Stay updated with the latest - Click here to follow us on Instagram

Journalism of Courage

Some feel that the government can look to increase the pension every month and make the amount more meaningful as the annual contribution into EPS far exceeds the benefits disbursed.

Some feel that the government can look to increase the pension every month and make the amount more meaningful as the annual contribution into EPS far exceeds the benefits disbursed.

Defending his decision to impose tax on 60 per cent of the Employees’ Provident Fund corpus in case it was withdrawn at the time of retirement rather than using it to buy an annuity product, finance minister Arun Jaitley had said the purpose of the move was to encourage more private sector employees to go for pension security after retirement instead of withdrawing the entire money from the PF account.

While the proposal met with all-round criticism and forced the finance minister to roll it back, experts point that the employer’s EPF contribution has a pension component in it (Employees’ Pension Scheme) and provides some amount of pension to all EPF members. While many feel that the pension amount under the EPS is not enough to meet post-retirement needs of individuals and finance minister’s intentions may have been good, they say that the government should look to provide more investment options instead of limiting the options to the annuity schemes of insurance companies.

Some feel that the government can look to increase the pension every month and make the amount more meaningful as the annual contribution into EPS far exceeds the benefits disbursed. In fact for FY14, while the EPS contribution amounted to an aggregate of Rs 16,417 crore, the benefits disbursed amounted to Rs 10,900 crore and thus the government is currently comfortably placed.

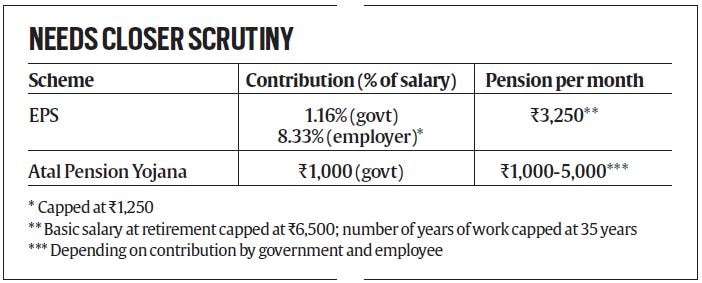

Is EPS sufficient?

Contrary to the general perception, it is not just the government employees who get pension under the EPF scheme. Even private sector employees who are part of the EPFO are eligible for pension under EPS.

While 12 per cent of the contribution from the employee goes to EPF, the equivalent contribution from the employer is split into two parts — 8.33 per cent going towards EPS (subject to a maximum of Rs 1,250) and the remaining 3.67 per cent towards EPF. Even the Central government contributes 1.16 per cent of wages of the employees towards Employees’ Pension Scheme.

If employer contribution towards EPS is limited at Rs 1,250 (8.33 per cent of the statutory wage limit of Rs 15,000), the more important factor is the quantum of pension that one will get after completion of service (maximum of 35 years). A quick check reveals that it is not much.

The monthly pension is calculated on the basic salary at the time of retirement (capped at Rs 6,500) along with the number of years of work (capped at 35 years). Calculations show that the monthly pension for an individual who has worked 35 years and has a basic salary of Rs 6,500 would amount to just Rs 3,250 per month for the lifetime and that is the maximum that one can earn as pension within the scheme.

It is crucial to note that unlike the EPF component, which earns an interest rate decided by the government (current rate stands at 8.8 per cent), the EPS component does not earn any interest. It, however, offers benefits such as pension on disablement, pension to widows and children and even gives the option to start pension at the age of 50.

Individuals who have contributed for less than 9 years and six months also get the option to withdraw their contribution in full. Clearly, Rs 3,250 is an insufficient amount to meet one’s post-retirement needs.

Some also feel that if the government increases the EPS component in the employer’s EPF part from the current limit of Rs 1,250 and also provides some interest on the contribution, it will provide a significant boost to the government’s idea of creating a pensioned society as both the corpus and the pension component will rise significantly.

What it means for you

If you contribute Rs 1,250 every month for 30 years, then the total corpus at the end of your work life would be Rs 4.5 lakh since the government does not provide any interest on it. However, if the government provides an interest rate of 8 per cent on the contribution, the corpus would jump to Rs 18.6 lakh. Instead, if the contribution is raised to Rs 2,000 per month and the government pays an interest of 8 per cent on the contribution, then over a period of 30 years the corpus would jump to around Rs 30 lakh.

The other option

In its effort to provide social security and monthly pension to all individuals in the country, the government announced the Atal Pension Yojana for all bank account holders in the country wherein the government guarantees a fixed pension of anywhere between Rs 1,000 and Rs 5,000 per month at the age of 60 depending upon the contribution.

Within the scheme, the government will contribute 50 per cent or Rs 1,000 per annum (whichever is lower) for a period of 5 years between FY16 and FY20 after which individuals may continue with the scheme.

However, even under this scheme, the maximum pension amount is limited to Rs 5,000 per month and financial experts feel that it may not be enough to cover your basic expenses after 20-30 years when one retires.

Assuming that you are 30 years old and have a monthly basic expense of just Rs 2,000, even then this pension amount of Rs 5,000 won’t cover your post-retirement needs. At an average inflation of 5 per cent over the next 30 years, you would

need at least Rs 8,643 per month to cover your expense.

As these two schemes do not offer sufficient pension to cover monthly expenses post retirement, it does call for review or better options to be made available. Although the finance minister proposed that EPF contributors can use 60 per cent of their EPF corpus to buy annuity and can save on tax, even as the proposal stands withdrawn, experts point that investors should be given more options. “Indians like to have access to their capital whereas investing in an annuity product locks the capital. The government could have thought of more options for investors where they can park 60 per cent of the EPF corpus. It would have allowed them to invest a part of the corpus with annuity product and the other part somewhere else where there is access to capital,” said a certified financial planner, who did not wish to be named.

Stay updated with the latest - Click here to follow us on Instagram