© The Indian Express Pvt Ltd

Tags:

Strong domestic demand and a pickup in capital investment will support the country’s growth trajectory in FY24, according to the Economic Survey. In possible pointers to the Union Budget 2023-24 pushing capital expenditure, the Survey said the government’s thrust on capex, particularly in the infrastructure-intensive sectors like roads and highways, railways, and housing and urban affairs, has longer-term implications for growth. Capex-led growth, it said, will bring back animal spirits and help manage debt levels.

Central to the government’s growth optimism in FY24 is the expectation of a recovery in private capex, driven by improved balance sheets, resurging credit, and the crowding in from public capex. This, and an anticipated funding boost stemming from capital flows once the recessionary trends in major advanced economies trigger a halt in monetary policy tightening, are likely to be growth drivers in the coming years.

“Growth is expected to be brisk in FY24 as a vigorous credit disbursal, and capital investment cycle is expected to unfold in India with the strengthening of the balance sheets of the corporate and banking sectors,” the Survey said. “While on the one hand, capital expenditure strengthens aggregate demand and crowds-in private spending in times of risk aversion; it also enhances the longer-term supply-side productive capacity,” it added. The financial system stress experienced in the second decade of the millennium, evidenced by rising non-performing assets, low credit growth and declining growth rates of capital formation caused by excessive lending witnessed in the first decade-plus, is now behind us, the finance ministry’s report card on the government’s performance during the current fiscal said.

The other factors, the Survey said, that will push India’s growth are limited health and economic fallout for the rest of the world from the current surge in Covid-19 infections in China; inflationary impulses from the reopening of China’s economy turning out to be neither significant nor persistent and recessionary tendencies in major advanced economies triggering a cessation of monetary tightening and a return of capital flows to India amidst a stable domestic inflation rate below 6 per cent.

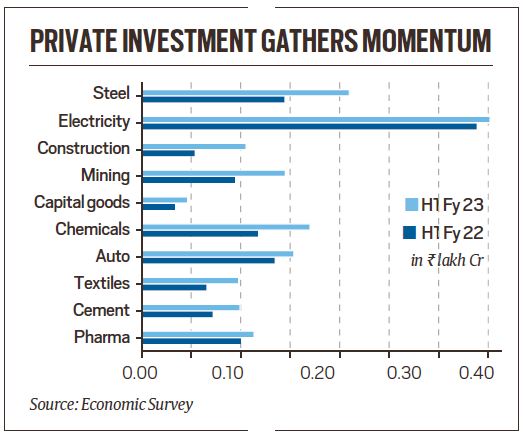

It further said aided by healthy financials, incipient signs of a new private sector capital formation cycle are visible. More importantly, compensating for the private sector’s caution in capital expenditure, the government raised capital expenditure substantially.

Although domestic consumption rebounded in many economies, the rebound in India was impressive for its scale, which has contributed to a rise in domestic capacity utilisation, it said. “The rebound in consumption has also been supported by the release of pent-up demand, a phenomenon not again unique to India but nonetheless exhibiting a local phenomenon influenced by a rise in the share of consumption in disposable income,” it said.

Since the share of consumption in disposable income is high in India, a pandemic-induced suppression of consumption built up that much greater recoil force. Hence, the consumption rebound may have lasting power, the Economic Survey said. It said while an increase in export demand, rebound in consumption, and public capex have contributed to a recovery in the investment/manufacturing activities of the corporates, their stronger balance sheets have also played a big part equal measure to realising their spending plans.

According to the survey, the resilience of the domestic financial system is reflected in the healthy balance sheet of banks, stronger capital levels of non-banking finance companies (NBFCs) and robust growth in the asset under management (AM) of domestic mutual funds.

Buoyant demand for bank credit and early signs of a revival in the investment cycle are benefiting from improving asset quality, a return to profitability and resilient capital and liquidity buffers, the survey said.