© The Indian Express Pvt Ltd

Tags:

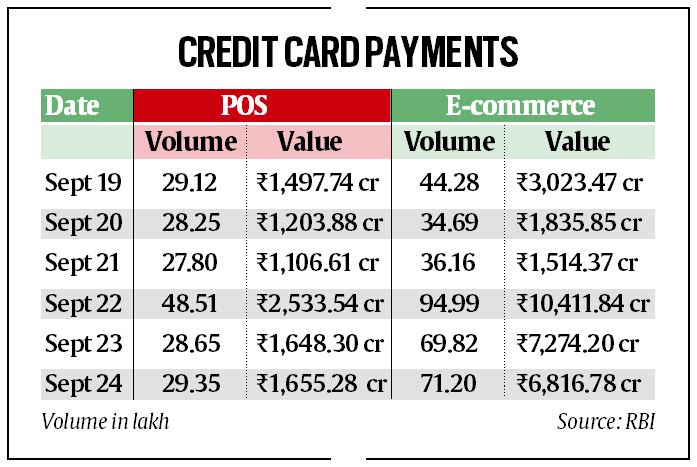

A DAY AFTER the government slashed GST rates, online platforms saw a sudden spurt in consumer spending, with e-commerce transactions using credit cards alone jumping about six-fold in a single day on September 22 to Rs 10,411 crore, according to Reserve Bank of India (RBI) data.

Even on September 23, the momentum remained strong, with Rs 7,274 crore spent through credit cards in close to 70 lakh online transactions, suggesting that shoppers were in no mood to slow down.

Point-of-sale (POS) transactions more than doubled to Rs 2,533 crore on September 22 from Rs 1,106 crore the previous day, RBI data shows.

The surge wasn’t limited to credit cards. Debit card transactions also reflected the shopping spree.

On September 21, purchases worth only Rs 193 crore were made using debit cards. But on September 22, spending soared more than four times to Rs 814 crore through 14.33 lakh transactions, as consumers across the country eagerly tapped into the festive-feel discount wave sparked by the GST cut.

Payments through UPI platforms also rose to Rs 82,477 crore on September 22 as against Rs 60,320 crore on the previous day, according to RBI data.

Retailers and banks are rolling out festive offers and special packages to cash in on the recent GST cuts, which cover a wide range of products from FMCG goods to automobiles. The timing coincides with the festive season, adding momentum to consumer demand. Spending is expected to stay strong in the run-up to Diwali as shoppers take advantage of lower prices and discounts. However, questions remain about whether this surge in demand will last once the festive cheer fades and the one-time boost from the GST reduction tapers off, a banking source said.

Arun Nayyar, Managing Director and CEO of NeoGrowth said: “Digital payments in India have moved on from being an urban privilege to becoming a national standard. What we are witnessing is a behavioural transformation, powered by technology. From kiranas to kiosks, India’s retailers are redefining adoption and efficiency in digital modes of transacting.”

“This is accelerating the formalisation of the economy by creating digital trails. At the same time, it’s generating rich data and laying the groundwork for more democratic access to credit. We believe this shift is not just about convenience of payment, it’s about trust in a future-ready ecosystem,” Nayyar said.

Digital retail transactions — from UPI payments to credit and debit cards — have become an integral part of daily consumer spending in India, with adoption continuing to rise nationwide. The top 29 cities in India are rapidly closing the digital gap, with digital spends now accounting for 74 per cent of all retail transactions, up from 45 per cent two years ago.

In other words, out of every Rs 100 spent on retail in these 29 cities, Rs 74 is paid digitally. This surge reflects a deep behavioural shift among consumers, who are increasingly choosing convenience and speed of transacting digitally, according to a NeoGrowth NeoInsights study.

India’s digital payment habits are now deeply embedded into everyday life. From personal grooming (83 per cent) to grocery runs (68 per cent) to vehicle maintenance (80 per cent) digital retail transactions rule across both discretionary and essential categories. While groceries (68 per cent) and fuel (63 per cent) are fast catching up. Cities such as Hyderabad (82 per cent), Bengaluru (79 per cent), and Pune (79 per cent) lead digital payments adoption in the top cities, while Visakhapatnam (76 per cent), Nagpur (71 per cent), and Chandigarh (68 per cent) rank highest among the cities beyond metros, the study said.

In contrast, cities such as Ahmedabad (60 per cent), Kolkata (55 per cent), Jamshedpur (54 per cent), Madurai (52 per cent), and Rajkot (48 per cent) still rely more on cash, the study said. The gap, however, is not driven by lack of access but by behavioural factors. A continued reliance on cash transactions, along with resistance to changing familiar payment habits, has likely slowed the adoption of digital payments.