© The Indian Express Pvt Ltd

Tags:

IN her last full Budget ahead of Lok Sabha elections next year, Union Finance Minister Nirmala Sitharaman kept her focus on two key aspects: one, growth – by setting aside a large outlay for an unprecedented surge in capital spending, and two, fiscal consolidation, by slashing subsidies and spending on the job guarantee scheme.

The big Budget idea came in the form of raising the threshold at which income tax kicks in to Rs 7 lakh a year from Rs 5 lakh a year, plus a solid nudge prodding individuals to shift to a new tax regime by restructuring the tax slabs. This does key things: pushing people to a clutter-free zero exemption tax regime, to freeing up money in the hands of those earning just under Rs 60,000 a month for spending and also directing money from tax-focused saving instruments to discretionary spending or investment in the markets.

Clearly, Sitharaman knew the new personal tax regime introduced three years back found little or no traction so far, and hence felt the need to incentivise individuals for them to step out from the exemption era. This is similar to a simplification she attempted on the corporate tax side where the rate was lowered to 22 per cent from 30 per cent for companies not claiming any exemptions.

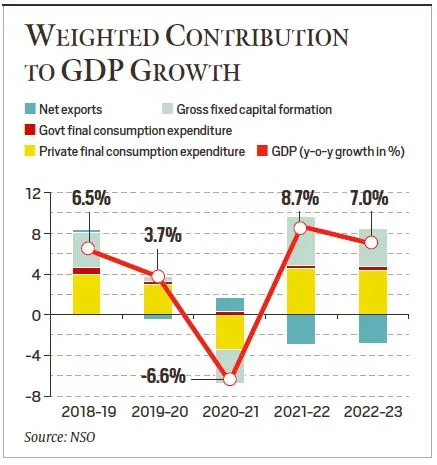

The Budget has projected a nominal growth rate of 10.5 per cent for 2023-24; only if the average retail inflation for the year is assumed to be 4 per cent, does the real growth rate turn out to 6.5 per cent (nominal growth rate minus inflation) as projected in the Economic Survey. But the RBI has projected inflation in the first half of this year itself to be 5.2 per cent; even if the average inflation in the second half is 4 per cent, the full year average turns out to be 4.5 per cent. This only suggests that the government may be over-estimating the growth prospects for the next year.

Over the last three years, and particularly after the pandemic, the government has consistently hiked the allocation for capital spending. Capital spending has a much higher multiplier effect – 2.5x – and hence adds more to economic output than revenue expenditure comprising salaries, pensions, interest payments, etc. In just three years, the capital expenditure outlay has more than doubled to Rs 10 lakh crore (over 3 per cent of the GDP) from Rs 4.39 lakh crore in 2020-21. This is an acknowledgment that the strategy of higher government spending to draw in private sector investment is yet to show results; in other words, the government needs to continue to spend a lot more in infrastructure to crowd in the private sector. Complementing the Centre’s capex push, Sitharaman has allowed states to raise up to Rs 1.3 lakh crore through 50-year interest free loans. The effective capital expenditure (which includes grants to states) is budgeted at Rs 13.7 lakh crore for the next year, almost 13 per cent higher than in 2022-23.

This capex push, Sitharaman hopes, will bring growth, and also jobs. The huge allocation to railways (Rs 2.4 lakh crore next year compared with Rs 1.59 lakh crore in 2022-23), roads and highways (Rs 2.7 lakh crore in 2023-24 compared with Rs 2 lakh crore this year) and housing (PM Awas outlay hiked 66 per cent to Rs 79,000 crore), will not only spur demand for heavy equipment, cement, steel and other commodities, but also generate more employment. This is probably a reason why the government has reduced the NREGA outlay by a third to Rs 60,000 crore, a signal to part of the workforce which migrated to the hinterlands to return to employment-intensive sectors including housing and construction and contact-service industries like hotels and restaurants.

[https://www.youtube.com/watch?v=RBDqX-RvddE]

The government has managed to stick to its fiscal prudence mantra and did not breach its deficit target of 6.4 per cent of GDP for the current financial year. What has helped the government meet its target in the current financial year, however, is the high nominal GDP (the denominator while calculating fiscal deficit as a percentage of GDP). The nominal GDP is high because inflation remained way higher at 6.7 per cent this year compared with the RBI’s 4 per cent target.

For the next two years as well, it has provided a glide path which would inspire confidence. It has estimated the fiscal deficit for 2023-24 at 5.9 per cent of the GDP and also hopes to consolidate over the next two years such that the fiscal deficit in 2025-26 is 4.5 per cent of GDP or less.

The Budget did not succumb to populist demands or expectations of big giveaways ahead of the Lok Sabha elections next year. But it also chose to keep in abeyance difficult reforms – those that require consensus-building among stakeholders and are in subjects that need states on board. Reforms in these areas – land, labour, farm – where the NDA government has met with limited success require transparency, political heavy-lifting and a different language to communicate.