Looking at 2025, The Economy: Some positives, some concerns

Finance Minister Nirmala Sitharaman says the slowing of Q2 growth is a “temporary blip”. But RBI has downgraded its GDP growth forecast for 2024-25 to 6.6% from 7.2% earlier.

The last mile of disinflation is turning out to be prolonged, with increasing dissonance in the growth and inflation trajectories.

A pronounced dip in economic output in the first three quarters of 2024 notwithstanding, India’s long-term growth story is believed to be intact. A growth rate of 6.5% is projected over the next half decade, which would help the country remain the fastest-growing big economy in the world.

However, China, Japan, and South Korea grew at well over 8% on a sustained basis during their rapid-growth phases. Whether 6%-plus growth would be enough for a country that needs to generate upwards of 8 million jobs every year until 2030 is the big question — and whether this growth rate would be enough to bridge expanding wealth disparities and offer scope for generational mobility.

You’ve Read Your Free Stories For Now

Sign up and keep reading more stories that matter to you.

There is a view that the decline in growth rate simply brings it back to trend after data aberrations triggered by the pandemic and the subsequent buoyancy on an abnormally low statistical base. Finance Minister Nirmala Sitharaman has said the lower-than-expected GDP growth of 5.4% in the second quarter of FY25 was only a “temporary blip”.

Economist Neelkanth Mishra and his team at Axis Bank have described the loss in momentum for the Indian economy in the first half of the current fiscal as “cyclical”, due to “unintended fiscal and monetary tightening”. In October, Japanese brokerage Nomura had said the Indian economy was in a phase of “cyclical growth slowdown”, and described the Reserve Bank of India’s estimate of 7.2% GDP expansion as “overly optimistic”. Weeks later, RBI was forced to pare its forecast by more than half a percentage point.

The Positives

There are some clear upsides to the current picture of the economy.

Government spending

Fiscal spending is already seen as rising after the dust of the elections has settled. The recent cut in the cash reserve ratio (CRR) has freed up money kept by banks with the RBI.

The capex cycle seems to have restarted in some sectors, boosting capital formation, says Mishra, adding that this growth will be investment-led. Also, monetary easing is expected to support growth in the coming financial year. But the government will likely have to continue to do the heavy lifting.

Story continues below this ad

Economists also say the GDP shock of Q2 FY25 — another set of dismal numbers are likely in Q3 — merely signals a progressive normalisation of the growth trajectory after the waning of the base effect of the pandemic, when the economy shrank abnormally. That could partly explain the steady slide in growth from 8.6% to 7.8% to 6.7% to 5.4% in 2024.

State of economy, key indicators. State of economy.

“…It is not that we think that the second quarter slowdown is purely a data artefact and as more data comes in, it will automatically be upgraded. The numbers will be revised higher or it could be a simple, seasonal factor… Or it could be something more fundamental as the ability of the state to spend what is budgeted… We will be on track to achieve…between 6.5-7 per cent for the whole financial year. But…the focus is on how to make sure that we grow at a sustainable rate in a world that is going to be extraordinarily difficult,” Chief Economic Adviser V Anantha Nageswaran said at a CII event on December 12.

After a couple of quarters of likely sub-optimal economic output, GDP growth is projected to settle around 6.5%, which could mark the real rate of growth going back to trend. The question that RBI’s overestimation — and subsequent correction — poses is this: did the central bank keep interest rates high for longer than needed because it had projected an excessively rosy picture of GDP growth? However, inflation remains at the upper end of the permissible band, and food prices are at near double digits in terms of inflation — that somewhat strengthens the argument for sticking with high rates, and compounds RBI’s problems going forward.

Lower investment growth was largely due to public investments coming down; this could change in the second half of the fiscal and later. One indication is the surge in order backlog for capital goods companies that suggests investment activity is likely to grow going forward. For instance, in utilities, a pivot from renewables back to thermal power, which accounted for the bulk of the capex between 2010 and 2015, could give impetus to industrial activity, given that virtually no thermal capacity has been added over the past 6-7 years.

Story continues below this ad

According to Mishra, a relatively empty election calendar in the states in 2025, provides a window for reforms. But the appetite — even for restarting pending reforms such as the Labour Codes — appears diminished.

Possible MSME recovery

In two other dismal trends, analysts see a possible silver lining.

Corporate growth is slowing, partly due to sliding consumption growth, but there could be an upside. Former Chief Statistician Pronab Sen said Micro, Small and Medium Enterprises (MSMEs), which have been hit repeatedly by shocks such as demonetisation, implementation of GST, and the Covid-19 lockdown, are perhaps getting back in business, and competing with the corporate sector.

While more data are needed on this, two other signals suggest this possibility: one, there is consumption recovery in rural areas even as urban growth is flagging; two, Periodic Labour Force Survey numbers show an improvement in salaried employment, which could be partly due to increasing non-casual jobs with MSMEs. An MSME rebound could mean the two branches of the K-shaped recovery could narrow.

Story continues below this ad

The labour data show another positive: female participation in the labour force is increasing, particularly in rural areas. Around 39.6% of women with education level of post-graduate and above were reported as working in FY24, compared to 34.5% in FY18. For women with higher secondary education level, these numbers were 23.9% and 11.4%.

Growth in services

India’s services surplus as a share of GDP hit a new high in October 2024 — a key positive. On the structural drivers of India’s share gains in global services exports, Mishra and his team say the disaggregation of global services value-chains, rapid increase in global cross-border telecom bandwidth, and the surge in remote-working are adding to the demographic trends supporting the growth in India’s services exports to developed markets.

In November, India’s services trade exports surpassed goods exports as IT exports continued to register strong growth amid weak goods demand in the West, and higher shipping costs due to disruption in the Red Sea, according to official data released by the Commerce Ministry. Going forward, however, India’s IT exports, on a compositional basis, appear vulnerable to new technologies such as AI.

The Negatives

Sluggish investments

Performance is tapering off for many corporates, and investments are struggling. Executives at Tata Consumer Products Ltd have flagged concerns over “softness” in urban demand; those at Nestle India have said big cities are pressure points and blamed the “muted demand” partly on high food inflation. Carmakers are pointing to worries on demand, blaming it on heavy rain and the election-induced slowdown. All of this could have repercussions for growth and job creation.

Story continues below this ad

But why are private investments struggling, despite pre-Covid corporate tax cuts and exhortations by the government to invest?

To unleash the so-called animal spirits, companies must feel optimistic about the future, and not have to look behind their backs. The single biggest hurdle to fostering a conducive investment environment is India’s tax laws and its administration, Arvind P Datar, Senior Advocate, said at the National Convention of All India Federation of Tax Practitioners on December 16.

Companies are also scaling down salary outlays. Real salary and wage expenditure growth of listed non-financial corporates — a proxy for real urban wages — has moderated to 0.8% in Q2 FY25 from 1.2% in Q1 FY25, and is down from 2.5% in FY24 and 10.8% in FY23, Nomura said.

Savings-investment gap

The decline in the household financial savings rate could present another challenge. The RBI’s latest Financial Stability Report shows net financial savings of households fell to 5.3% of GDP in FY23 from 7.3% in FY22, sharply below the 8% average of the previous decade. Household net savings are the total money and investments of families, including deposits, stocks and bonus, minus any money they owe, such as loans and other debt.

Story continues below this ad

Over the same period, household debt has jumped sharply. Annual borrowings are at 5.8% of GDP, the second-highest level since the 1970s. A large part of savings is also entering financial markets bypassing the banking industry, which is another worry.

Sliding credit growth

Growth in credit has been falling — households, which mostly borrow to finance home purchases, have not been doing so since 2021. For a while, industry had offset this, but this has tapered off since the beginning of 2023. Excess capacity and lack of appetite for new projects is seen as limiting industry’s capacity to absorb new credit.

In such a scenario, bond-financed government spending is the only meaningful way to generate new credit in the economy, according to Mishra, but much of this new debt issued is being used to clean up old ‘hidden debt’ at the local level.

Unless there is a fundamental shift in the use of fiscal force to stimulate the economy, high growth is unlikely. Bank lending to MSMEs could be something to watch for, especially if personal credit slows and corporates are unwilling to borrow.

Story continues below this ad

While bad loans have been coming down, there are new concerns over a significant rise in NPAs in the personal loan and credit card segments. Both these types of credit are unsecured and carry high interest rates. In November 2023, the RBI had increased risk weight on the exposure of banks towards consumer credit, credit card receivables, and non-banking finance companies.

Fiscal prudence

At the Centre, fiscal consolidation has been a consistent theme. A projected decline in fiscal deficit from 6.4% to 5.9% of GDP in FY24 will stabilise public debt at around 83% of GDP — a promising indicator of sustainability, given India’s growth outlook, according to the IMF.

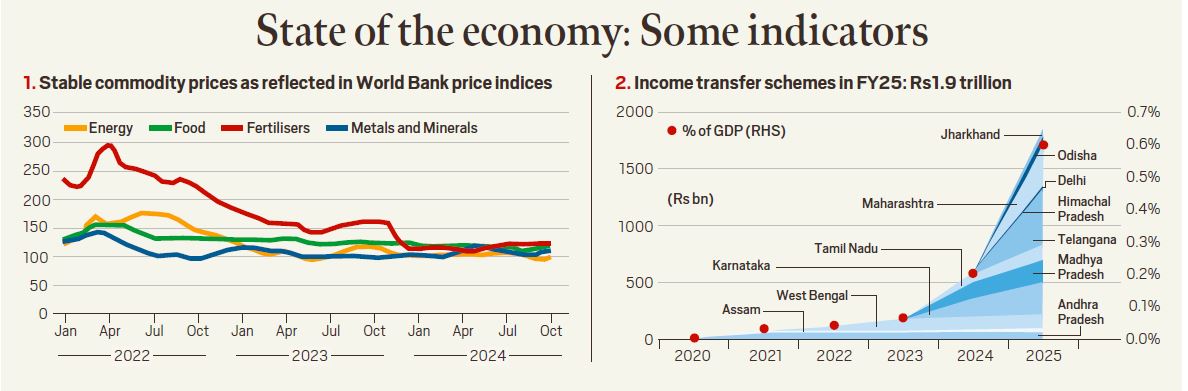

But competitive loosening of purse strings by states poses a fiscal problem. The RBI has flagged concerns over a sharp increase in expenditure by states on various subsidies, including farm loan waivers and cash transfers.

Axis Bank’s India Outlook report said that by 2025, 14 states would have some version of “handout” schemes aimed at about 134 million women, which is almost 20% of all women in India. These programmes cost the government almost Rs 1.9 lakh crore every year, or about 0.6% of the country’s GDP.

Story continues below this ad

While these transfers have helped lower-income families by giving them more money to spend, especially on food such as pulses, onions, and tomatoes, the supply of these items has not increased enough, which has caused food prices to rise, the report said.

Anil Sasi is the National Business Editor at The Indian Express, where he steers the newspaper’s coverage of the Indian economy, corporate affairs, and financial policy. As a senior editor, he plays a pivotal role in shaping the narrative around India's business landscape.

Professional Experience Sasi brings extensive experience from some of India’s most respected financial dailies. Prior to his leadership role at The Indian Express, he worked with:

The Hindu Business Line

Business Standard

His career trajectory across these premier publications demonstrates a consistent track record of rigorous financial reporting and editorial oversight.

Expertise & Focus With a deep understanding of market dynamics and policy interventions, Sasi writes authoritatively on:

Macroeconomics: Analysis of fiscal policy, budgets, and economic trends.

Corporate Affairs: In-depth coverage of India's major industries and corporate governance.

Business Policy: The intersection of government regulation and private enterprise.

Education Anil Sasi is an alumnus of the prestigious Delhi University, providing a strong academic foundation to his journalistic work.

Find all stories by Anil Sasi here ... Read More