© The Indian Express Pvt Ltd

Tags:

ExplainSpeaking-Economy is a weekly newsletter by Udit Misra, delivered in your inbox every Monday morning. Click here to subscribe

Dear Readers,

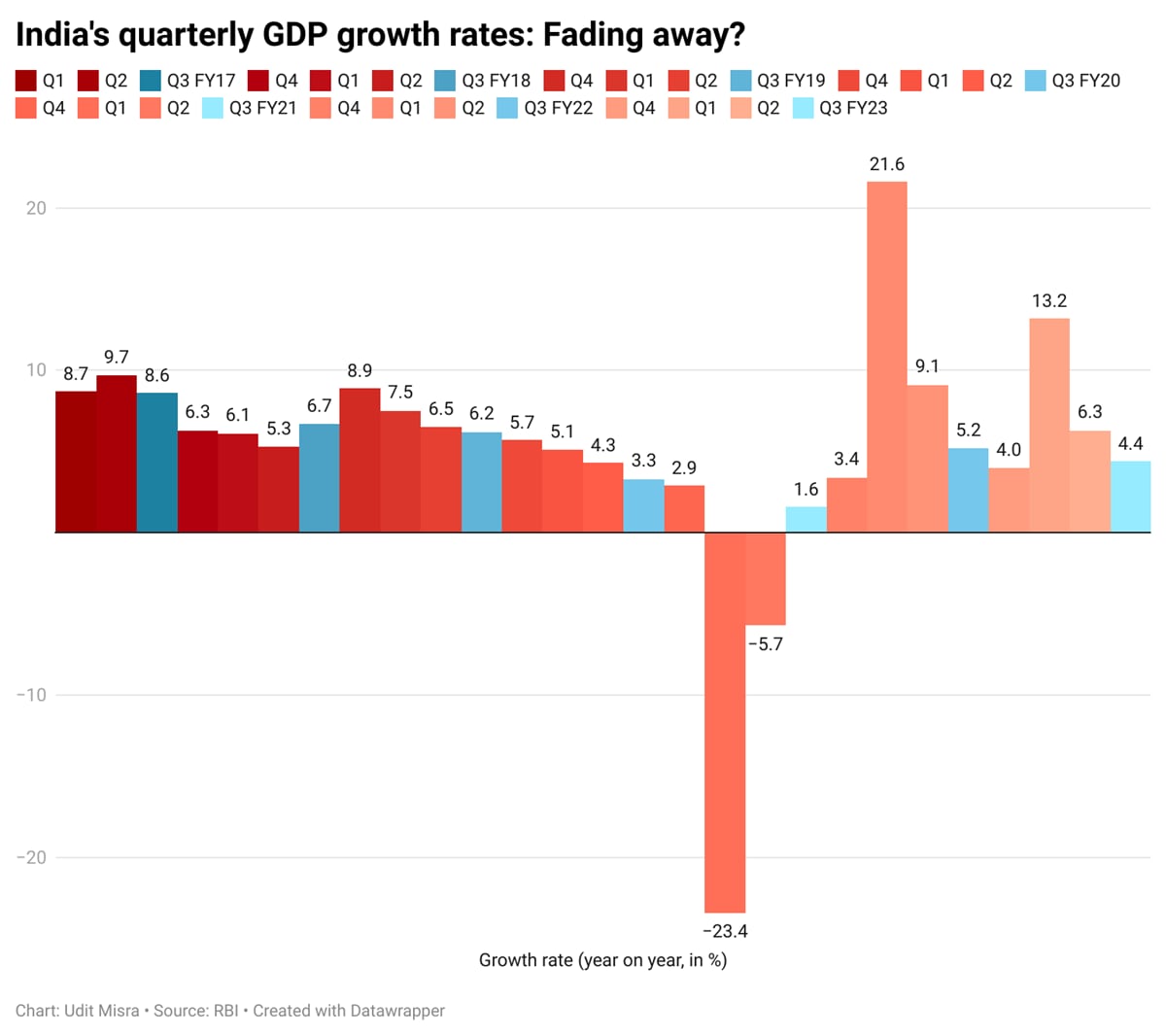

The data in question pertains to India’s GDP growth in the third quarter (October to December, 2022) of the current financial year (2022-23). You can read a detailed explanation on it by clicking here. A key takeaway was that India’s GDP grew at just 4.4% in the quarter ending December 2022.

CHART 1 below stacks up the quarterly GDP growth rates since the start of 2016-17 onwards. The third quarter data for each financial year is highlighted in blue just for ease. The chart brings out the broader point of a steady deceleration in quarterly GDP growth rates.

This has led to two contrasting responses. Economic experts associated with the government such as the current as well as the previous Chief Economic Advisors argued that if the data for the previous years had not been revised upwards, then India’s growth rate would have been much higher. We will come to this point later.

On the other hand, Rajan, who has often voiced his doubts about the health of the economy in the past, pointed to “subdued private sector investment, high interest rates and slowing global growth” as some of the reasons that may further drag down India’s growth rate. It is a fact that the RBI has been raising interest rates since May last year in a bid to contain high inflation. But there is growing unease among policymakers, including within the RBI’s rate-setting body — the six-member Monetary Policy Committee (MPC) — about the effect of higher interest rates on India’s growth.

India’s growth rate — calculated by comparing GDP levels in a year or a quarter to the same period a year ago — has been fast losing momentum since recovering from the Covid-induced (technical) recession in 2020. For instance, in 2021-22, India’s GDP grew by 9.1% but in 2022-23 it is expected to struggle to achieve even a 7% growth rate. Worse, many economists, including Rajan, expect the GDP growth to decelerate to under-6% and possibly closer to 5% in the coming financial year (2023-24) that starts in April.

“I am worried that earlier we would be lucky if we hit 5% growth. The latest October-December Indian GDP numbers (4.4% on year ago and 1% relative to the previous quarter) suggest slowing growth from the heady numbers in the first half of the year,” stated Rajan.

And because India’s recovery pattern has been quite uneven — read K-shaped, wherein the rich get richer and poor get poorer — lower growth rates typically imply fewer new job opportunities, likely job losses, and greater inequality.

“My fears were not misplaced. The RBI projects an even lower 4.2% for the last quarter (January to March 2023) of this fiscal. At this point, the average annual growth of the October-December quarter relative to the similar pre-pandemic quarter 3 years ago is 3.7%,” Rajan said.

“This is dangerously close to our old Hindu rate of growth! We must do better.”

The first thing to know is that contrary to what many readers might believe, the term “Hindu rate of growth” has been in use in India’s economic history literature since 1982 when an Indian economist, Raj Krishna, coined it. To be sure, Krishna was not someone who aligned with the ideologies of the Congress-led governments of that time.

“Chicago-trained and, in the political climate of the time, with a reputation for being somewhat of a right-winger, he (Krishna) was perhaps a more acute observer of the Indian economy than most of his peers,” states Pulapre Balakrishnan, professor of economics at Ashoka University, in his piece titled “The recovery of India: Economic growth in the Nehru era”.

During the Emergency, Krishna was teaching at the Delhi School of Economics. After the Indira Gandhi government was ousted in 1977, he became a member of the Planning Commission under the Janata Party government. During his tenure, the Commission wrote the draft Sixth Five Year Plan. Concurrently, he was also a member of the Seventh Finance Commission responsible for the disbursement of funds to the states.

In 1979, he resumed teaching at the Delhi School and stayed there until his death in 1985. According to The New Oxford companion to Economics in India (OUP), it was “during this period that he coined the memorable phrase ‘The Hindu Rate of Growth’, a polemical device intended to draw attention to the meagre 3.5 per cent growth rate experienced by India over the long run. The fact that this rate of growth remained steady through changes in governments, wars, famines, and other crises, made it for him an inherently cultural phenomenon—hence the name”.

In other words, the term Hindu was not used to denigrate the Hindu community.

In his piece, which readers can find in Uma Kapila’s book titled “Indian Economy since Independence”, Prof Pulapre Balakrishnan provides a context and understanding of India’s growth record during “the Nehru era” (1951 to 1964).

The growth rates of India’s GDP and GDP per capita shot up from 0.9% and 0.1%, respectively, during 1900 and 1946 (the colonial era) to 4.1% and 1.9%, respectively, between 1950 and 1964. Moreover, India’s GDP growth rate of 4.1% during the Nehru era was higher than China’s 2.9% over the same period, although it was lower than the 6.1% rate of Korea. What further puts India’s performance during the Nehru era in context is the GDP growth rate of the US (3.6%), the United Kingdom (1.9%) and Japan (2.8%) between 1820 and 1992.

“It is now possible to place in perspective Raj Krishna’s lament that independent India’s record of growth until the late 1970s placed it lower than 100 economies worldwide. Krishna had used per capita GDP as his measure. This succeeds in masking the degree of progress made in the Nehru era,” write Prof Balakrishnan. Between 1900 and 1946, India’s population grew by 0.8% each year but during the Nehru era, it increased by 2%.

“…we can see that were the rate of growth of population to remain at the colonial rate, the rate of growth of per capita income during 1950-1964 would have exceeded 3%. This is more than twice the rate of growth of per capita income of the US and the UK during 1820-1992, and exceeds that attained by Japan during the same period,” argues Prof Balakrishnan.

He quotes Raj Krishna — “an economist who placed himself at an obtuse angle vis-à-vis the establishment that had donned the Nehruvian mantle” — stating: “If today (1982) we can boast of a large measure of self-reliance (read Atmanirbhar-ta), it is because considerable capacity has been created in the metallurgical, mechanical, chemical, power and transport sectors. These sectors are basic precisely because they are equally indispensable for defence, for large-scale consumer goods production, for small-industry development and rural development.”

At first glance it may appear that India’s growth story turned a corner after the reforms of 1991. But the GDP growth rate data suggests that India started growing faster than the Hindu rate of 3.5% long before the crisis and reforms of 1991.

In a piece published in the Economic and Political Weekly in 2006, the late Baldev Raj Nayar, Professor Emeritus at Canada’s McGill University, argued that while it is certainly true liberalisation accelerates economic growth, “but it is equally true, as more recent work by economists has shown, of the within-system economic policy reforms of the 1980s.”

For instance, according to Nayar’s calculations, India’s average annual GDP growth rate between 1956 and 1975 was 3.4% — almost exactly the Hindu rate of growth. However, between 1981 and 1991 — that is, a full decade before the crisis and reforms — India’s growth averaged 5.8%.

For many economists, such as Arvind Virmani and Arvind Panagariya, 1980 (or the 1980s more broadly) is likely the turnaround year, thanks to the reforms initiated by the governments of both Indira Gandhi (who had returned to power after being “chastised” for enforcing Emergency) and Rajiv Gandhi.

But Nayar points out that the first phase of economic liberalisation started in 1975 — the year in which Emergency was enforced. To buttress his claim he points out that the GDP growth rate between 1976 and 2006 averaged 5.6% — well above the Hindu rate of growth.

India will grow close to 7% this year — that’s twice the Hindu rate of growth. But that is cold comfort given that in the coming year, the growth rate is likely to slip considerably.

In fact, looking back (see CHART 1 above) at the quarterly growth rates there is a distinct trend where growth rate tends to moderate quite considerably from one quarter to another.

In particular, in nine of the14 quarters (a period of three consecutive months) since Q1 (April, May, June) of 2019-20, India’s GDP growth rate was less than 4.5%. Some of the values that were higher than 4.5% have come primarily because of a low base effect; the contraction in GDP during Covid-induced lockdowns in 2020-21 was so severe that it distorted the picture in the first couple of quarters of the next few financial years. But without that low base, the growth rates of Q3 and Q4 have tended to fall within the range of the Hindu rate of growth.

In fact, last year in June, when the Q4 (of 2021-22) GDP data was released, we asked this very question to Prof. Sudipto Mundle, Chairman, Centre for Development Studies and a member of the 14th Finance Commission. You can catch that episode here.

Even that early, Prof Mundle had correctly predicted that India’s growth rate would decelerate from one quarter to another as the financial year progresses.

“(But) we haven’t been there (that is, at the Hindu rate of growth) for a long time. Forget the Covid year. Only in one year (2019-20) we went down to the Hindu rate of growth (GDP had reportedly grown by 3.7% in that financial year). Other than that we generally don’t get there (anymore),” he had said.

“You can, of course, redefine the Hindu rate of growth to be 5%,” he had said jokingly.

But on a more serious note, Prof Mundle had stated that going forward, the debate essentially will be whether India will fall in the 5%-6% range or in the 7%-8% range.

However, the idea of treating 5%-6% as the “new Hindu rate of growth” is not entirely unheard of. In the aforementioned book, editor Uma Kapila writes: “Some analysts believe that the high growth story has come to an end and an average growth rate of 5-6 per cent might be more of a rule and see this as the ‘new Hindu rate’ of growth”.

To be sure, even the current CEA in the latest Economic Survey had agreed that India’s potential economic growth rate (that is, the rate at which India can grow without fueling undesired levels of inflation) had fallen to 6% even before the onset of the Covid pandemic.

But what about the claims by the CEAs that India’s growth is higher if one does not count the revisions of past GDP levels?

It is true that both Chief Economic Adviser (CEA) V Anantha Nageswaran as well as the former CEA Krishnamurthy Subramanian, who is currently Executive Director at the IMF, have argued that India’s Q3 GDP growth is much faster if one ignore the data revisions. Read this report and the tweet below for more details.

But simply put, there is no way one can ignore data revisions if one wants to know the true picture of the economy. The truth is that the economy grew by a certain extent in each of the past years and quarters. The initial estimates — such as the First Advance Estimates etc. — often fail to capture the actual change accurately. That is why NSO statisticians need to have several rounds of revisions — First Advance Estimates, Second Advance Estimates, Provisional Estimates, followed by First, Second and Third Revised Estimates — before arriving at the “Actual” number. These revisions carry on for 5 years before the Actuals are accepted as the final picture.

But it would be a cardinal mistake to imagine that with each revision, stretched over the years, the economy itself was improving with retrospective effect. The economy has already grown — it is only our understanding of it that is getting revised.

As such, ignoring latest revisions just to argue that GDP for the current period is better than what it seems to be, would essentially be an exercise of wilfully ignoring the truth and choosing facts as per convenience.

What is the upshot?

The central message from last month’s data release was, at one level, quite promising. It found that India had grown faster in each of the past three years than what was previously reported. That is the good news.

Of course, a higher base meant that the current year’s growth rate is lower than what was expected.

But, again, the current year’s data is likely to be revised in the coming months and years as better quality data is available.

As things stand today, India is still far from the 3.5% level that is associated with the Hindu rate of growth.

However, it is noteworthy that India had been decelerating in the three years leading up to the pandemic and grew by just 3.9% in the year just before Covid. Further, it is also true that many economists outside of the government suspect that India’s growth rate may falter to around 5%-5.5% in the coming financial year.

If that happens, labelling it as “dangerously close” to the old Hindu rate of growth or simply designating it as the “new Hindu rate” of growth is a personal choice.

Share your views and queries at udit.misra@expressindia.com.

Warm regards,

Udit