© The Indian Express Pvt Ltd

Tags:

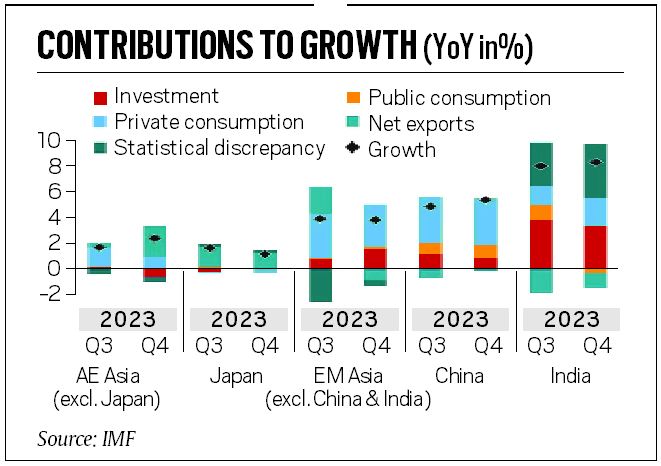

Public investment remains an important driver for India, making it the world’s fastest growing major economy, the International Monetary Fund (IMF) said in its latest remarks on the Regional Economic Outlook for Asia and Pacific released Tuesday. The IMF also said that headline inflation may see further reductions due to lower energy prices in several economies in the Asia and Pacific region, but food price pressures – especially for rice – may slow headline disinflation in India.

The IMF had earlier this month raised India’s growth forecast for the financial year 2024-25 to 6.8 per cent from 6.5 per cent earlier and retained the growth forecast for 2025-26 at 6.5 per cent. India and the Philippines have been the source of repeated positive growth surprises, supported by resilient domestic demand, the IMF said.

The IMF has also raised the regional growth forecast for Asia and Pacific to 4.5 per cent, up 0.3 percentage point from six months earlier, reflecting upgrades for China, where policy stimulus is expected to provide support. But the growth forecast for the region is slower than 5 per cent growth in 2023.

Global disinflation and the prospect of lower central bank interest rates have made a soft landing more likely, hence risks to the near-term outlook are now broadly balanced, Krishna Srinivasan, Director, Asia and Pacific Department said in a blog post. Asian central banks should continue to focus firmly on domestic price stability and “avoid making policy decisions overly dependent” on anticipated interest rate moves by the US Federal Reserve, Srinivasan said.

In a still subdued external environment, robust private consumption will remain the main growth driver in Asia’s other emerging market economies, he added.

For inflation, the IMF said it is already at or close to target in emerging markets and there is heterogeneity in inflation drivers going forward. “Core inflation is largely expected to remain contained. As for headline inflation, several economies may experience further reductions due to lower energy prices while in others (for example, India), food price pressures—especially for rice—may slow headline disinflation,” the IMF said.

Asian countries are better placed than before to cope with exchange rate movements, with fewer financial frictions and better macro-fundamentals and institutional frameworks and should continue to allow the exchange rate to act as a buffer against shocks, he said. Advancing fiscal consolidation is an urgent priority both to lessen the burden of higher debt levels and interest costs and to rebuild the fiscal space needed to address medium-term structural challenges.

The IMF said China is a source of both upside and downside risks. “Policies aimed at addressing stresses in the property sector and to boost domestic demand will both help China and the region. But sectoral policies contributing to excess capacity will hurt China and the region. Geoeconomic fragmentation remains a significant risk,” it said. Growth rate for China, the world’s second-largest economy, is projected to slow from 5.2 per cent in 2023 to 4.6 per cent this year and 4.1 per cent in 2025.

Global conflict poses additional risks to trade, as evidenced by the re-routing of ships around Africa to avoid the Red Sea, which raises shipment costs, Srinivasan said. “For Asia’s economies these are unfortunate developments, as many of them are deeply integrated into global supply chains and benefit greatly from trade. Hence policymakers should be cautious to not aggravate trade frictions themselves,” he said.