024. (Photo: bluejethealthcare.com)India is rightly called the pharmacy of the world. It supplies 60% of the world’s vaccines, 40% of generic drugs in the US, 50% of Africa’s generic drugs, and 25% of medicines in the UK.

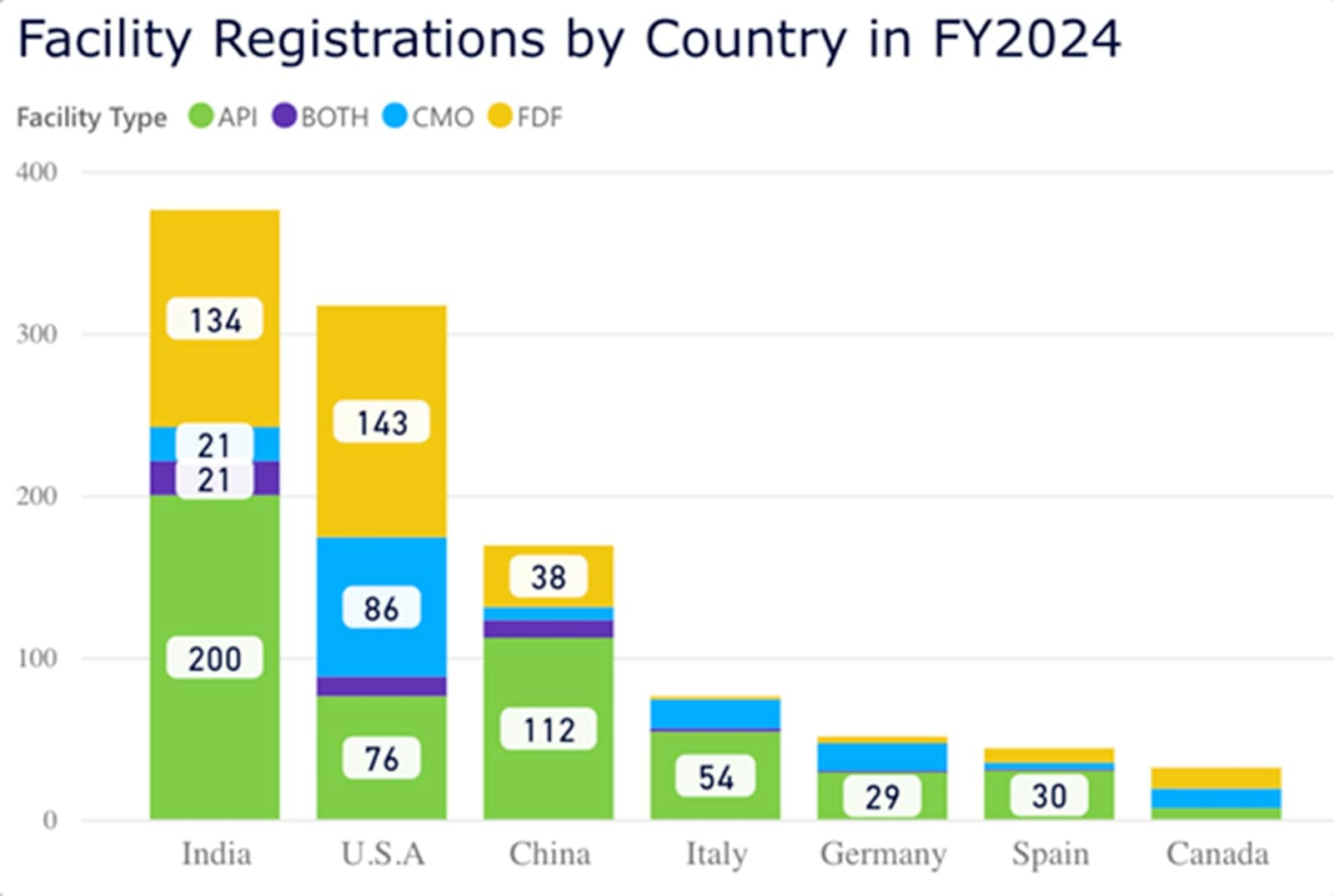

With lower generic drug manufacturing costs than even Chin, India has the highest number of US-FDA-approved sites outside the US. In FY2024, India led with 376 US-FDA facility registrations, the highest for any country.

Fig 1. Source: http://www.pharmacompass.com

Fig 1. Source: http://www.pharmacompass.com

Despite its pharmaceutical dominance, India’s prowess has largely been in generic drug manufacturing. The industry thrives on producing and exporting drugs after patents expire, avoiding the high-cost, high-risk investment in research and development (R&D) for new drugs.

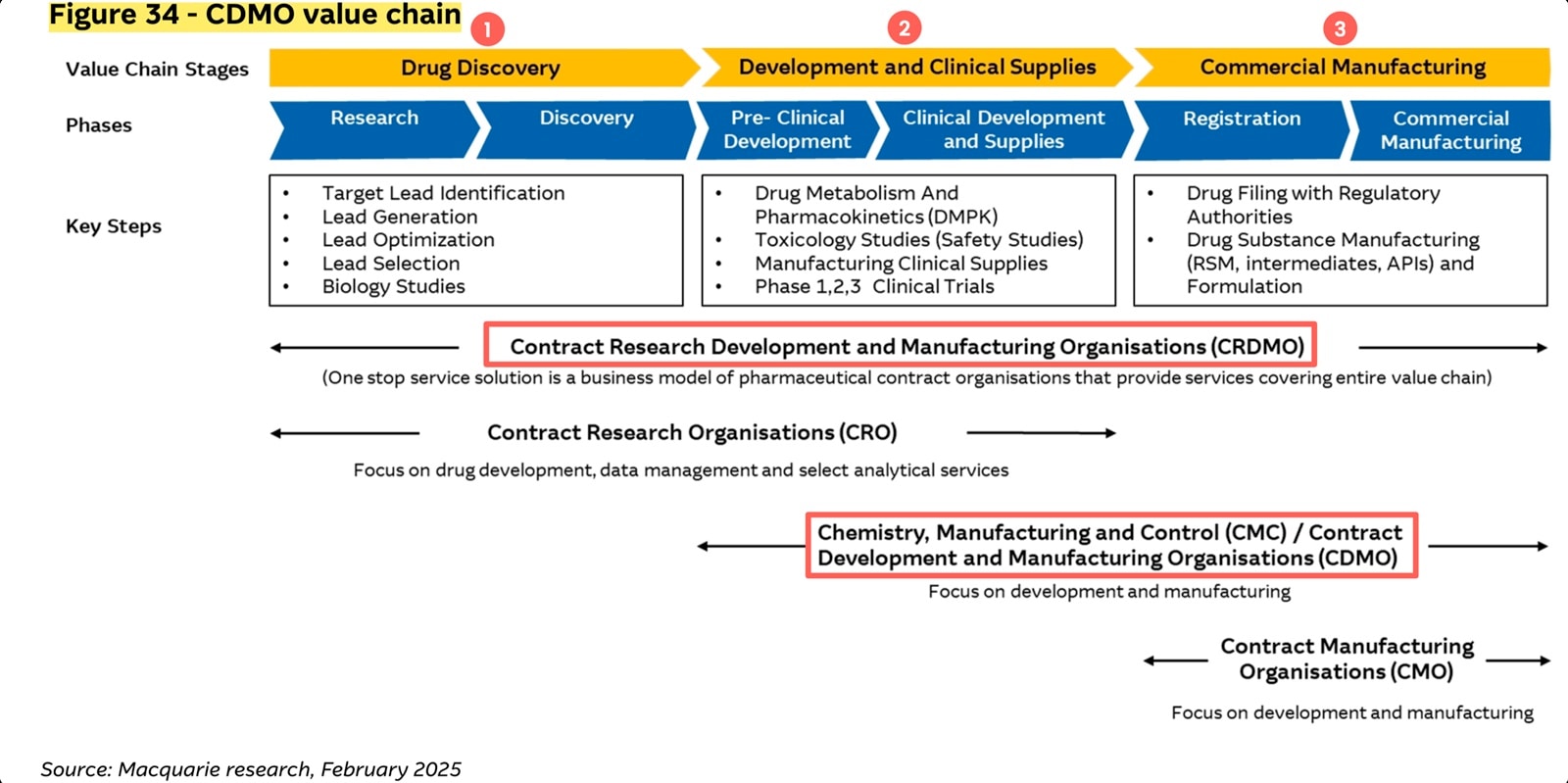

This is slowly changing. Indian firms are now expanding beyond generics into research, discovery, clinical testing, development, and manufacturing (CRDMO). Some focus on clinical development and manufacturing while bypassing full-scale R&D, saving billions.

Fig 2. Source: Macquarie Research, February 2025.

Fig 2. Source: Macquarie Research, February 2025.

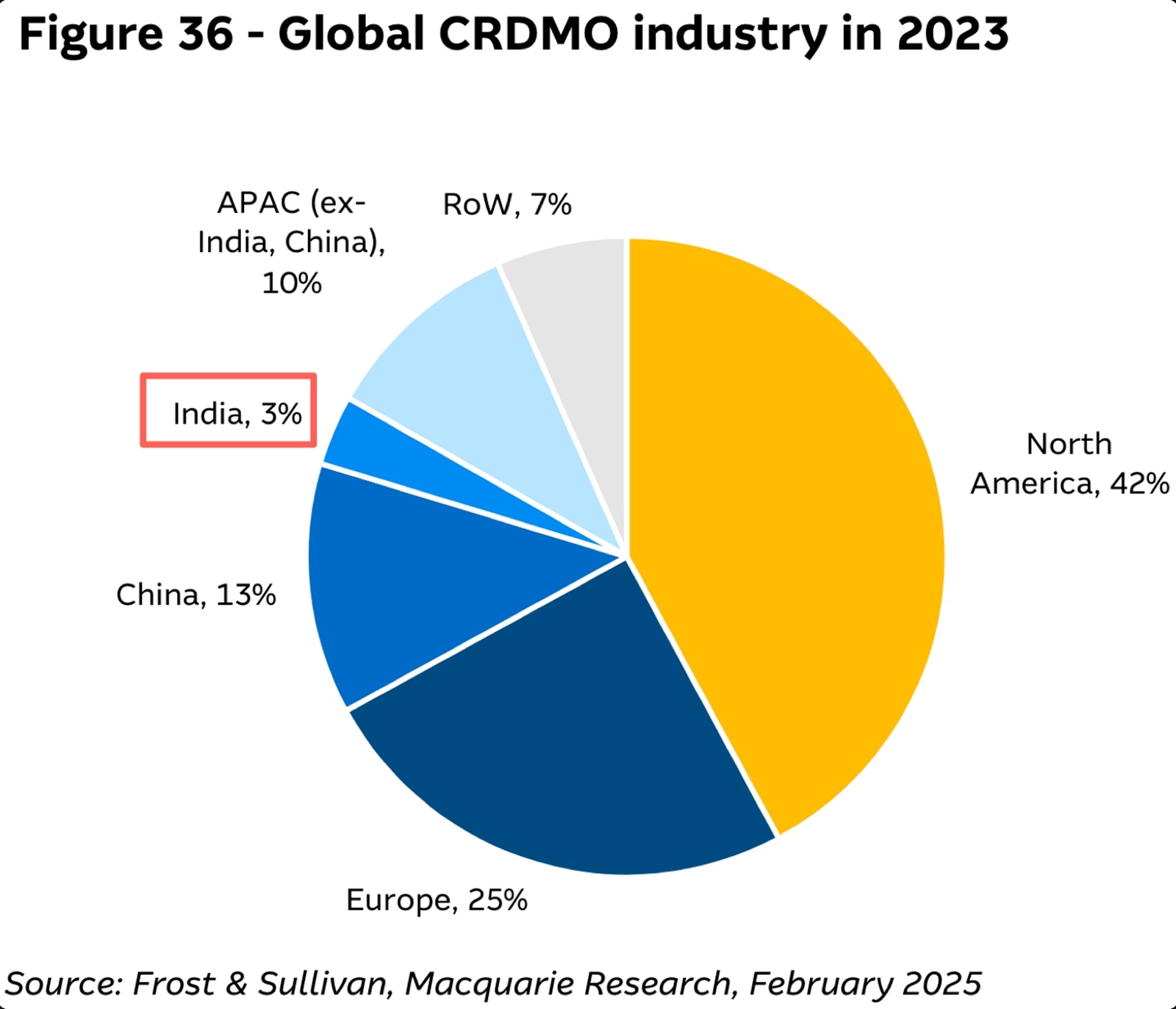

Currently, India accounts for just 3.6% of the global market share, but a significant opportunity lies ahead.

Global pharmaceutical firms are increasingly shifting from China to India due to several factors, including drug pricing pressures, geopolitical factors, and regulatory changes such as the US Bio-secure Act. The US Bio-secure Act is encouraging US firms to diversify away from China.

India is becoming a preferred destination for small molecule development due to its cost advantages, regulatory compliance, and expertise in Active Pharmaceutical Ingredients (APIs). The Inflation Reduction Act (IRA) is also driving demand for Contract Development and Manufacturing Organisation (CDMO) services in India.

Listed in November 2023, Blue Jet Healthcare saw its stock remain stagnant for six months before surging from June 2024. While the NIFTY Small Cap Index has declined 21.4% since September 2024, Blue Jet is up 38.5%.

Figure 3: http://www.tradingview.com

Figure 3: http://www.tradingview.com

Is this just market hype, or is Blue Jet truly positioned to ride the CRDMO wave? Let’s dive deeper.

Blue Jet Healthcare operates in three business segments:

📌 Contrast Media Intermediates

📌 High-Intensity Sweeteners

📌 Pharma Intermediates & API (Active Pharmaceutical Ingredients)

With the following Revenue breakup in 9MFY25 :

Fig 4: Source: Macquarie Research, Indian CRDMO Report, February 2025

Fig 4: Source: Macquarie Research, Indian CRDMO Report, February 2025

However, a closer look at growth trends across these segments reveals where the real opportunities lie.

Blue Jet Healthcare produces contrast media intermediates (raw material), not contrast media itself. Contrast media are agents used to enhance imaging in X-ray/CT scans, MRI, and ultrasound.

Contrast media are categorised based on the imaging methodology for which they are used

• X-ray/Computed Tomography (CT): Predominantly iodine-based

• Magnetic Resonance Imaging (MRI): Predominantly gadolinium-based

• Ultrasound (USG): Stabilised microbubble-based

This industry has high entry barriers, with four players controlling 75% of the market. These players generally tend to stay with key suppliers over long periods. Blue Jet has strong, long-term relationships with top customers, spanning 4 to 25 years. Further, 70% of the total sales in this segment are backed by volumes.

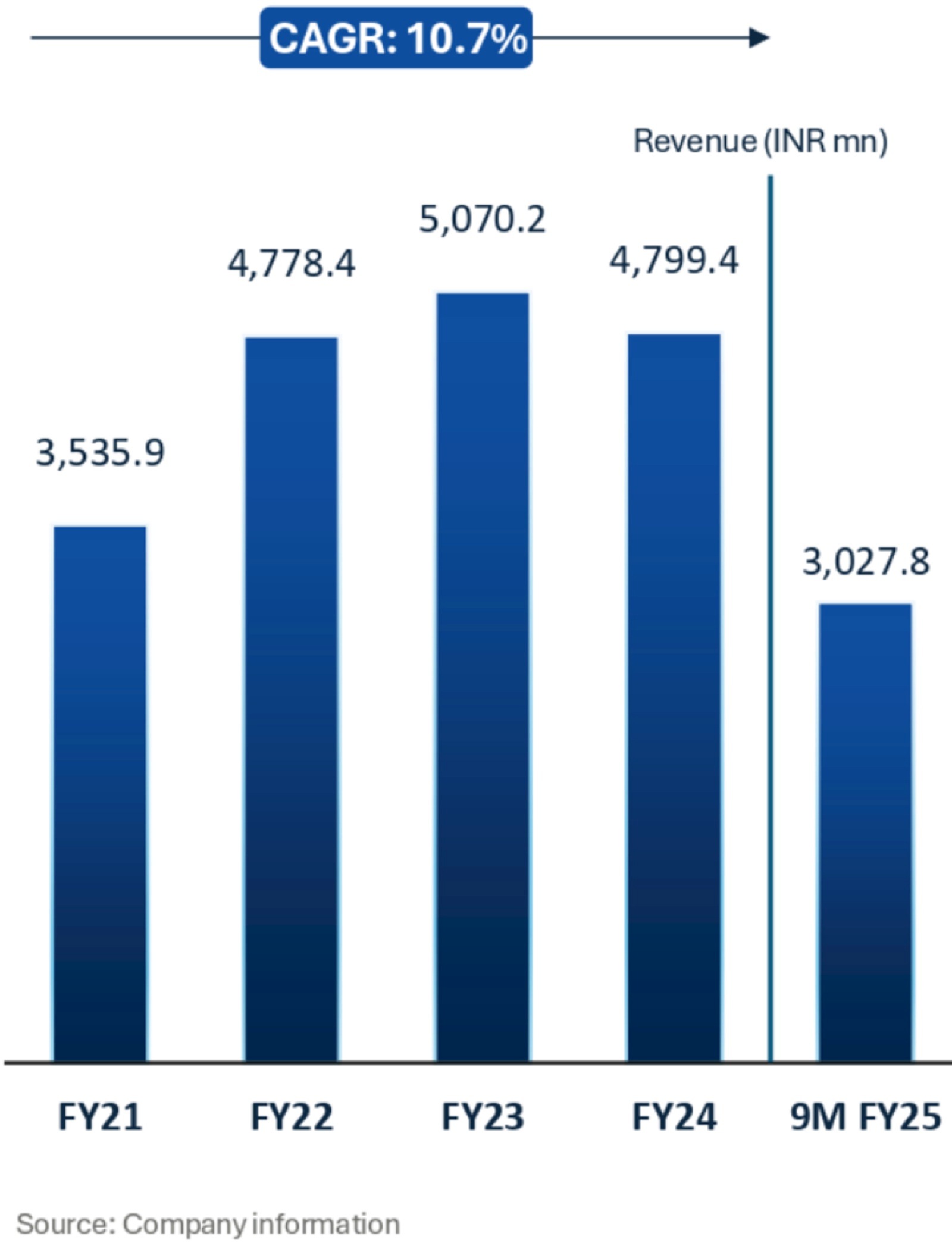

Despite being Blue Jet’s largest segment, growth has been modest, FY21–24 revenue CAGR was 10.7% and 9MFY25 revenue was down 17.8%.

Fig 5: Source: Blue Jet Healthcare, Q3FY25 Investor Presentation

Fig 5: Source: Blue Jet Healthcare, Q3FY25 Investor Presentation

However, current numbers do not capture key developments in the segment.

Value Addition: Blue Jet has progressed in the contrast-media intermediate business, moving from supplying basic building blocks to key intermediates, increasing realisations by approximately three-fold. The company is moving towards the iodination of key intermediates, which could potentially increase realisations by fourfold. Blue Jet has also commissioned a 37KL capacity for gadolinium-based contrast media which recently finished plant validation batched and is likely to contribute to the segment further.

According to the Macquarie Report on the CRDMO sector, this segment could grow at 16% CAGR by FY30.

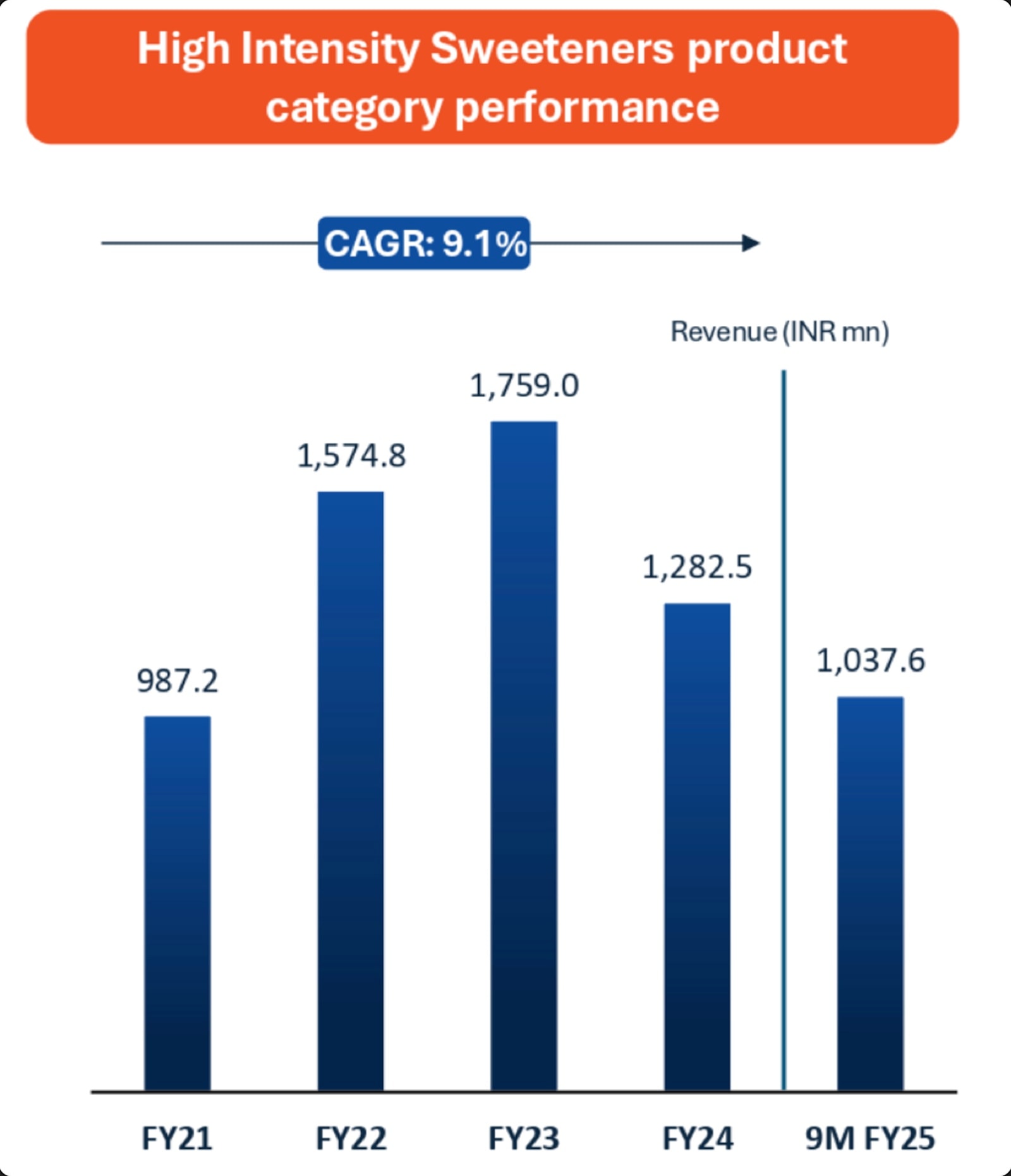

High-Intensity Sweeteners: Blue Jet Healthcare has had a legacy segment for over three decades in high-intensity sweeteners (HIS), contributing nearly 20% of its top line. The company has seen a top-line compound annual growth rate (CAGR) of about 10% since FY21.

The high-intensity sweetener addressable market is about $3 billion, with saccharin, Blue Jet’s major product, constituting about 13-14% of this market share.

Capacity and Global Presence: Blue Jet has about 10% of the world’s capacity for saccharin, with a production capacity of about 3,500 to 4,000 metric tons, making it one of the leading players worldwide in this molecule.

However, this segment is unlikely to be a major revenue driver going forward.

Fig 6: Source: Blue Jet Healthcare, Q3FY25 Investor Presentation

Fig 6: Source: Blue Jet Healthcare, Q3FY25 Investor Presentation

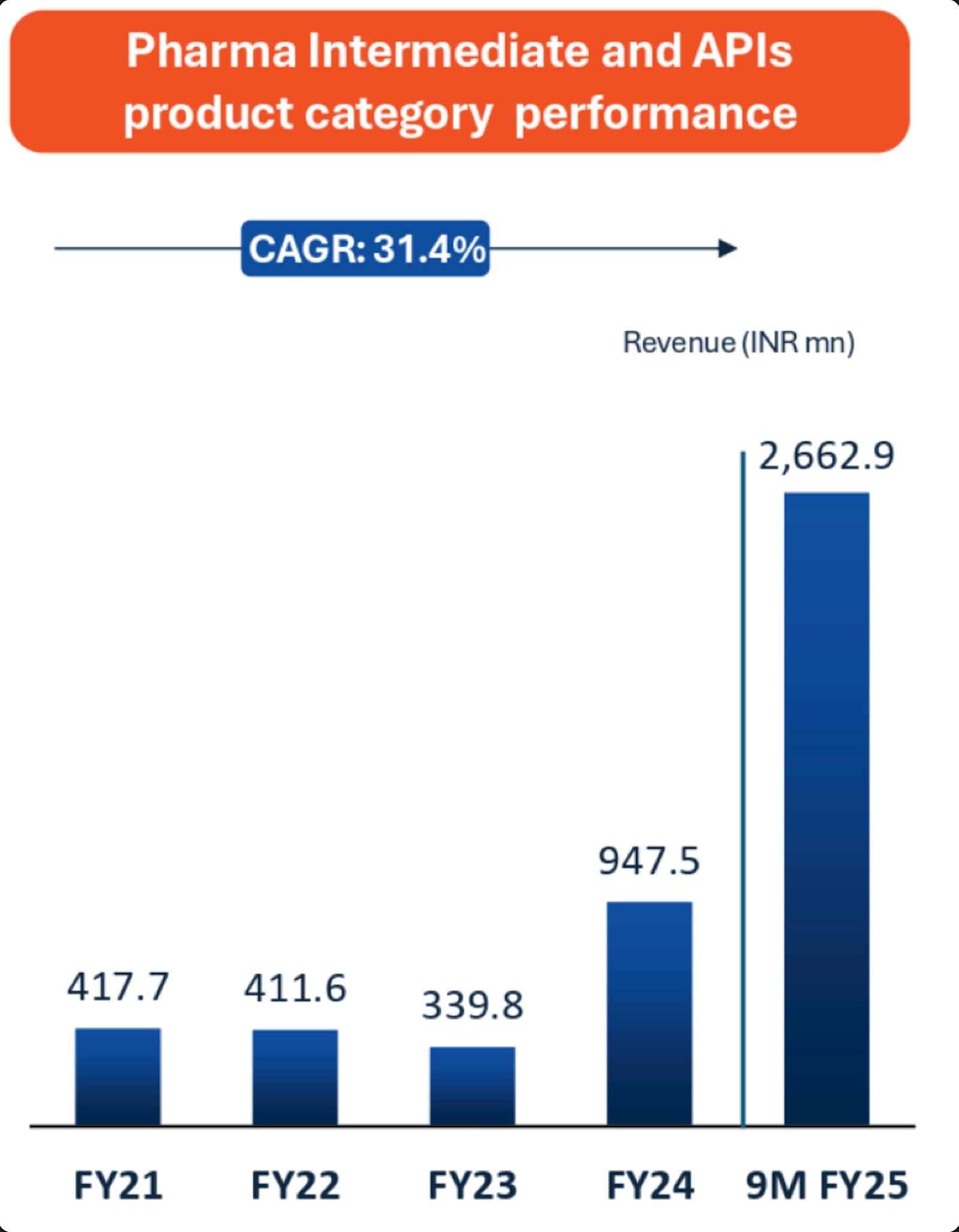

This segment has captured market attention due to rapid expansion. Blue Jet’s CDMO and CRAMS (Contract Research and Manufacturing Services) capabilities allow it to partner with multinational firms and innovator companies from bench to bulk stage, focusing on chronic therapeutic segments.

As of H1FY24, the company has 20 products, eight of which are under the CDMO model. This segment has been built over time, with opportunities incubated three to four years ago reaching industrial scale now.

Key Intermediate for Bempedoic Acid: A primary driver of top-line growth is the increasing supply of TosMIC, a key intermediate for Bempedoic acid (a lipid-lowering drug), to an innovator company, Esperion. Bempedoic acid is a cholesterol-lowering drug.

Esperion’s recent label expansion in the US and EU markets has increased the total addressable patient pool from 10 million to 70 million. According to Macquarie Capital report, US prescriptions are growing at a double-digit rate quarter-over-quarter. Macquarie expects revenues to go up 15X by FY30.

This segment, around 13% of FY24 revenue, accounted for more than 30% in 9MFY25. The revenue went from 33 crore in FY23 to 266 crore in 9MFY25.

Fig 7: Source: Blue Jet Healthcare, Q3FY25 Investor Presentation

Fig 7: Source: Blue Jet Healthcare, Q3FY25 Investor Presentation

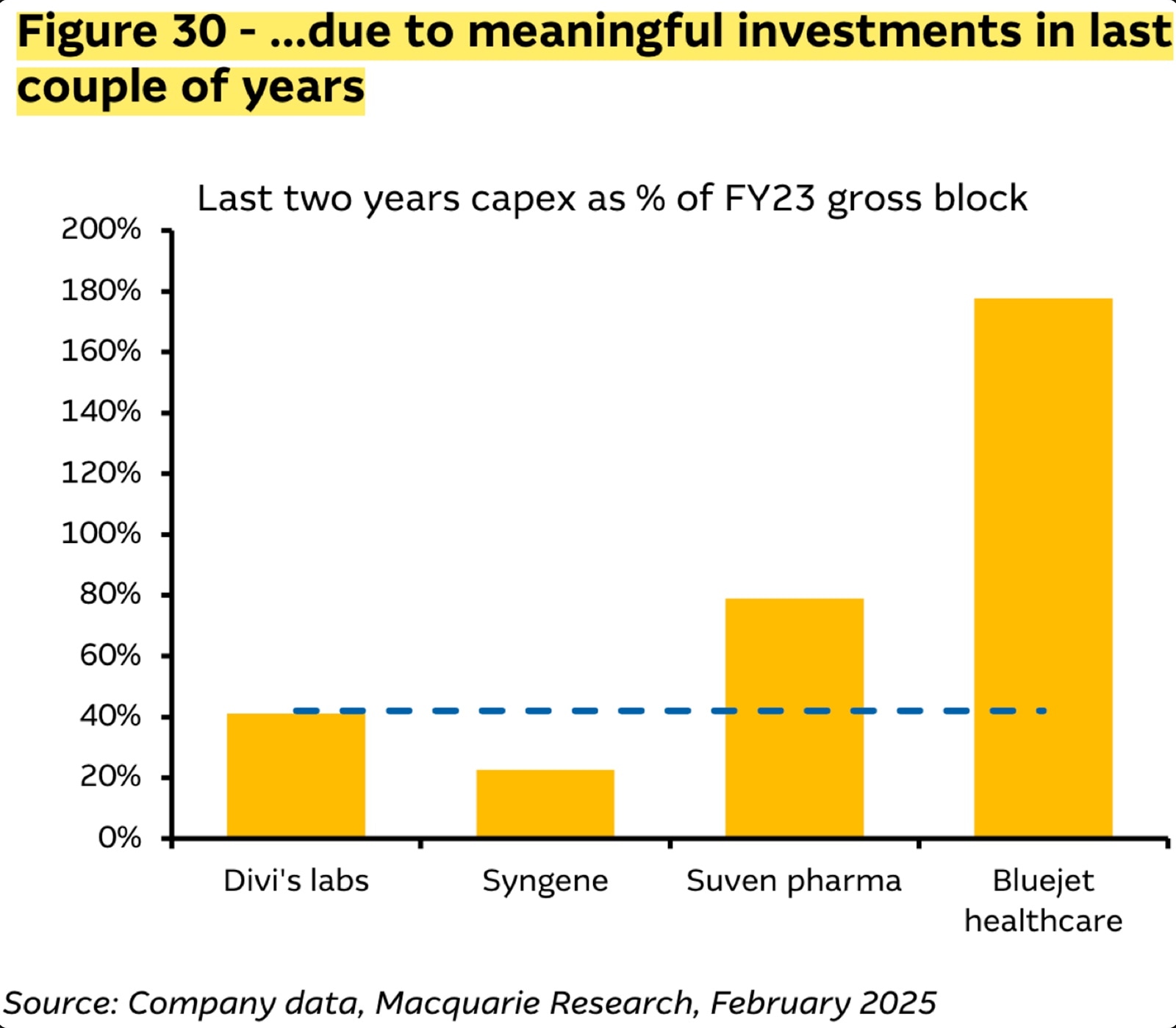

Moreover, Blue Jet has increased its capacity by 2.5X since FY23, signaling confidence in sustained growth.

Fig 8: Source: Blue Jet Healthcare, Macquarie Research

Fig 8: Source: Blue Jet Healthcare, Macquarie Research

Blue Jet is unlikely to be a value stock, it is now available at ‘growth stock’ valuations. With a trailing PE of 55X and EV/EBITDA of 38.7X, it’s hard to say the company is cheap. If its growth trajectory holds, Blue Jet could be a compelling long-term investment. Investors will need to assess whether the industry tailwinds and company fundamentals justify its premium valuation.

Note: We have relied on data from http://www.Screener.in and http://www.tijorifinance.com throughout this article. Only in cases where the data was not available, have we used an alternate, but widely used and accepted source of information.

Rahul Rao has helped conduct financial literacy programs for over 1,50,000 investors. He also worked at an AIF, focusing on small and mid-cap opportunities.

Disclosure: The writer and his dependents DO NOT HOLD the stocks discussed in this article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.