© The Indian Express Pvt Ltd

Tags:

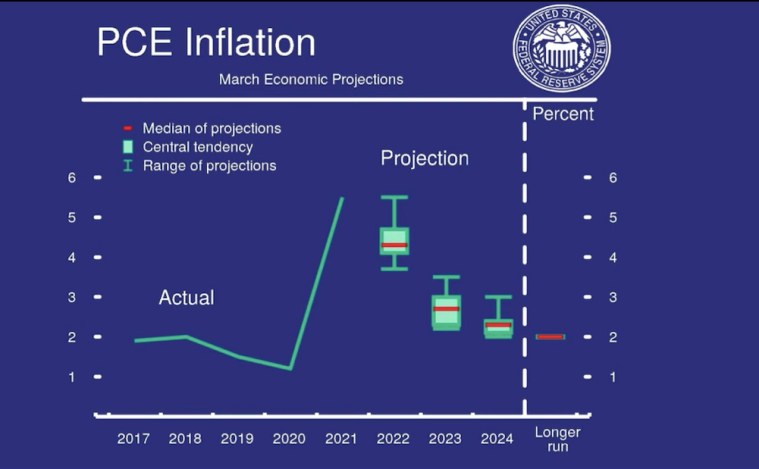

In its first hike since 2018, the US Federal Reserve on Wednesday raised interest rates by 25 basis points and outlined an aggressive stance that also includes balance sheet reduction aimed at fighting record high inflation. The Fed projected that its policy rate would hit a range between 1.75 per cent and 2 per cent by year’s end, arguing that the ongoing increases will be appropriate to curb inflation, the highest in 40 years at 7.9 per cent in February. It also cited the war in Ukraine as creating additional upward pressure on inflation, with global commodity prices remaining elevated.

Federal Reserve Chairperson Jerome Powell said at a press briefing that inflation is expected to start cooling off by the second half of the year and fall to its target level of 2 per cent by 2024. The strong US economy should be able to expand even with a less accommodative monetary policy. “All signs are that this is a strong economy, indeed, one that will be able to flourish, not to say withstand, but certainly flourish in the face of less accommodative monetary policy,” he said.

Markets responded positively to the clear path outlined by the world’s largest central bank, with US markets closing higher by 2 per cent and Indian stock markets opening with a gap of more than 1 per cent on Thursday. Commodities retreated with the Brent crude oil falling and remaining below $99 per barrel, sharply lower than the $139 per barrel recorded just a few days ago.

Going forward, Indian and global markets are expected to stay positive as three major uncertainties seem to be over — the Assembly elections in five Indian states, the US Fed’s decision, and signs of the Russia-Ukraine conflict entering a resolution phase. Any spike in commodity prices could cause corrections in equity markets, even as the broader trend of rising stock prices remains intact.

The Fed’s decision to hike rates and rising domestic retail inflation rate will have a direct bearing on the Reserve Bank of India’s monetary policy review at the next meeting of the Monetary Policy Committee scheduled between April 6 and April 8. Unlike the US Fed, which has clearly reversed course from its accommodative monetary policy, the RBI continues to hold an accommodative stance. This is partly because the retail inflation in India has not breached the set target range of the RBI.

As per recent data, domestic retail inflation rose to an eight month high of 6.07 per cent in February, breaching the upper tolerance level of medium-term inflation target of 4+/- 2 per cent for the second month in a row.

Some economists argued that the RBI may have to revise upward its inflation forecast as inflationary pressures are becoming generalised. A reassessment of the current accommodative stance of the central bank is also possible. This is the fifth consecutive month of rising inflation. Retail inflation was at 6.01 per cent in January 2022 and 5 per cent a year ago. The RBI has projected retail inflation at 5.3 per cent for FY22, with Q4 inflation at 5.7 per cent before easing to 4.9 per cent in Q1 FY23.

According to the Finance Ministry, two months of over 6 per cent retail inflation cannot be seen as a breach of the upper band of RBI’s target, and crossing of the inflation rate above the 6 per cent band “for a particular month cannot be construed as breach of target”.

“Breach of this inflation target is construed only when: (a) the average inflation is more than the upper tolerance level of the inflation target for any three consecutive quarters; or (b) the average inflation is less than the lower tolerance level for any three consecutive quarters,” as per the ministry. Therefore, the RBI has room to stay the course on its present stance, despite some risks from elevated commodity prices. The fact that Brent crude oil has retreated sharply below $99 a barrel should provide additional comfort to the central bank.

Some policy makers also believe that since the fiscal policy is in “contraction” mode, the monetary policy must maintain an accommodative stance. The government has pegged the fiscal deficit at 6.4 per cent of GDP in 2022-23, down from 6.9 per cent in 2021-22 and 9.2 per cent in 2020-21.

“From the levels of 9.2 per cent, the fiscal contraction next year will almost be 3 per cent, now this is a huge contraction. At a time when fiscal policy is in contraction, and private consumption is still below previous levels with no likelihood of economy overheating, the monetary policy must remain accommodative under such circumstances,” an official said, indicating why the government expects RBI to continue to hold an accommodative monetary policy stance.

Newsletter | Click to get the day’s best explainers in your inbox