© The Indian Express Pvt Ltd

Tags:

Finance Minister Nirmala Sitharaman announced several changes that brought cheer to the middle class.

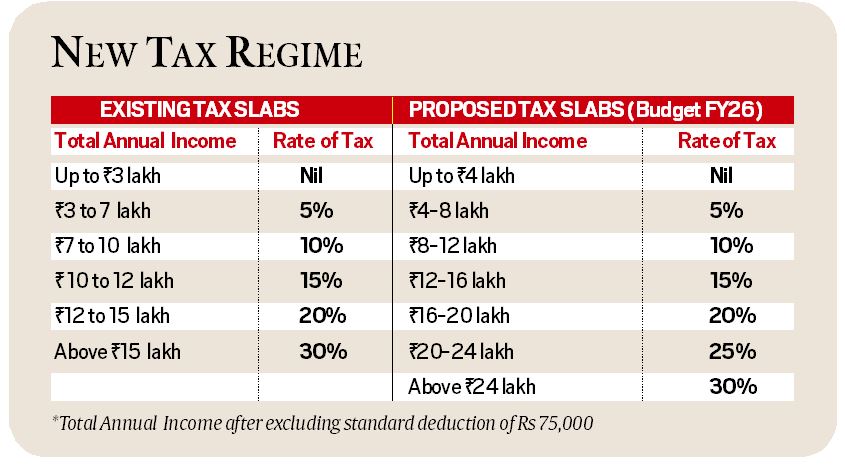

Starting from raising the limit of rebate from Rs 7 lakh to Rs 12 lakh under the New Tax Regime (NTR), Sitharaman also tweaked the tax slabs in a manner that would benefit taxpayers in higher salary brackets as well, effectively leaving more money in their hands.

This sweetening of the NTR, the government hopes, will lead to more taxpayers opting for the simple and exemption-free new regime over the exemption-heavy old regime. In fact, the changes in the NTR could be the final nail in the coffin for the OTR.

A rebate means that income up to that limit will not lead to any tax liability, which effectively means that anyone with an annual taxable income of up to Rs 12 lakh, or a monthly income of up to Rs 1 lakh, will not be required to pay any income tax under the NTR.

However, if the annual taxable income breaches Rs 12 lakh, it will be subject to tax as per the prevailing tax slabs for the entire income.

This comes as a huge relief for all those earning between Rs 7 lakh and Rs 12 lakh. While an individual earning Rs 12 lakh per annum had an annual tax liability of Rs 80,000, she will have to pay no income tax in the financial year 2025-26.

Rs 12 lakh taxable income is same as Rs 12.71 lakh

While those earning up to Rs 12 lakh a year will have zero tax liability under NTR, the tax outgo would shoot up to Rs 61,500 if the taxable income breaches Rs 12 lakh by just Rs 10,000. Thus, an employee having an annual taxable income of Rs 12.1 lakh would actually take home Rs 51,500 less than the one earning Rs 12 lakh.

A back-of-the-envelope calculation shows that parity is achieved only at the income level of Rs 12.71 lakh in terms of take home salary. At Rs 12.71 lakh, the tax is Rs 70,500, which means the take-home salary at that level would be almost equal to Rs12 lakh.

Under NTR for the financial year 2024-25, an individual with a taxable income of Rs 15 lakh would have a tax liability of Rs 1.4 lakh. However, following the tweaking in tax slabs in the budget 2025-26, that liability comes down to Rs 1.05 lakh.

This means an individual earning Rs 15 lakh, would have an additional saving of Rs 35,000 purely on account of tweak in the tax slabs as the income between Rs 12-16 lakh will now be taxed at 15 per cent as against an earlier tax rate of 20 per cent tax for taxable income between Rs 12-15 lakh.

There are bound to be higher savings for those earning Rs 20 lakh and those earning between Rs 20 and Rs 24 lakh as the tax rate has been brought down for that income bracket. While income above Rs 15 lakh currently attracts a tax rate of 30% under NTR, the changes in tax slabs and rates prescribe a rate of 20% for the Rs16 lakh-20 lakh income bracket, and 25% for the Rs 20 lakh-24 lakh bracket.

By virtue of this change in slab rate, while an individual with taxable income of Rs 20 would have paid a tax of Rs 2.9 lakh under the existing NTR, it would now come down by Rs 90,000 to Rs 2 lakh for the upcoming financial year.

For those earning between Rs 20 lakh and Rs 24 lakh, there are additional savings as that income would now be taxed at 25% as against the current NTR rate of 30%. So, as per the Budget proposal, an individual earning Rs 24 lakh would have a tax outgo of Rs 3 lakh in 2025-26, instead of Rs 4.1 lakh in 2024-25.

So far, those claiming heavy deductions under OTR — particularly on account of house rent — found the old regime significantly beneficial in terms of lower tax outgo vis-à-vis NTR. This made a sizable number of taxpayers loath to migrate to the new regime. But with further sweetening of NTR, while there may still be a few scenarios in which OTR may be beneficial, gains in most cases would be far more diminished.

It is likely that more taxpayers may move to NTR even if they have to pay a marginally higher tax, as the move to the simplified NTR will save them the hassle of claiming heavy deductions.

It should be noted that for claiming such high deductions under OTR, the taxpayer may be forced to make certain exemption-eligible investments that she may otherwise not be keen to make.

A rough calculation shows that while an individual with a gross salary of Rs 15.75 lakh (pre-standard deduction) would have to pay a tax of Rs 1.27 lakh under the OTR even after he claims deductions of up to Rs 4.75 lakh (including section investments under 80C, home loan interest outgo, health insurance for self and parents, and investment of Rs 50,000 under NPS), the tax outgo would be significantly lower at Rs 1.05 lakh under the sweetened NTR.

HRA and other deductions under OTR: How beneficial would these be now?

Take for instance an individual with a gross annual salary of Rs 20 lakh, who claims most major deductions allowed under the OTR to the maximum possible extent. Let us assume that this individual claims deductions totaling Rs 7.75 lakh—Rs 50,000 standard deduction, Rs 1.50 lakh under Section 80C, Rs 25,000 under section 80D, Rs 5 lakh as exemption on house rent, and Rs 50,000 for additional pension contribution.

Even after claiming all these deductions, the tax liability under the OTR comes out to be Rs 1.80 lakh, which is just Rs 5,000, or less than Rs 500 a month, lower than the tax liability of Rs 1.85 lakh under the NTR. Had the HRA exemption been just Rs 15,000 lower—at Rs 4.85 lakh—the tax liabilities under the NTR and OTR would have been almost at the same level.

All taxpayers who have persisted with the OTR due to heavy deductions would do well to revisit their tax computations under both tax systems and make an informed choice.