© The Indian Express Pvt Ltd

Tags:

Incipient signs of softening consumption demand, especially in urban areas, reflected in multiple high-frequency indicators and corroborated by the earnings guidance of consumer goods companies, have raised concerns about a weakening of the growth momentum in the Indian economy.

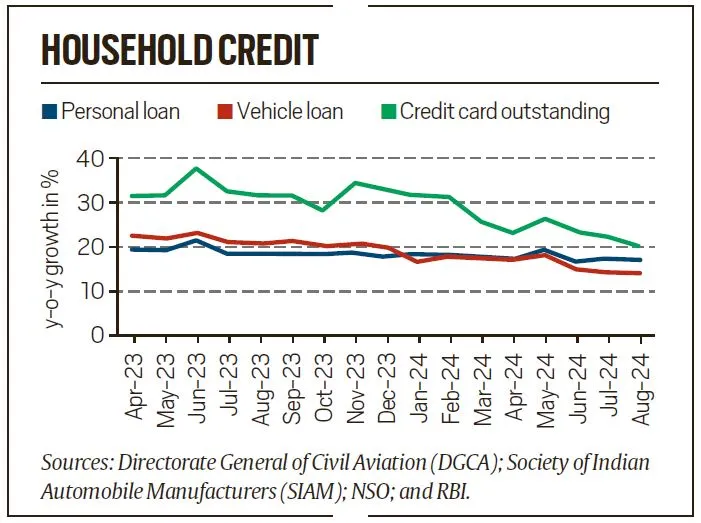

While rural demand is seeing an uptick, high food inflation and a moderation in credit growth are possible headwinds that could slow down growth in the second quarter of 2024-25.

Carmakers are pointing to worries on demand for the sector that has largely bucked India’s consumption downturn so far, blaming it on heavy rains and the election-induced slowdown. All of this could have repercussions for India’s growth story going forward.

The sequential decline in underlying growth momentum is discernible. For Nomura India, the growth glass “looks half empty”, with its latest coincident activity index — a composite index covering consumption, investment and the external sector — pointing to slower GDP growth in the second quarter of 2024-25 compared with the first quarter.

In the first quarter, GDP growth had already moderated to around 6.7 per cent from 7.8 per cent in the previous quarter. During the second quarter of July-September, this could moderate even further to around 6.5 per cent (much lower than RBI’s projected 7 per cent) amid a slowdown in investment and industrial activity that could compound the slowdown in discretionary consumption sector, especially in urban centres, that Nestle and Tata Consumer are alluding to.

“Real wage growth for rural agricultural and non-agricultural workers is providing some support to consumption growth. In the urban areas, new demand is not there. It’s mostly status quo as urban consumers have broadly consumed a lot in the post-Covid phase and exhausted the pent-up demand,” Devendra Kumar Pant, Chief Economist, India Ratings and Research said.

According to the Finance Ministry’s economic review for September, rural demand continues to improve, as reflected in increasing fast moving consumer goods (FMCG) volume sales and a rise in three-wheeler and tractor sales. However, urban demand appears to moderate due to softening consumer sentiments, limited footfall due to above-normal rainfall, and seasonal periods during which people tend to refrain from new purchases, the Ministry said.

Broader data sets clearly point to this: Corporate sector’s growth rates in revenue and profits have taken a beating if the initial trends from the financial results of listed companies for the quarter ended September 2024 are any indication, with the growth rate in net profit of 197 companies down to 6.1 per cent at Rs 83,007 crore in Q2 of 2024-25 as against 27.4 per cent (Rs 78,224 crore) in the same period of last year largely on account of a rise in expenses and input costs in the second quarter, according to data compiled by Bank of Baroda Research. The picture weakens further if the 10 banks in the sample are excluded. Rating firm Crisil said revenue growth of 5-7 per cent for Q2 is likely to be the slowest in the last 16 quarters.

Companies are also scaling down their salary outlays. Real salary and wage expenditure growth of listed non-financial corporates –a proxy for real urban wages – has moderated to 0.8 per cent in Q2 FY25 from 1.2 per cent in Q1 FY25, and is down from 2.5 per cent in FY24 and 10.8 per cent in FY23, Nomura said.

Adding to these stress signals are worries about high food inflation. The RBI has indicated that food inflation continues to be a worry and that it could be risky to talk about cutting rates at this point in time. “At this stage of the economic cycle, having come so far, we cannot risk another bout of inflation. The best approach now would be to remain flexible and wait for more evidence of inflation aligning durably with the target,” RBI Governor Shaktikanta Das wrote in the minutes of the Monetary Policy Committee (MPC) held from October 7- 9.

The other problem is on the external front, where protectionist measures in the US and sluggish demand in western Europe do not promise much for India’s already struggling exports. During the annual meetings of IMF-World Bank in Washington last week, Finance Minister Nirmala Sitharaman said that the output-inflation tradeoff globally has worsened and cooling may slow down the economic momentum — which necessitates continuous data-driven policy adjustments to monitor spillovers.

Speaking on the Indian economy at an event organised by the Peterson Institute for International Economics in Washington on Friday, Das remained upbeat and said that improving domestic demand, lower input costs and a supportive policy environment continue to spur manufacturing activity, while the services sector is displaying strong growth.

“The growth outlook reflects the underlying strength of India’s macro-fundamentals, with domestic drivers – private consumption and investment – playing a major role,” the central bank governor said, adding that the government’s thrust on capex and healthy balance sheets of banks and corporates are expected to support private investment and that private consumption appears to be on track for a strong improvement due to the favourable agricultural outlook and the pickup in rural demand.

So while the lead indicators point to a moderation in growth, certain components of growth, including government spending that had dipped during the election months, could see a pick up in the coming quarters. During April-August, central government expenditure stood at Rs 16.52 lakh crore, down 1.2 per cent from the corresponding period a year ago. Higher government spending along with efforts to bring down inflation could help India’s growth in the second half of this year.

Government spending is likely to pick up as that is overdue, but the continuing moderation in credit growth, particularly consumer credit growth means constraint in terms of discretionary activity could continue. That’s already reflective on the urban demand side. And on whether private capex is picking up, whether it is broadening out, with demand continuing to be soft, the changes of a pickup, especially a broad-based one, are unlikely.

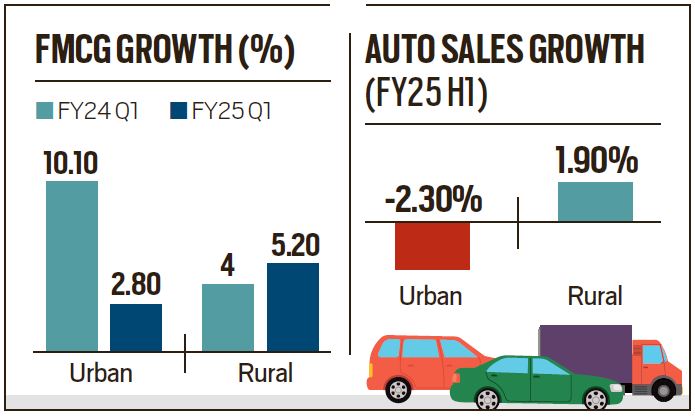

The positives going forward include the festive season demand, and to what extent discounts help boost consumer activity. It would also be crucial to see to what extent government capex picks up and if rural demand will hold. The Finance Ministry has flagged the need to watch the demand conditions at the margin. Citing data from Nielsen IQ, the Ministry said rural demand has strengthened in H1 of FY25, with improvement seen in rising FMCG sales of 5.2 per cent (volume growth) in Q1 FY25 as against 4 per cent seen in the year-ago period. There has also been a pickup in auto sales in rural areas by around 2 per cent in H1 FY24, with a significant increase in three-wheelers (7.4 per cent) and passenger vehicles (4.9 per cent) sales. In urban areas, however, volume growth in FMCG sales has slowed to 2.8 per cent in Q1 in FY25 from 10.1 per cent in Q1 FY24. Auto sales declined by 2.3 per cent in H1 of FY25, mainly due to lower sales in Q2 FY25 in urban areas. Housing sales and launches have also dipped in Q2 FY25, the Ministry said.

Going ahead, a further monetary easing by the US Fed post-elections are expected to boost India’s capital inflows, experts said. A higher real wage growth and above-normal monsoon also augur well for consumption growth going ahead. There is a distinct possibility that government expenditure will be the biggest driver for overall economic recovery, especially if one were to consider the run rate so far and factor in the budget forecast assuming an implied growth in capital expenditure from September to March 25 should be around 40 per cent year on year. Given the contraction seen in April-August, there has to be a big improvement. Revenue expenditures from the government side should also see an improvement, which could have some impact.