© The Indian Express Pvt Ltd

Tags:

Competition among industry giants has always existed in the food sector. From Pepsi versus Coca Cola to McDonald’s versus Burger King, legendary rivalries have driven marketing and operational innovations. But the biggest disruptor in this rivalry is always consumer behaviour.

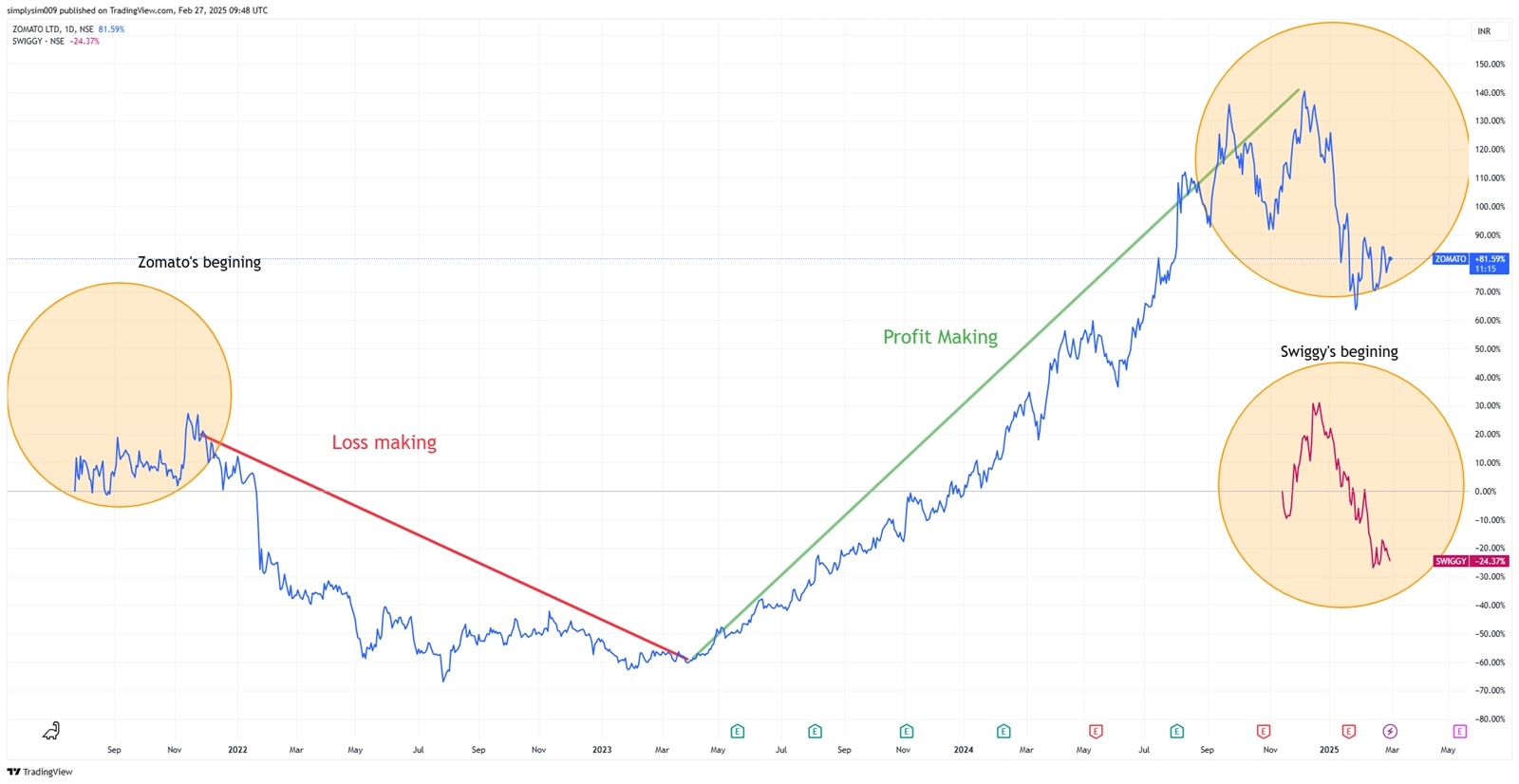

India’s own food tech rivalry — Zomato versus Swiggy — is playing out, with both vying for the same customers. While their marketing and new launches have always made the headlines, this year they will be making headlines in the stock market.

Though the two operate in the same business, their strategies differ.

📌 Zomato focuses on faster execution and increasing market share through company acquisitions, aggressive marketing, and new customer additions.

📌 Swiggy focuses on innovation to get the first-mover advantage and organic growth through improved efficiency and customer retention.

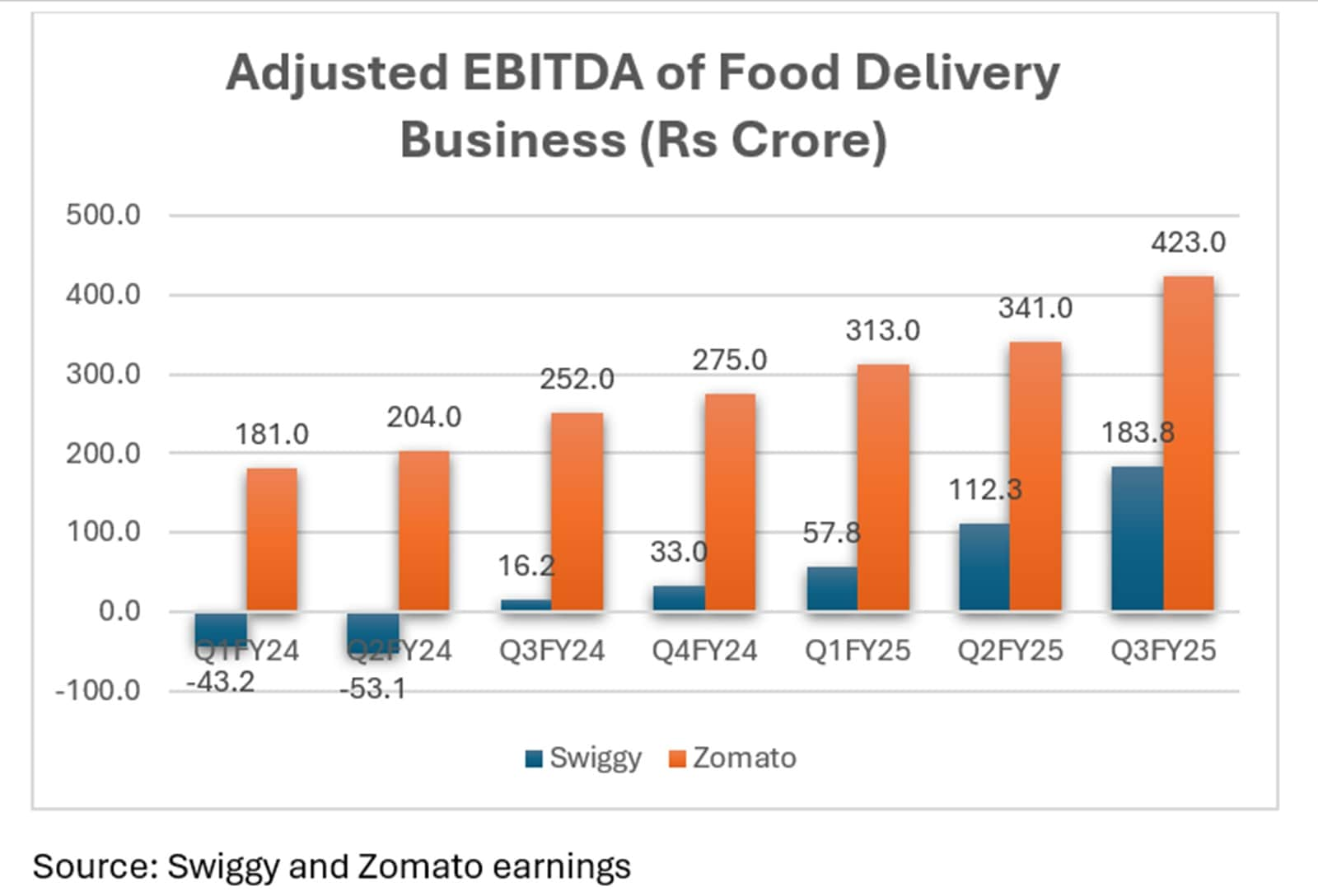

This difference in their approach has placed Swiggy two years behind Zomato in key metrics like gross order volume (GOV), monthly transacting users (MTU), number of dark stores, revenue, adjusted EBITDA, market share, and market capitalisation.

In the low-margin, high-volume business of food delivery and quick commerce, Zomato moved early to tap the capital markets, launching its IPO in July 2021, raising Rs 9,375 crore. But while the stock market opens opportunities to raise significant capital, it is also brutal with losses.

Initially, Zomato faced shareholders’ backlash due to losses. This led to a strategic shift from revenue growth to profit. In Q3 FY23, it closed its operations in 225 cities with weak performance. Soon, operating efficiencies kicked in, and Zomato reported its first operating profit of Rs 12 crore in Q1 FY24. There was no looking back, with the company growing its adjusted EBITDA to Rs 330 crore in Q2 FY25.

Swiggy finally made its stock market debut more than three years after Zomato.

Looking at the stock price trends, Swiggy seems to be repeating Zomato’s story. Zomato stock fell 70% between November 2021 and July 2022 as the overall market turned bearish. Swiggy too has entered a bear market and has dipped 40% from its high. Like Zomato, Swiggy is now under pressure to turn profitable. It aims to break even by December 2025 by expanding its dark stores and boosting its marketing budget.

Interestingly, the stock price charts of the two companies mirror each other. On January 21, the shares of Swiggy and Zomato fell 8% and 10.5%, respectively on NSE after Zomato reported a slowdown in the food delivery business in Q3. Such reactions show the dynamo effect one has on the other.

While Swiggy has just entered the bourses, Zomato is making it to the big leagues with its entry into the Nifty 50 Index in the upcoming Index reshuffle on March 27, 2025.

There are two questions in every investor’s mind:

📌 Does Swiggy’s entry into the stock market threaten Zomato stock’s upside potential?

📌 Can Swiggy repeat Zomato’s last two years rally of 550%?

Analysts currently favour Zomato over Swiggy because of the former’s numbers. Bernstein has an ‘outperform’ rating on Zomato, with a price target of Rs 310, representing a 36% upside from the current trading price of Rs 227. It believes Zomato can continue building its market leadership in quick commerce.

It remains to be seen if a different story unfolds for contrarian investors in the long term.

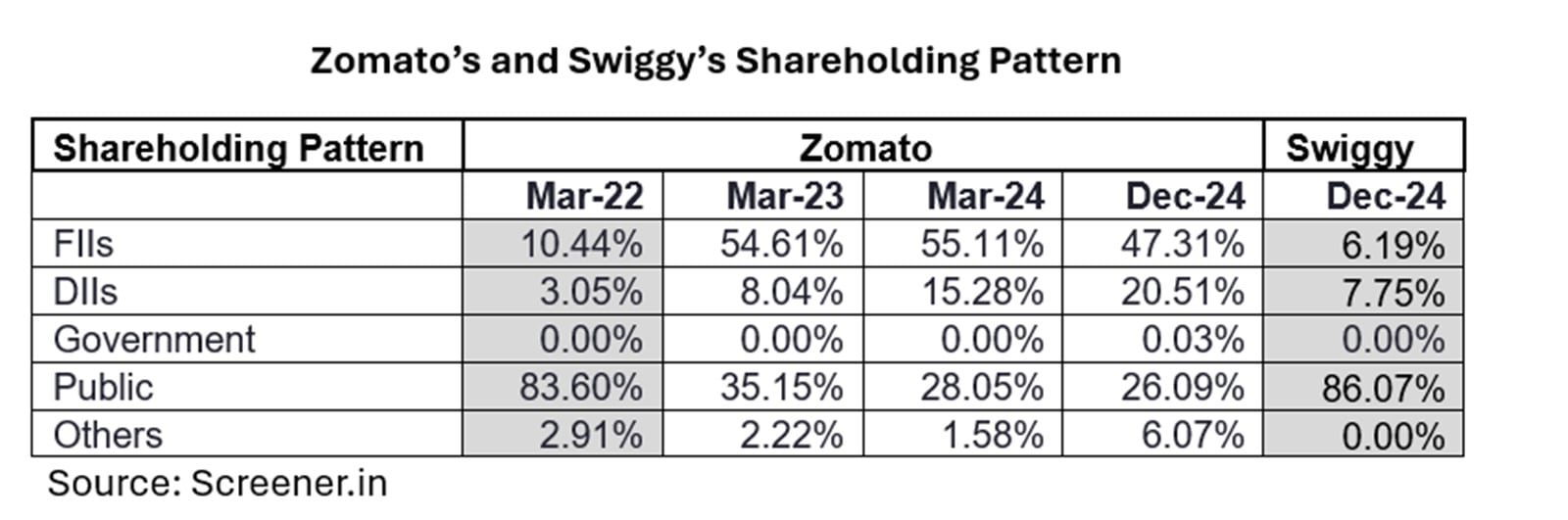

Until now, Zomato has been the focus of public investors interested in food delivery and q-commerce. Foreign Institutional Investors (FIIs) and Domestic Institutional Investors (DIIs) increased their holdings in Zomato from 10.4% and 3.05% from March 2022 to 55% and 15.3% in March 2024.

The increasing investments inflated Zomato’s stock valuation to a price-to-earnings (PE) ratio of 561x in July 2024. From this point, FIIs started selling their holdings in Zomato to 52.53% in September 2024. In December 2024, Zomato’s Rs 8,500 crore QIP diluted FII holding to 47.31%. The stock price dip has reduced its PE ratio to 328x.

In the shareholding pattern, Swiggy is starting on a similar note, with more than 80% of public holdings. At present, it is playing catch up with Zomato on the adjusted EBITDA of the food delivery business.

Swiggy’s efforts to turn profitable could attract the attention of FIIs and DIIs, giving it more upside potential than Zomato, which is already trading on high valuations. It remains to be seen if Swiggy can repeat Zomato’s 550% rally. It might have to overtake its rival in the market share and profit margins. The one with a better return on capital employed (ROCE) could win investor confidence in the long term.

At present, Zomato is leading with an ROCE of 1.14% against Swiggy’s -24.4%.

It could open up investing from index funds that track the Nifty 50. But with great capital comes great expectations of returns. Zomato faces the pressure of growing profits to justify its 328x PE ratio.

Until now, it has reported positive earnings per share (EPS) because it invested its IPO money in fixed-income instruments and earned interest income. Excluding this income, Zomato is still making net losses because of high depreciation. The focus could gradually shift from adjusted EBITDA to EPS, as it enters the even more competitive large-cap Nifty 50 Index.

While the food delivery business could bring stability, quick commerce could be the earnings growth driver for Zomato.

In November 2024, the rivalry intensified.

📌 Swiggy raised Rs 11,327 crore through IPO.

📌 Zomato raised Rs 8,500 crore through a qualified institution placement (QIP).

📌 Zepto raised $350 million in funding from private investors.

All three are betting on dark stores to make quick commerce more competitive and cost-effective. Dark stores are like mini-fulfillment centers, where fast-selling items are stored to execute orders quickly. The closer the dark store is to customers’ locations, the faster the delivery, the lower the delivery cost, and the higher the delivery charge.

Zomato, Swiggy, and Zepto are looking to tap the quick commerce market which CLSA expects to grow from $3.8 billion in FY24 to $10 billion by FY26.

Zomato’s Blinkit is currently leading with a 39-40% market share, followed by Swiggy’s Instamart (28%) and Zepto (28%).

Blinkit and Instamart are expanding their dark store network. In Q3 alone, Blinkit added 216 stores while Instamart added 96.

Blinkit has 1,007 stores and plans to add another 1,000 this year. More than half of the new stores will be in the top 8 cities, 20% in new cities, and the remaining in non-serviceable areas near major cities.

Instamart, on the other hand, has 705 stores and has no specific target on the store count addition. However, it is focused on densification and increasing the size of existing stores so it can serve more goods from the same stores. It has no plans to enter unserviced areas.

A dark store becomes profitable once it starts processing 1,000 orders per day. The time for a dark store to break even is also different. While Zomato says it takes 2-3 months, Swiggy says it takes 6-9 months.

Both have different approaches to moving ahead in the quick commerce space. Yet again, the numbers favour Blinkit as the economies of scale kick in. Its contribution margin stands at 3% in Q3 FY25 while that of Instamart is at -4.6%. Instamart aims to achieve break-even on contribution margin by Q3 FY26 as the percentage of mature stores increases. Macquarie noted that Instamart can break-even if it improves its average order value to Rs 600 from Rs 534 in Q3 FY25.

Quick commerce is still in the infancy stage. These numbers may not determine the market leadership yet as the competition picked up in the last six months. Currently, all players have ample capital to pour into dark stores and marketing.

Investors believe quick commerce volumes are huge enough to absorb all the new capacity dark stores are bringing into the market. But what if the demand falls? That is a risk the duo has to take. One cannot grow conservatively in a fast-growing, high-volume market.

The real deal would be converting quick commerce orders into profits by achieving economies of scale. The sheer volume of that business and the high delivery charges it attracts can overtake food delivery orders and help Zomato and Swiggy report positive EPS after excluding the “other income”.

Numbers keep changing in a fast-growing, dynamic, and highly competitive market like quick commerce. Swiggy was ahead of Zomato in food service until January 2020, when Zomato overtook it with the acquisition of Uber Eats.

While service price is a determining factor in such competition, it is customer experience that is the disruptor. Zomato and Swiggy are operating in a market where people are paying for convenience. Open Network for Digital Commerce (ONDC) tried disrupting the Swiggy and Zomato food delivery dominance by charging restaurants lower commission (around 3% as compared to 25%) but has so far not posed a threat. It’s been Swiggy versus Zomato all along, despite the entry of new players.

Zomato and Swiggy are unlikely to enter into a price war, given the wafer-thin margins they operate on.

Investors have already priced in hyper-growth in the stock prices, with Zomato and Swiggy trading at price-to-sales ratios of 12x and 7x, respectively. These ratios complement their 69% and 36% annual sales growth, but the valuations are still stretched.

Right now the competition is just heating up. It will be interesting to see how the opportunity unfolds and whose approach brings returns.

Note: We have relied on data from http://www.Screener.in throughout this article. Only in cases where the data was not available, have we used an alternate, but widely used and accepted source of information.

Puja Tayal is a financial writer with over 17 years of experience in the field of fundamental research.

Disclosure: The writer and his dependents do not hold the stocks discussed in this article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.