© IE Online Media Services Pvt Ltd

Tags:

In early 2021, the restaurant industry was making a dramatic comeback from the pandemic. Investors were hungry for the next big opportunity, and Barbeque Nation — a household name, a first-mover in the live-grill buffet concept, and a casual dining chain riding India’s urban consumption boom — served up exactly that.

When Barbeque Nation launched its IPO in March 2021 at Rs 500 per share, demand was scorching hot. The offering was oversubscribed 6x, signaling immense confidence in its growth story.

In November 2021, the stock surged to a peak of Rs 1,946 — a staggering 290% gain. Analysts were bullish, hailing it as a direct play on India’s rising discretionary spending, a potential multibagger that could scale like Dominos or McDonald’s did in the Quick Service Restaurant (QSR) space.

The numbers seemed to justify the hype.

From FY21 to FY24, revenue soared 150% from Rs 507 crore to Rs 1,255 crore as dining out rebounded. Same-store sales surged, profitability improved, and the brand aggressively expanded into new cities.

Everything looked set for a golden decade of growth.

But then, the euphoria faded.

Fast forward to today, and Barbeque Nation’s stock has crashed over 80% from its peak, wiping out investor gains. What happened? Rising costs, slowing same-store growth, and a business model struggling to sustain its momentum. Suddenly, the market isn’t sure if this is a high-growth restaurant chain or just another discretionary dining brand facing saturation.

With the stock now trading near all-time low, the big question looms: Is this a buffet of value at a deep discount, or has the growth story hit a dead end?

India’s food services industry has evolved dramatically over the past two decades. What was once an unorganised sector dominated by street food vendors and family-run eateries is now a ~ Rs 4.5 trillion ($60 billion) industry with a growing share of organised players, chains, and cloud kitchens.

Casual dining restaurants (CDRs) like Barbeque Nation sit at the heart of this transformation, catering to the urban middle-class consumer’s demand for experiences over just meals.

The organised restaurant segment is projected to grow at a ~13% CAGR over the next five years, faster than the broader food service industry’s ~8% CAGR. Casual dining makes up the largest sub-segment, accounting for 48% of the organised market.

The reason? Unlike Quick Service Restaurants (QSRs) such as McDonald’s or Domino’s, which cater to fast, affordable meals, CDRs like Barbeque Nation offer a premium dining experience, making them a preferred choice for family gatherings, celebrations, and corporate outings.

Yet, while the demand for casual dining is strong, the market is becoming increasingly fragmented and competitive. Brands like Absolute Barbecues (AB’s), Mainland China, and global entrants like Chili’s and Olive Bar & Kitchen are intensifying competition. At the same time, Indian QSR brands (such as Wow! Momo, Behrouz Biryani, and Biryani Blues) are capturing customers who prefer convenience over sit-down dining.

Barbeque Nation is positioned as a premium, fixed-price, all-you-can-eat buffet restaurant, a format that resonates with Indians’ love for variety and indulgence.

The brand pioneered the live table grill concept, where diners can cook skewered starters at their tables, creating an interactive dining experience. It’s a high-footfall business, dependent on repeat customers and special-occasion dining to drive growth.

While this model has worked well, it also means higher costs.

Unlike QSRs, which thrive on low-cost, high-margin fast food, casual dining requires larger outlets, full-service waitstaff, and premium locations (malls, high streets, business districts). Additionally, table turnover rates (how quickly a table is emptied and reused) are lower in buffets, as customers tend to stay longer than in a typical restaurant.

For years, Barbeque Nation’s growth engine ran on three key levers: same-store sales growth (SSSG), new store expansion, and cost control.

These levers worked in tandem — existing restaurants kept growing revenue, new outlets added fresh markets, and efficient cost management ensured profitability.

But as recent data suggests, cracks are beginning to form. Each of these levers is now facing significant challenges, making it harder for Barbeque Nation to scale as effortlessly as before.

For any restaurant chain, same-store sales growth (SSSG) is the ultimate health check. If existing outlets are growing revenue year after year, it means the brand is strong, demand is increasing, and operations are improving.

But when SSSG turns negative, it raises serious questions — are customers losing interest? Is competition eating into market share? Is the business hitting saturation?

For most of its history, Barbeque Nation had steady mid-to-high single-digit SSSG. Between FY15 and FY19, growth averaged 6-8% per year. Even during economic slowdowns, people kept coming back for their buffet meals.

Then came COVID, which wrecked dine-in restaurants everywhere. In FY21, Barbeque Nation’s SSSG plummeted to -44%, a staggering drop caused by lockdowns. But the post-pandemic recovery was equally dramatic — SSSG soared to 27.5% in FY23, fuelled by pent-up demand.

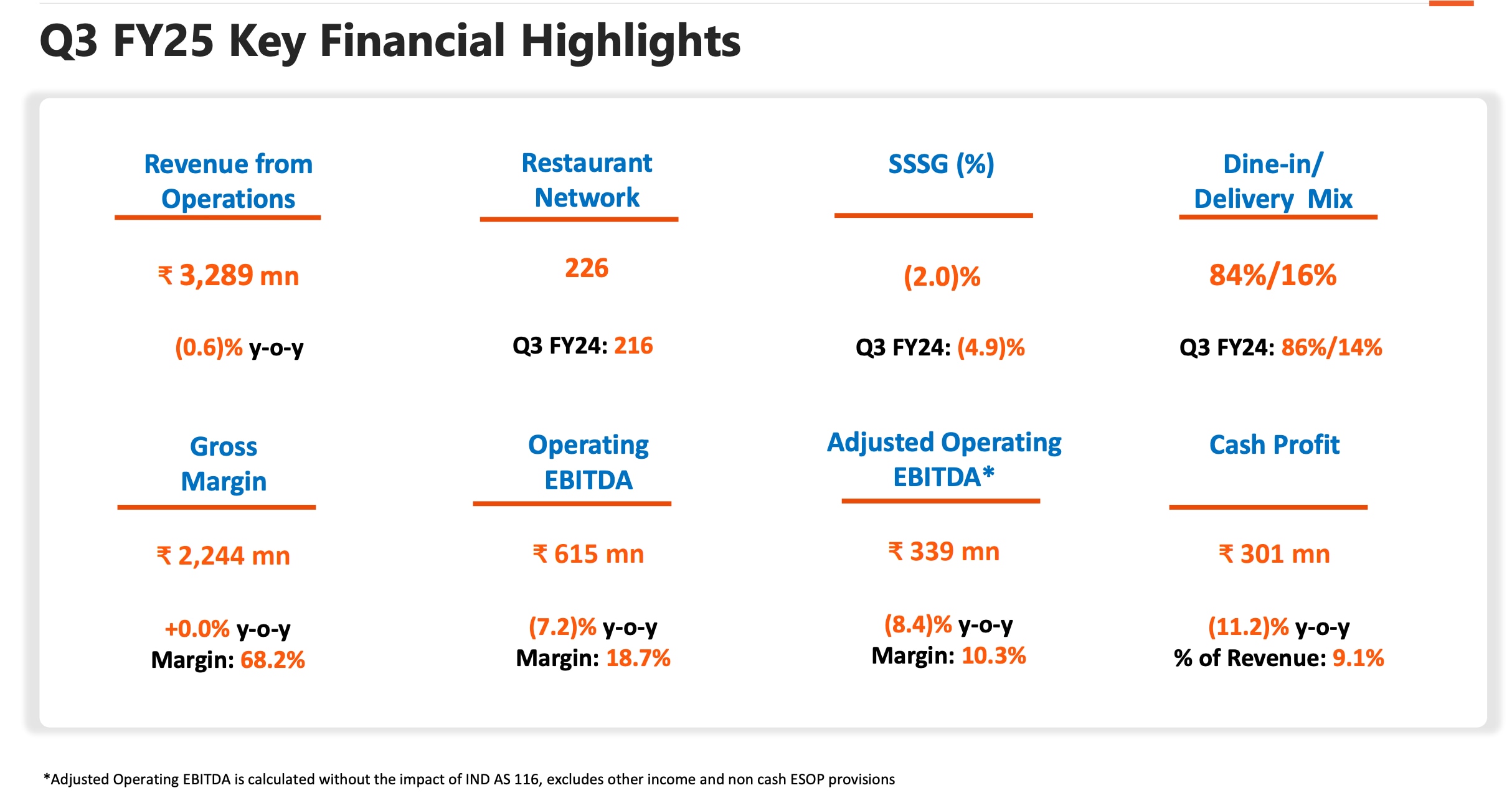

It seemed like Barbeque Nation was back in business. But just a year later, things have taken a sharp turn. In Q3 FY24, SSSG slipped into negative territory again, falling by -4.9% year-over-year.

That’s a worrying signal.

A one-time surge after COVID was expected, but now that demand has normalised, existing restaurants are struggling to keep up.

First, buffet dining isn’t as popular as it used to be. During the early 2010s, Barbeque Nation had a unique positioning — people loved the idea of an unlimited grill experience at a fixed price. But in recent years, consumers have started looking for more premium, experience-driven dining rather than just all-you-can-eat buffets. Post-pandemic, health-conscious customers are also more mindful of excessive eating.

Second, pricing has become a challenge. Barbeque Nation operates in the premium casual dining space, meaning it caters to middle-class and upper-middle-class consumers. But rising competition from brands like Absolute Barbecues, Farzi Café, and premium standalone restaurants has forced it to keep its prices in check. Before the pandemic, a weekend buffet at Barbeque Nation cost ₹1,300+ tax per person. Today, they’ve had to cut prices to ₹1,000+ tax to remain competitive. Meanwhile, rival buffet chains are offering similar experiences for ₹900-950, eroding Barbeque Nation’s pricing power.

And third, customer fatigue is setting in. Barbeque Nation thrives on repeat visits, especially for birthdays, office gatherings, and family outings. But after 10-15 years in the market, the novelty has worn off. Consumers now have plenty of other options, from cloud kitchens and QSR chains to microbreweries and themed restaurants. If people aren’t visiting existing outlets as often, same-store growth will continue to struggle.

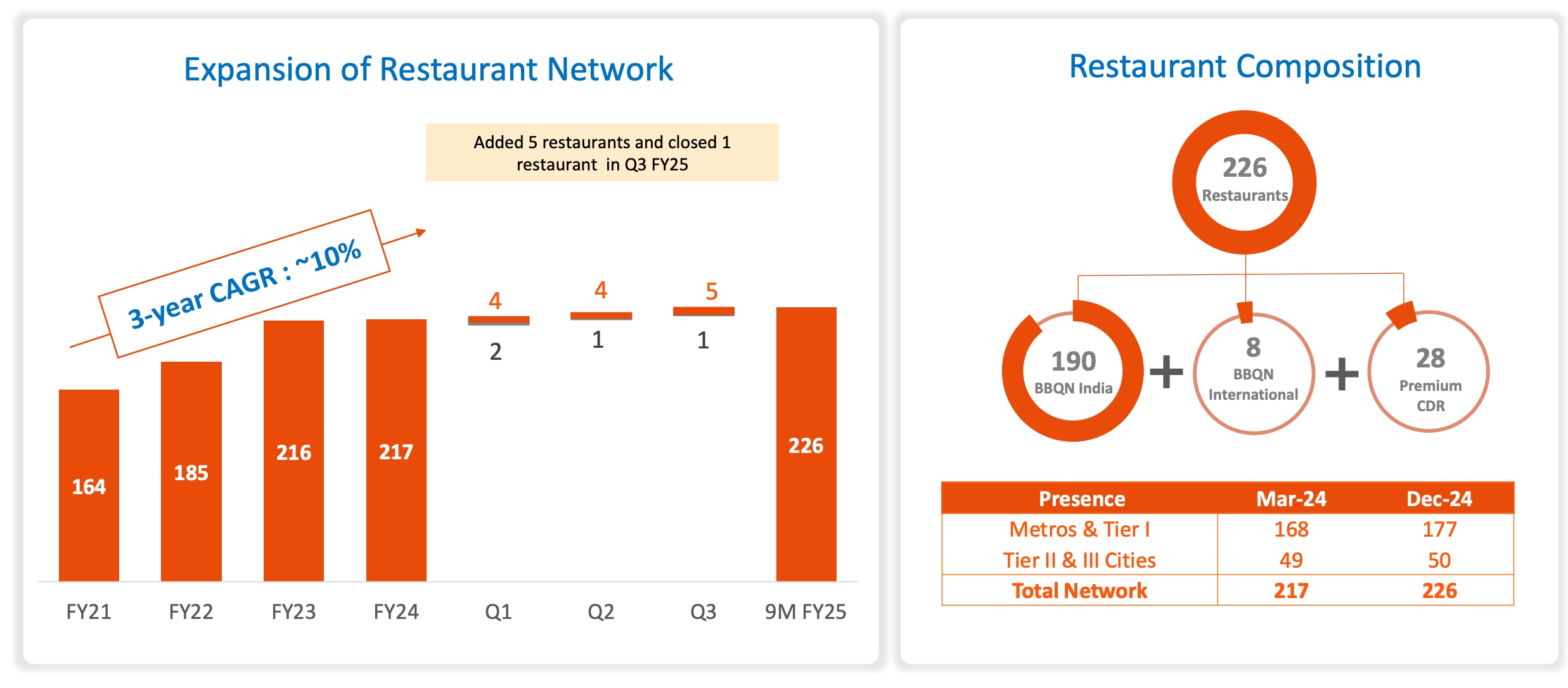

When SSSG slows down, the only way to keep growing revenue is by opening new outlets. That’s exactly what Barbeque Nation has been doing over the last decade.

From 40 outlets in FY15, the company expanded to 164 by FY21. The post-IPO phase saw even more aggressive expansion, with a target of 300+ outlets by FY24. But as of today, they have only 226 restaurants, far below initial projections.

One major reason is high capital costs. Opening a Barbeque Nation outlet isn’t cheap — it requires Rs 2.5-3 crore in upfront investment for kitchen equipment, interiors, staff training, and rent deposits. In the early years, this wasn’t a problem because new outlets quickly became profitable. But today, each new restaurant takes 3-4 years to break even, meaning the return on investment is much lower than before.

Real estate is another challenge. In metro cities, prime locations are either too expensive or already have existing outlets, leading to cannibalisation — new stores steal business from old ones instead of expanding the market. Meanwhile, in Tier-2 and Tier-3 cities, demand isn’t as strong, meaning new outlets struggle with low footfalls and lower per-customer spending.

The numbers tell the story.

Between FY23 and FY24, the company effectively opened just one restaurant. This year, Barbeque Nation opened 13 new outlets but also shut down 4 underperforming ones. The fact that some locations are being shut down suggests that new restaurant openings are no longer a guaranteed success.

Restaurant utilisation rates are also under pressure. In the best-performing outlets (mostly metro locations), each table was used possibly four times per day on average, ensuring high revenue per store. But in smaller cities, this figure has fallen to 1.2-1.3 turns per day, making profitability harder to achieve.

If Barbeque Nation can’t expand profitably and existing outlets aren’t growing revenue, where does future growth come from?

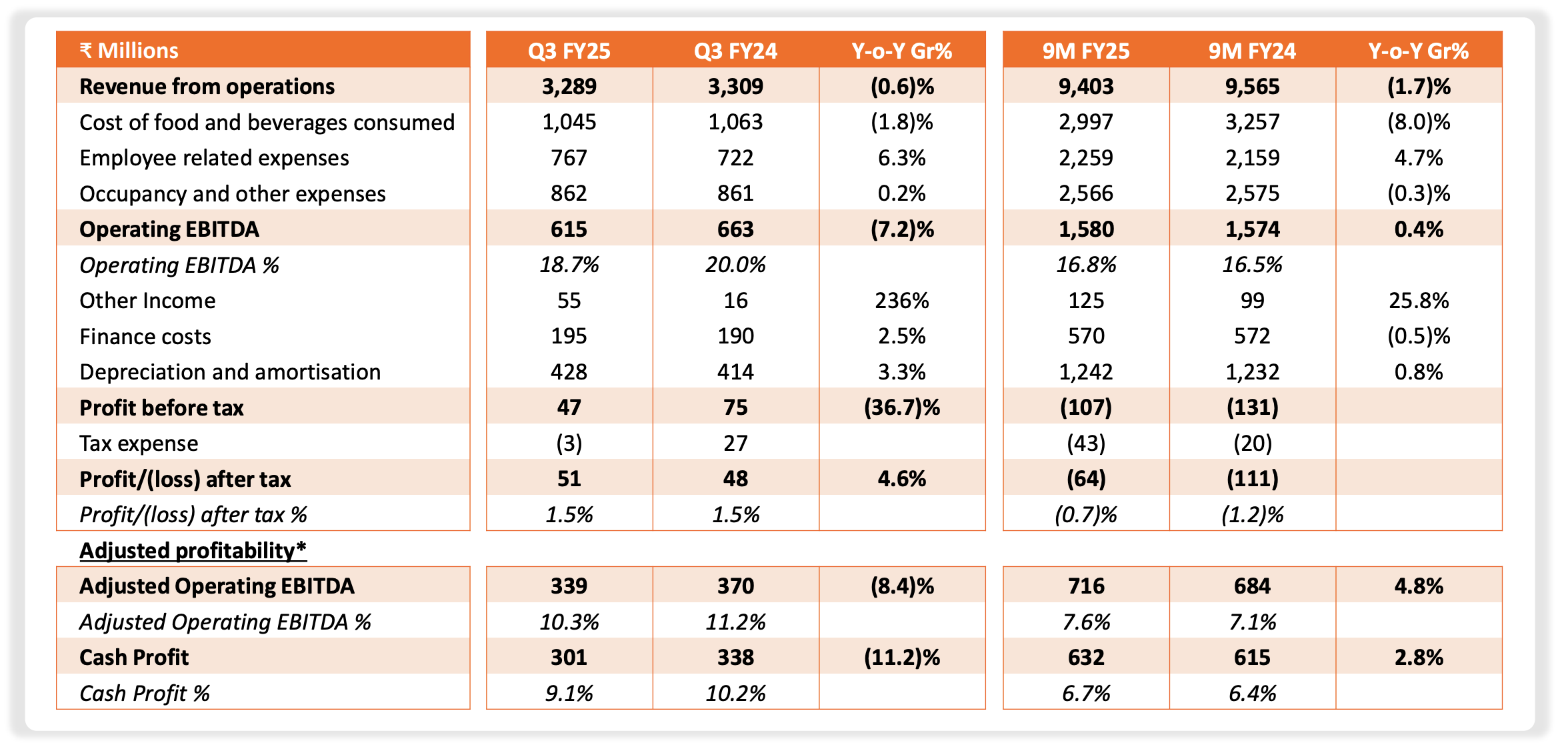

Even as revenue has grown, costs have risen even faster, making it harder for Barbeque Nation to maintain profitability.

The biggest burden is rent and occupancy costs, which have escalated to nearly 26% of revenue — alarmingly high for the restaurant industry.

The issue is that rent is a fixed expense, meaning it remains constant regardless of how much revenue an outlet generates. Essentially, the same high-cost real estate is being underutilised, making rent a much heavier burden on profitability. In a typical restaurant, rent is considered reasonable when it is around 10-15% of revenue, but at 26%, it is unsustainably high unless revenue growth returns.

Labour costs have also surged. Unlike QSR chains, which can automate much of their operations, Barbeque Nation requires waitstaff, kitchen staff, and grill attendants, all of whom need to be trained. Employee costs have risen by 6% YoY, further squeezing margins.

With its stock down 80% from its peak, Barbeque Nation is trading at what seems like an attractive valuation. But is it truly cheap, or is the market pricing in deeper structural problems?

One of the biggest concerns is Barbeque Nation’s leveraged balance sheet. Unlike QSR chains, which operate on a capital-light franchise model, Barbeque Nation owns and operates most of its outlets. This means each new restaurant requires Rs 2.5-3 crore in capital expenditure, financed largely through a mix of debt and internal accruals.

As of FY24, Barbeque Nation has Rs 500+ crore in debt, making it one of the most leveraged companies in the restaurant sector. Its debt-to-equity ratio is above 1, indicating that a large portion of its growth has been debt-funded. While this was sustainable when same-store sales were rising, negative SSSG and shrinking margins make debt repayment a concern.

The company’s interest coverage ratio (EBITDA/interest expense) has also weakened, meaning a higher share of its operating profits is being used to pay interest costs instead of reinvesting in growth. This is a stark contrast to QSR chains like Jubilant FoodWorks (Domino’s) and Devyani International (KFC, Pizza Hut), which have asset-light, high-margin businesses with lower debt.

To determine whether Barbeque Nation is a bargain, let’s compare its EV/EBITDA multiples (approx numbers and based on data from Tijori Finance) with competitors in the restaurant space.

|

Company

|

EV/EBITDA

|

EBITDA Margin

|

Net Profit Margin

|

|

Jubilant FoodWorks (Domino’s, Dunkin’)

|

28x

|

22-24%

|

8-10%

|

|

Devyani International (KFC, Pizza Hut, Costa Coffee)

|

27x

|

20-22%

|

6-8%

|

|

Westlife Foodworld (McDonald’s India – West & South)

|

31x

|

18-20%

|

3-6%

|

|

Specialty Restaurants (Mainland China, Oh! Calcutta, Sigree)

|

10x

|

12-14%

|

3-5%

|

|

Barbeque Nation

|

8x

|

15-17% |

At first glance, Barbeque Nation looks undervalued, trading at 8-9x EBITDA, much cheaper than Jubilant (28x EBITDA) or even Devyani (27x EBITDA).

However, there are good reasons why the market is assigning such a low multiple:

Lower and shrinking margins: QSR chains like Domino’s and KFC have 22-24% EBITDA margins, while Barbeque Nation is struggling at 15-17%, with recent quarters showing even lower margins.

Slowing growth vs competitors: While Barbeque Nation’s revenue grew 150% in three years, much of this was a post-pandemic recovery rather than organic growth. In contrast, QSR chains have steady mid-to-high teen revenue growth with expanding store counts.

Capital-intensive model vs asset-light competitors: Jubilant, Devyani, and Westlife operate mostly through franchises, reducing capital expenditure requirements. Barbeque Nation’s owned-store model means high debt and lower return on invested capital (ROIC).

Negative SSSG signals a structural problem: Barbeque Nation’s declining SSSG is a red flag, while QSRs continue to show positive same-store growth, indicating demand resilience.

At 8-9x EBITDA, Barbeque Nation looks like a value buy on paper, but the market is clearly sceptical of its ability to return to strong, profitable growth.

The key concerns are:

Same-store sales are declining at a time when competitors are still growing.

High fixed costs (rent at 26% of revenue) make it vulnerable to revenue fluctuations.

A leveraged balance sheet with Rs 500+ crore in debt limits financial flexibility.

Competition from both QSR chains and premium casual dining brands is intensifying.

While Barbeque Nation could be a turnaround play, the risk is that its business model may not be as scalable or profitable as initially expected. Unlike QSRs, which have high-margin, repeat business, and rapid scalability, casual dining chains face higher costs, limited pricing power, and slower expansion potential.

Barbeque Nation is cheap, but that doesn’t automatically make it a buy. The stock has been punished for real reasons — weakening sales, shrinking margins, and an expensive business model. Investors will need to see fundamental improvements before confidence in its growth story is restored. Until then, it remains a high-risk, high-reward turnaround bet rather than a proven compounding machine like Jubilant or Devyani.

(Errata – Same-Store Sales Growth (SSSG) Clarification

In an earlier version of this article, we stated that Barbeque Nation reported a -10.7% YoY Same-Store Sales Growth (SSSG) in Q3 FY24. This figure referred to Q2 FY24, not Q3, and was accurately sourced from the company’s Q2 FY24 investor presentation.

The correct SSSG figure for Q3 FY24 is -4.9%, as per the company’s Q3 FY24 earnings report.

We regret the oversight in attribution and have updated the article accordingly. This correction does not affect the core argument regarding the sequential decline in SSSG across FY24, which remains a key concern in the company’s growth narrative.)

Note: We have relied on data from the annual report and industry reports for this article. For forecasting, we have used our assumptions.

Parth Parikh has over a decade of experience in finance and research, and he currently heads the growth and content vertical at Finsire. He has a keen interest in Indian and global stocks and holds an FRM Charter along with an MBA in Finance from Narsee Monjee Institute of Management Studies. Previously, he has held research positions at various companies.

Disclosure: The writer and his dependents do not hold the stocks discussed in this article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.