© IE Online Media Services Pvt Ltd

Tags:

The recent debut of DeepSeek jolted global tech markets, causing a sharp decline in US tech stocks, from Nvidia to AMD, and wiping out billions of dollars in market value.

In India, Dixon Technologies, a key electronic manufacturing services company, too felt the tremors, with its share price falling 5.3% on January 28, extending its January descent to 20.8%. It underperformed the Nifty 50 Index, which fell 5% during the same period.

The paradox situation

While Dixon Technologies stock fell over 5% because of the DeepSeek shockwave, the stock has shown a seasonal downtrend in January over the last three years, falling 10.5% in January 2024, 31% in January 2023, and 38% in 2022. The 2022 downturn lasted from January to May as the global tech bubble burst.

January descent comes as Dixon Technologies’ December quarter is seasonally weak. The company reports a sequential decline in revenue following a peak in the September quarter. In Q3FY25, its revenue fell 9.4% sequentially to Rs 10,453.68 crore, and net profit fell 47.5% sequentially to Rs 216.23 crore.

Adding to this paradox is foreign institutional investors’ (FII) activity. While FIIs are selling several of their Indian stocks, they increased their holdings in Dixon Technologies to 23.22% in the December 2024 quarter from 22.69% in the September 2024 quarter .

The mobile PLI scheme

While the seasonal dip and overall market bearishness is a common reason for the correction in Dixon’s share price, another possible reason is the end of mobile Production Linked Incentive (PLI) scheme in March 2026.

Let us understand the importance of the PLI scheme for Dixon.

Dixon is the poster child of India’s most successful PLI scheme. PLI scheme incentives are provided when companies meet production targets, and Dixon was the only domestic company to continue meeting targets and get incentives for mobile phones, lightning, telecom and networking products, and inverter controller boards for air conditioners.

It is also a beneficiary of the PLI scheme for IT hardware (laptops and servers). It has already begun mass production for Lenovo and Acer and plans mass production for HP and Asus in Q1FY26.

Among all PLI schemes, the one for mobile has been the most successful to date.

The mobile segment is a volume-driven business. The China+1 strategy and the launch of the PLI scheme in 2020 paved the way for India’s electronic manufacturing services (EMS) players to flourish. Dixon took the high-volume, low-margin product route to make the most of the PLI scheme. Strong execution and operating efficiency helped Dixon become a leader in mobile phone contract manufacturing in India, driving its share price at a compounded annual growth rate (CAGR) of 78% in the last five years.

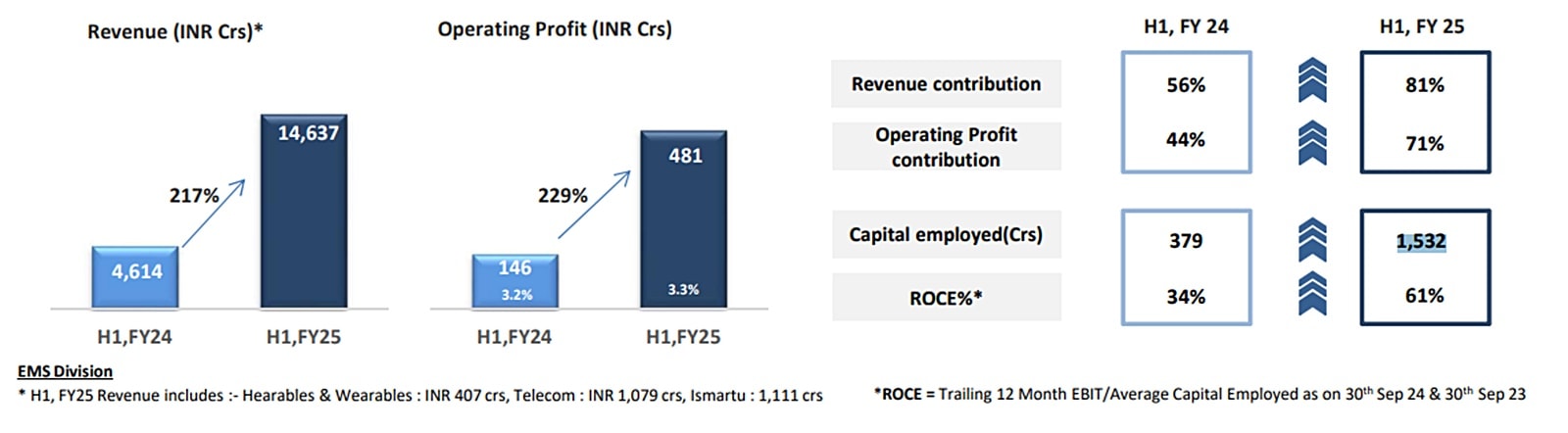

The Mobile and EMS segment contributed 81% to the revenue and 71% to the operating profit in H1FY25. Operational excellence, strong capital allocation discipline, higher asset turnover, and effective working capital management helped Dixon expand its return on capital employed (ROCE) to 61% in H1FY25 from 34% a year ago.

Dixon acquired a 56% stake in Ismartu India, which has a 10-12% smartphone market share and almost a 30-35% feature phone market share in India. It is expected to add Rs 7,000-8,000 crore in Dixon’s annual revenue, said Dixon Technologies CFO Saurabh Gupta in an interview with a business daily. Moreover, Dixon has entered into a smartphone manufacturing joint venture with Vivo, which has approximately 16% market share.

With the addition of Vivo, Dixon is now catering to almost 80-85% of the overall mobile market, serving 8 out of the top 10 mobile companies, said Arafat Saiyed, Vice President, InCred Research in an interview.

What analysts say

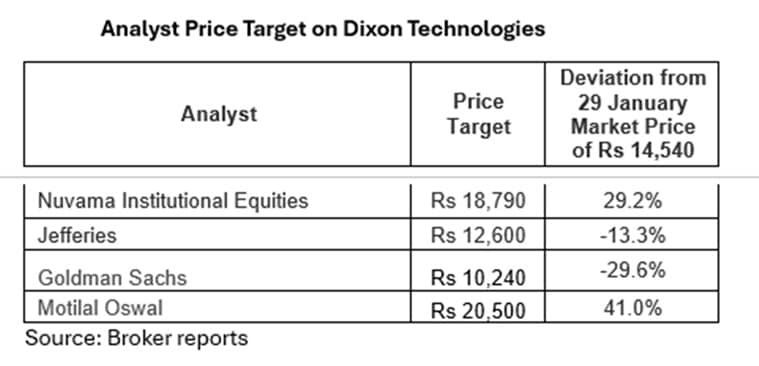

Nuvama Institutional Equities raised its target price to Rs 18,790 (from earlier Rs 16,400), a 29% upside from the current price of Rs 14,540. It has cut the FY25 profit after tax (PAT) estimates for Dixon Technologies by -3% to account for weaker performance of TV. However, it raised the FY27 PAT estimate by 10% to account for Vivo JV and Ismartu acquisition.

However, Jefferies has maintained its ‘Underperform’ rating on the stock with a target price of Rs 12,600, a 13% downside. It believes that a 106x forward price-to-earnings (PE) ratio for FY26 has stretched the risk-reward ratio amidst the expiry of the mobile PLI scheme. Goldman Sachs is further bearish on Dixon and has a “sell” rating with a price target of Rs 10,240 (29.6% downside) as growth moderates and earnings upgrade cycle halts temporarily.

Search for the next growth driver?

At the Q3 FY25 earnings call, Dixon Technologies CEO & MD, Atul Lall, said, “The electronics manufacturing industry in India has reached a level of maturity in terms of device and product manufacturing. To sustain and grow further, a strong component ecosystem is essential.”

The problem with Dixon’s low-margin, high-volume model is that it is only sustainable in high sales volume. A maturing industry means the growth rate will slow in the coming years, making investors question the company’s 147x price-to-equity (PE) valuation. To justify the high PE, Dixon needs a next growth driver that can continue generating strong earnings growth.

That’s where Dixon’s backward integration strategy comes into play. It is looking to foray into the components sector to increase the wallet share from existing customers. Lall noted, “We have already launched a display module, which will become operational in the next two to three quarters, along with mechanical and other modules.”

It is waiting for government subsidies under India Semiconductor Mission (ISM) 2.0 to set up a world-class display fab, which will require around $3 billion in capital expenditure. The display fab will cater to its existing customers across mobile, television, and notebook segments, while also serving other players in the market.

Dixon is also looking to manufacture precision components, mechanicals, camera modules, and battery packs in the component sector. These are high-margin businesses and could accelerate the company’s profits.

What lies ahead

Dixon has almost closed in on its first growth cycle led by mobile EMS. The next growth driver could come from the production of higher margin components sector, IT hardware, and telecom.

Dixon’s share price is sensitive to announcements around PLI, ISM 2.0, and import duty on electronic components. Some sharp stock price movements could be expected around the Union Budget 2025 as the EMS industry has urged the government to extend the mobile PLI scheme ending in FY26 by another five years. Analysts believe that an extension, if any, will come with some riders probably around the design side. Dixon could benefit from its backward integration strategy.

Its stock is trading at a 147x PE ratio, way above the 5-year median PE ratio of 119.6x. However, if we factor in Motilal Oswal’s earnings estimate of 60% CAGR for FY24-FY27 led by backward integration, the stock is trading at 70.1x PE on FY27E earnings. The brokerage has raised the target price to Rs 20,500 for the stock, representing a 41% upside from the Rs 14,540 share price as of January 29. While Dixon Technologies’ present valuation is stretched, the potential for future earnings growth leaves room for another growth cycle.

It will be interesting to see if it can replicate the success of mobile manufacturing in display, telecom, and IT hardware. India’s foray into semiconductor manufacturing could also fuel the company’s interest in exploring printed circuit boards (PCB).

Considering there are a limited number of semiconductor manufacturers whose stocks are trading on the stock exchange, Dixon’s chances may be bright as investors look to participate in India’s semiconductor story.

Note: We have relied on data from http://www.Screener.in throughout this article. Only in cases where the data was not available, have we used an alternate, but widely used and accepted source of information.

Puja Tayal is a financial writer with over 17 years of experience in the field of fundamental research.

Disclosure: The writer and her dependents do not hold the stocks discussed in this article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.