© The Indian Express Pvt Ltd

Tags:

Dear Readers,

The Indian economy was one of the biggest global stories of last year. That’s because the pace of India’s GDP growth surprised everyone, even the domestic policymakers. India’s performance relative to the rest of the world made it stand out even more. Think about it: At a time when almost all of the developed world was, and is, struggling to avoid recession, India set itself up to grow by over 7%, and even at this high level of growth still beat street expectations of its economic growth by more than a percentage point.

2023 also saw China, which was until recently the main country receiving the attention of global investors, get further mired in an economic slowdown. Geopolitically, India is getting closer to the US, the world’s largest economy, just as China and US relations have started plummeting.

Since the start of the Covid pandemic, global investors have started looking for ways to diversify into other economies in a bid to find China’s substitute. There are a bunch of names across different continents — such as Mexico and Vietnam — but none of them come with the unique advantage of sheer size that India has.

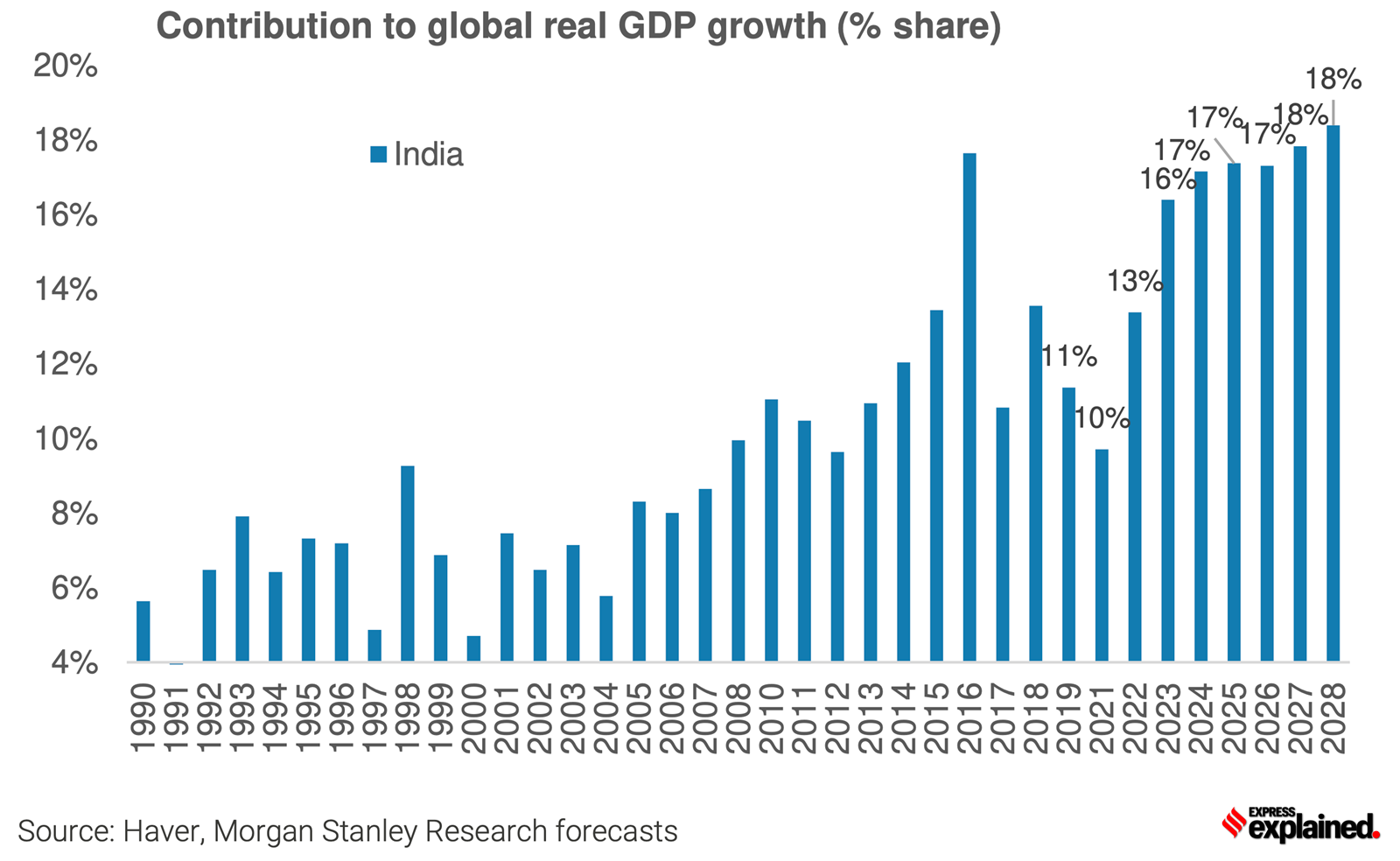

So India’s attractiveness is not just because it may prove to be a production base that may substitute China but also because India can be a massive domestic market. With a considerable young population and the national ambition to make per capita incomes rise 5-6 times the current levels, India can be the next China, the next engine of global growth (see CHART 1).

If global investors are convinced of India’s long-term potential, India can receive a lot of funding and this, in turn, can provide the Indian economy with the one factor of production it lacks: capital.

Three key concerns

But foreign investors have three main reservations as things stand. In a recent research note, economists at Morgan Stanley, which is one of the biggest and most influential investment banks in the world, details the three main concerns.

Having a large population helps a country both in being more productive as well as being a huge market. If the domestic market is big enough, it can make a lot of economic activities viable, even profitable. Smaller economies often have to depend on other countries to build momentum. Think about the Indian Premier League and how it became a reality when the Indian economy reached a certain threshold. Since then, the IPL has only grown in profitability from one year to another.

But a large population makes sense only when the large population can spend money. A large number of poor people or people with low purchasing power will matter little.

In India, almost 55% to 60% of its GDP is because of the money spent by common Indians in their personal capacity. To be sure, the GDP of any country is calculated by adding up all the money spent by different economic entities — people, governments, and businesses — in a year. In other words, the purchasing power of Indians is the biggest engine of India’s GDP growth. It may appear insignificant but it is not. For perspective — all the money spent by governments in India is just one-sixth in comparison.

So if India has to grow its share of the global GDP and indeed become an engine of global growth, the health of its biggest internal engine is critical.

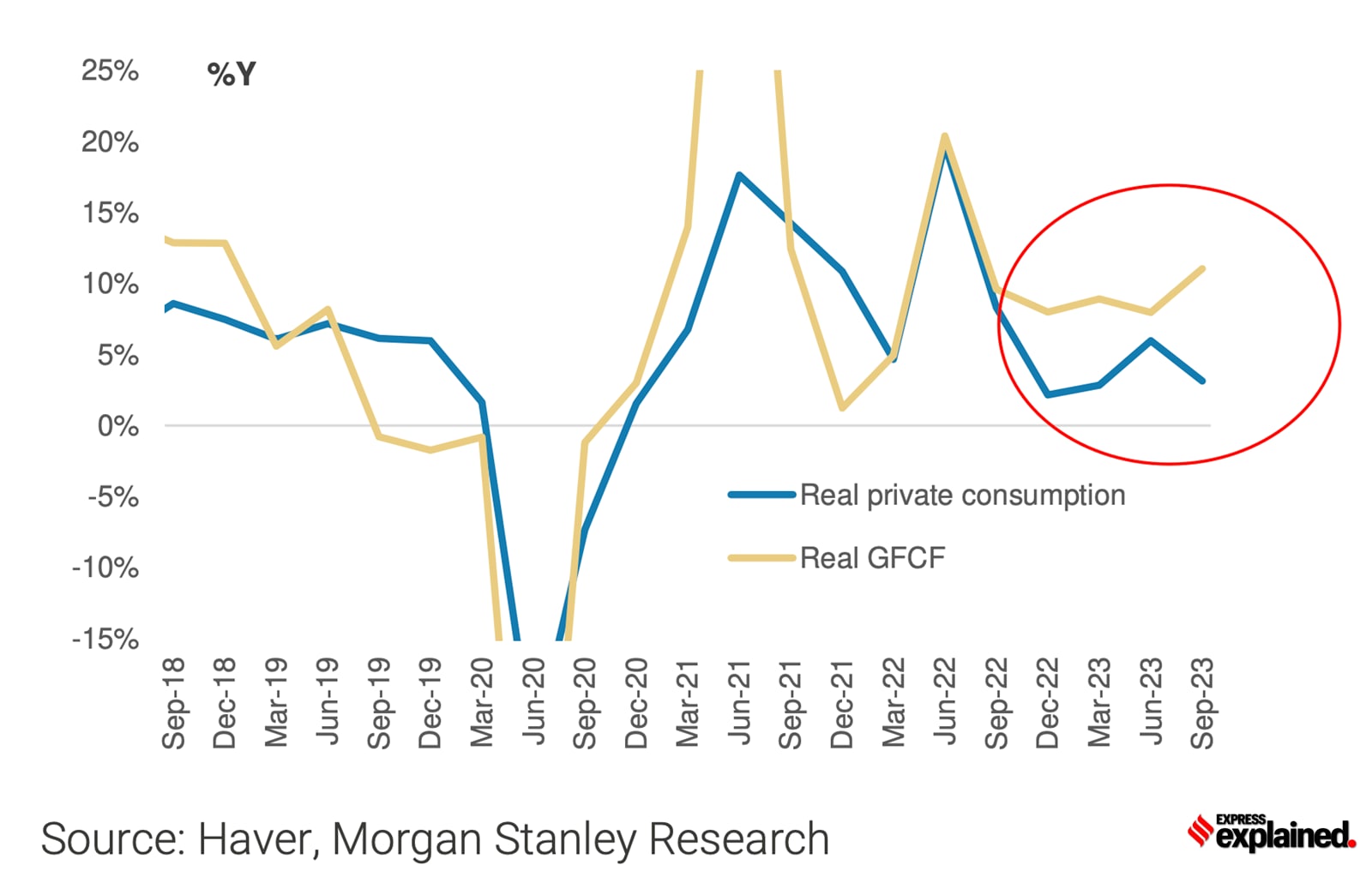

But this is where India’s GDP story has its biggest weak spot. For the longest time — and regular readers of ExplainSpeaking would have noticed this — GDP growth data repeatedly reveals that the so-called “private consumption demand” is quite weak. This is a trend that has been there since before the Covid pandemic (see the blue line CHART 2).

“Within domestic demand, it is the case that private consumption, weighed down by low- and medium-income segments, has been the relative laggard of the recovery since 2H22 (second half of 2022),” states the MS research note. Why has this happened? Partly this has to do with the fact that Covid pandemic hit the Indian economy at a time when it was already slowing down — India’s GDP growth rate in 2019-20 was less than 4%.

Moreover, unlike many European countries or the US, in India, the government did not provide as much direct financial help to households. This meant that people either ran down their savings or cut expenditures.

The Russia-Ukraine war only made matters worse by spiking inflation and further robbing people of their purchasing power. Predictably, even though the consumption levels among the rich Indians have recovered, the bulk of India still continues to struggle. “Whenever we start to discuss the consumption outlook with investors, the first thing we invariably hear is that there is no rural recovery at all,” states the MS economists.

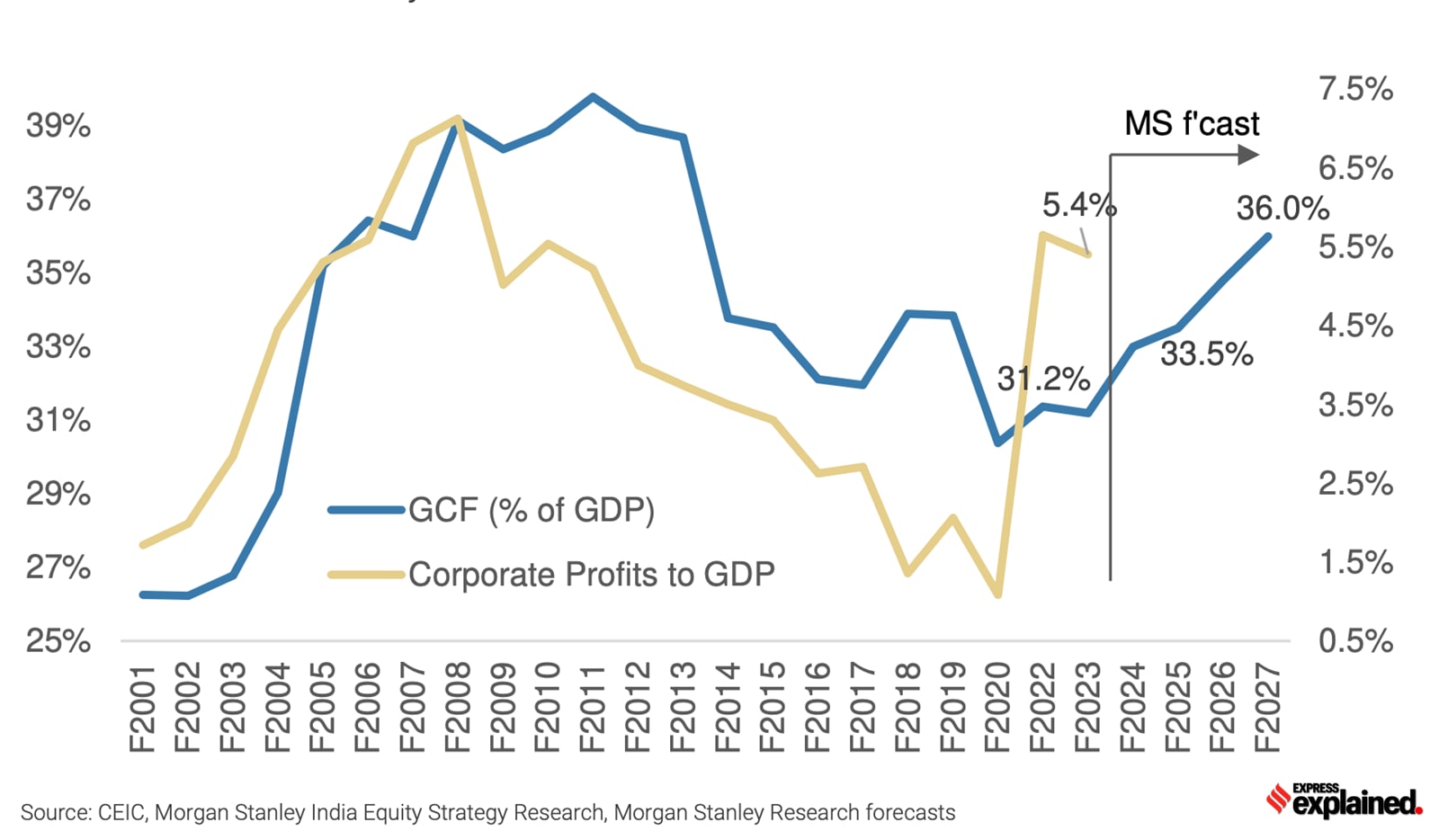

The money that businesses and governments spend towards increasing the productive capacity of the economy — say a building, a bridge, a factory or buying new computers for the employees — is called the “investment demand” (even more technically called Gross Fixed Capital Formation or GFCF) and, after private consumption demand, this is the second biggest engine of India’s GDP, accounting for around 30% of India’s GDP.

Now, on the face of it, India’s spectacular success in the current financial year is because of this investment demand (see the yellow line in CHART 2 above).

But again, there is fly in the ointment: The bulk of the growth has come because the government has been taking the lead.

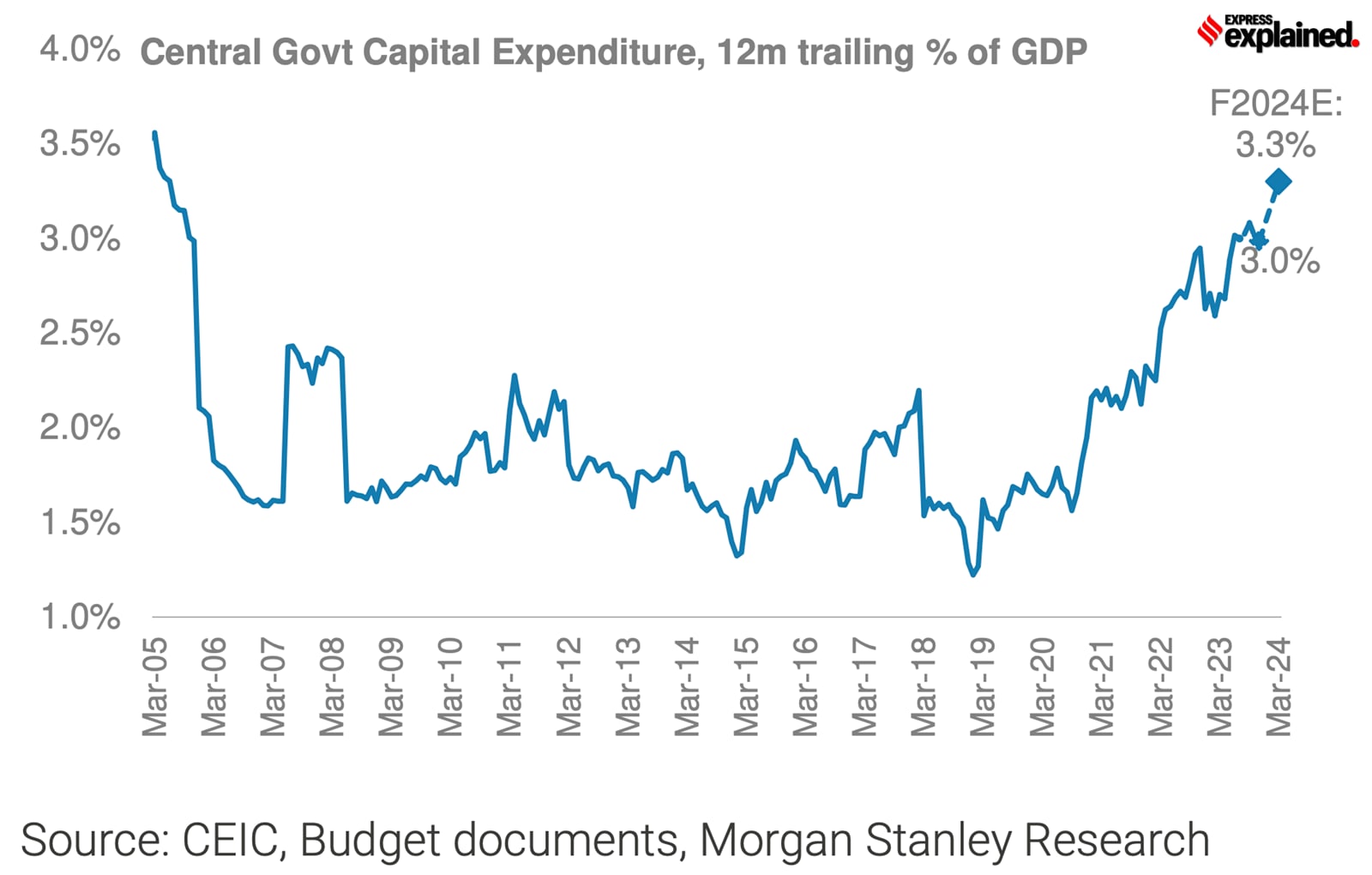

“Public capex has been strong with the central government’s capex to GDP ratio rising to 3%, an 18-year high (see CHART 3). Moreover, state-level capex data for 19 states show a renewed acceleration in state capex growth,” notes the MS note.

Capex essentially means capital expenditure — or the expenditure towards creating anything that allows new production possible; Capex is different from revenue expenditure, which involves payments towards day-to-day expenditures such as paying salaries.

In any economy, if businesses are investing in boosting productive capacities, it means they expect private consumption demand to rise or stay buoyant.

But this is exactly the reason why global investors are circumspect. While it is true that high investment demand augurs well for any economy, it is also true that businesses would not continue to invest endlessly unless domestic consumer demand comes into its own. If people do not start demanding new and more goods and services, the economy would struggle to grow as fast as many hope. Moreover, in India’s case, the rosy estimates of investment demand lean heavily on government spending.

A global investor may justifiably be worried about both the trends — weak consumer spending and limits to the government’s ability to keep spending.

“The latest policy documents from RBI were somewhat hawkish, prompting some investors to ask what if RBI does not cut rates,” states the MS note. Hawkish suggests that the central bank is more concerned about containing inflation than boosting growth.

When interest rates are low, it incentivises businesses to borrow money from the banks and create fresh assets. By the reverse logic, persistently high interest rates disincentive borrowing and drag down economic activity in the economy.

Typically, the RBI keeps interest rates high (or refrains from cutting them) if it believes that inflation is uncomfortably high. Since November and December, the inflation rate has started going in the wrong direction.

Thanks to the persistent inflationary pressures, forecasts of a cut in interest rates have been repeatedly pushed back. Most economists now expect RBI to cut rates in August 2024.

What is likely to happen?

To be sure, all three concerns are related. High interest rates will dampen the already struggling consumer demand, which, in turn, will dissuade businesses from jumping in and start boosting productive capacities in the Indian economy.

Morgan Stanley, which in October 2022 came out with a detailed note titled “Why This Is India’s Decade”, has been quite optimistic about India’s prospects.

On these three concerns too, Morgan Stanley’s team remains resolutely optimistic: “We are expecting a virtuous growth cycle to be sustained – where capex brings job creation, income and productivity growth, which in turn lift consumption activity,” states the research note. See CHART 4 to understand why MS economists believe that the investment cycle has inflected.

There are only two risks to the growing enthusiasm in their view.

One, electoral reversals for the incumbent government.

“In our view, the key risk would be the emergence of a weak coalition government, which could result into a pivot back towards redistributive policies at the expense of the focus on boosting capex and implementing supply-side reforms”.

Two, “a number of geopolitical tensions which could disrupt global trade and investment flows”. A slower world economy will also drag down India’s growth as well while a fast growing global economy will work like booster jets.

Until next time,

Udit