© IE Online Media Services Pvt Ltd

Tags:

Sumitomo Mitsui Banking Corporation’s (SMBC) agreement to acquire a 20% stake in Yes Bank at Rs 20 per share on May 14 has sparked new investor optimism. But can Japan’s banking heavyweight truly reignite growth and profitability at the struggling Indian lender?

Since its restructuring in 2020, Yes Bank’s stock has largely traded between Rs 11 and Rs 30 per share. Except for a brief rally from July 2022 to July 2024, it has consistently underperformed the NIFTY 50 Index.

The real question is: Will SMBC be able to maintain pristine asset quality and grow fast, and more importantly, drive strategy change that Yes Bank needs?

Yes Bank: Historical turning points

2016-19: Rapid rise and spectacular fall

Once amongst India’s fastest-growing private banks, Yes Bank built a Rs 3 lakh crore loan book by FY19 but saw asset quality deteriorate sharply. Gross Non-Performing Loans (GNPLs) breached 17 percent by March 2020. A run on deposits forced the RBI to intervene in March 2020, imposing a moratorium and engineering a rescue plan led by SBI (Source: Yes Bank FY24 Annual Report).

2020 Reconstruction

A Rs 10,000 crore capital infusion by SBI, HDFC, and others, followed by a follow-on public offering of Rs 15,000 in July 2020, stabilised the bank. A follow-on public offering (FPO) is when a company that’s already listed issues additional shares to the market to raise more equity capital.

Over the next two years, Yes Bank focused on cleaning its books — writing off legacy stressed assets, resolving NPLs via security receipts, and rebuilding provision buffers.

2022–24: Gradual recovery

By Q4 FY24, gross NPLs fell to 1.8 percent and net NPA to 0.4 percent, with a provision coverage ratio (PCR) above 76 percent. Loan growth resumed in SME and mid-corporate segments, and deposits grew over 20 percent YoY as the CASA ratio inched back toward 31 percent.

Q1–Q4 FY25: Stabilisation ahead of SMBC

In FY25, net interest income grew 10.5 percent to Rs 8,944 crore, non-interest income expanded to 1.4 percent of assets, and cost-to-income improved by 310 basis points to 71.3 percent. However, as of Q4FY25, Return on Assets (ROA), a common profitability metric for banks and financials, remained muted at ~0.6%, underscoring lingering profitability headwinds.

Profitability puzzle

A data roundup of 36 listed banks by Boston Consulting Group (BCG) reported an average ROA of 1.4%. In contrast, Yes Bank’s ROA stood at 0.6% for FY25.

This is because key operating parameters such as Net Interest Margins and cost-to-income are below the industry average.

The primary reason: a significant chunk of Yes Bank’s assets are parked in low-yield government accounts due to Priority Sector Lending (PSL) shortfalls.

As of Q3 FY25, PSL-shortfall-related assets made up 8.7% of Yes Bank’s total assets, down from a peak of ~11% in March 2024. These assets yielded just 2.97% in FY24. The Yes Bank management estimates that if this PSL burden were eliminated, NIMs would improve to around 3.0–3.1%.

The RBI mandates that banks must lend 40% of their deposits to farmers and small businesses (this is called Priority Sector Lending, or PSL). If a bank can’t find enough worthy borrowers in those areas, then it must park that money in special government accounts where they earn minimal interest.

Because that parked money makes little or no profit, it drags down the bank’s overall profit margin (NIM). In short, banks lose out on earnings whenever they have to keep money in low-interest government accounts instead of lending it at higher rates.

These assets held in lieu of PSL shortfalls represent a substantial portion of total assets. It peaked at ~11% as at March 31, 2024 and currently stands at 8.7% in Q3FY25, generating a considerably lower yield (average realised yield of 2.97% in FY 2023-24) compared to other assets.

Cost-to-Income remains elevated

A comparison of Yes Bank’s NIMs (2.5%) and cost-to-income (71%) versus various categories of banks/small finance banks places it in the worst possible buckets across both metrics.

The bank is aiming to reduce PSLC mandated assets to less than 5% and while there is no specific guidance for cost to income trajectory, it is expected to trend downward.

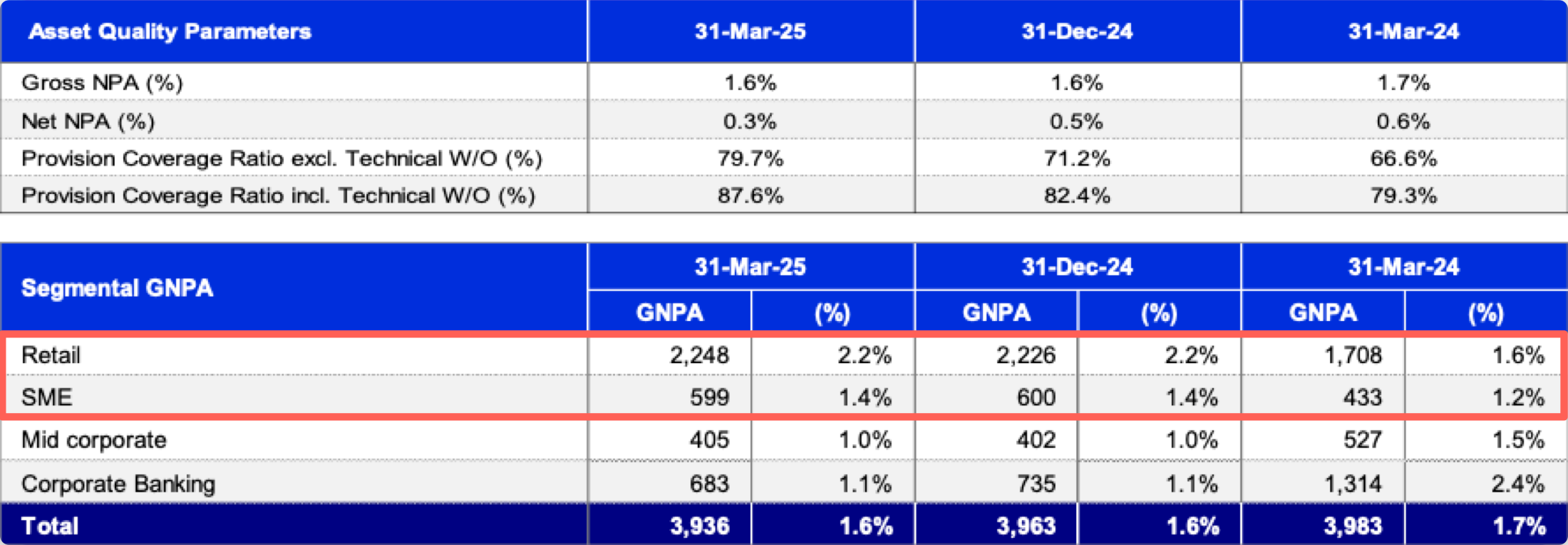

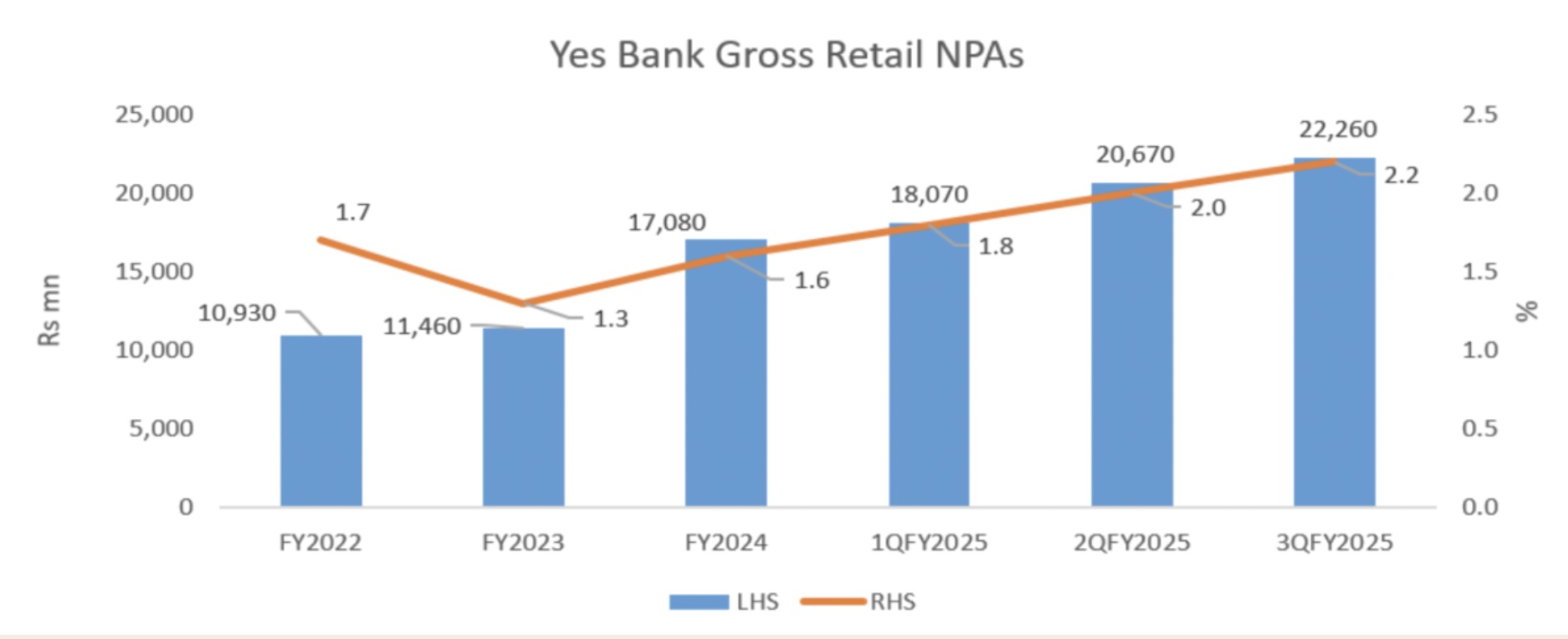

Asset quality is okay, retail asset quality is deteriorating

The overall asset quality is stable and the bank is reported to be at its “best ever since March ’20 quarter”.

Gross Non Performing Assets (GNPA) are down to 1.6% in FY25 from 1.7% in FY24 and net NPA is down to 0.3% from 0.6% during the same period.

However, the retail segment (including Personal Loans, Credit Cards, Microfinance/ISB) contributed significantly to recent slippages.

The bank’s retail-led turnaround strategy has not yielded the desired outcome.

In June 2024, Yes Bank laid off over 500 junior staff, mostly from its retail division. Nearly a year later, it reportedly removed four senior executives, three of whom were from retail.

According to Hemindra Hazari, a SEBI registered research analyst who has covered the capital market and financial sector for 30 years, “The rise in the bank’s 31-90 days overdue retail loans indicates a future rise in retail NPAs. As the entire banking industry is expected to have worsening retail asset quality, Yes Bank’s retail portfolio is particularly vulnerable. The low yield on retail loans should have normally resulted in high quality, but the bank has got the worst of both worlds, which reflects extremely poorly on its sourcing and credit risk management.”

Can SMBC unlock the franchise?

SMBC India, with total assets in India at Rs 52,000 crore, earns a ROA of 1.2-1.3% and has zero NPAs since inception in 2012.

In FY24, its cost of borrowing was 6.1%, whereas Yes Bank had a cost of borrowing of 6.4%. In the first 9 months of FY25, the number was 6.5% and 6.3%, respectively.

According to Moody’s, the acquisition should be a credit positive for Yes Bank, which should result in better credit ratings and lower funding costs.

By securing a 20 percent stake, SMBC gets pro rata rights in any future equity raise. Additionally, two SMBC nominees will join Yes Bank’s board immediately. This could usher in Japanese-style discipline in underwriting and provisioning — a potential game-changer.

Success, however, will depend on seamless cultural integration, technology harmonisation, and talent alignment. Additionally, the RBI may cap SMBC’s voting power at 20%, limiting its effective control.

Valuation and investor lens

At ~Rs 20/share, Yes Bank trades at ~1.36x its FY25 book value, slightly above the industry average of 1.27x.

At the current valuation, the market is pricing in a reasonably successful SMBC integration. While SMBC’s entry should help regain Yes Bank’s long-lost trust, it is too soon to speculate as to where the chips may fall.

Note: We have relied on data from http://www.Screener.in and http://www.tijorifinance.com throughout this article. Only in cases where the data was not available have we used an alternate, but widely used and accepted source of information.

Rahul Rao has helped conduct financial literacy programmes for over 1,50,000 investors. He has also worked at an AIF, focusing on small and mid-cap opportunities.

Disclosure: The writer or his dependents do not hold shares in the securities/stocks/bonds discussed in the article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.