Eight years after its launch, India’s Goods and Services Tax (GST) is undergoing its most significant transformation. GST 2.0 prioritises long-term structural reform over immediate revenue maximisation. As the government prepares to implement these changes, the real issue isn’t whether revenues will dip initially, but how these changes will be executed to unleash the full potential of a simplified, business-friendly tax system that can power the next phase of India’s economic growth.

At its core, GST 2.0 aims to reduce the complexity that has plagued India’s tax system since independence. The reform’s centrepiece lies in collapsing the current four-slab consumer goods structure (5 per cent, 12 per cent, 18 per cent, 28 per cent) into a more streamlined rate slab of 5 per cent and 18 per cent. Special rates of 0.25 per cent and 3 per cent remain with a new special rate of 40 per cent for a select few items.

The numbers tell a compelling story. Out of 506 goods listed in the GST Council’s recommendations, a remarkable 90 per cent of categories have seen rate reductions. Only 52 items see an increase, while most goods transition sensibly from the now-eliminated 12 per cent bracket to 5 per cent. Meanwhile, 52 items have been granted complete tax exemptions, signalling the government’s commitment to making essential goods more affordable.

The new 40 per cent rate for select luxury and sin goods, replacing the previous 28 per cent plus cess structure, brings mathematical clarity while maintaining the principle that luxury consumption should bear a higher tax burden. Removing the compensation cess on coal, lignite, and peat, even as tax rates rise from 5 per cent to 18 per cent would boost the bottom line of struggling power distribution companies, while luxury items graduating to the 40 per cent bracket reinforces progressive taxation principles.

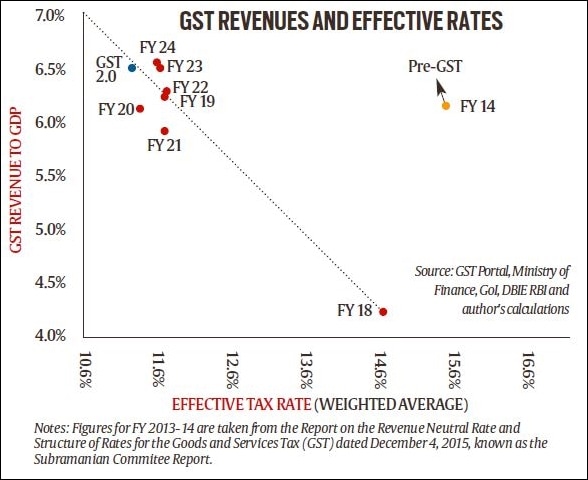

Analysts fixating on the immediate revenue impact are missing the forest for the trees. Yes, GST collections are projected to drop from Rs 20.2 lakh crore to Rs 19.7 lakh crore in the short term, an Rs 48,000 crore reduction based on FY24 data that aligns with government estimates. We estimate the effective rate to decrease marginally from 11.64 per cent to 11.43 per cent in the short term. But this temporary revenue sacrifice follows classic economic logic, embodied in the “Laffer curve”: Lower rates can eventually generate higher collections through expanded compliance and economic activity. Higher revenue collection would depend on two critical factors: Whether businesses actually pass the tax changes on to consumers, and how sensitive consumer demand is to price changes. Research shows that key products moving to the new 40 per cent tax bracket, including soft drinks and tobacco, for example, have relatively inelastic demand, meaning consumers don’t dramatically reduce purchases even when prices rise.

Beyond these demand-side considerations, the reform addresses a more fundamental issue: India’s persistent tax gap. We estimate that the difference between actual and potential collections has kept the country’s tax effort hovering around 70 per cent for over a decade. This represents enormous untapped potential. GST 2.0 directly addresses this challenge by reducing the compliance burden and enhancing voluntary participation in the formal economy.

Markets, however, often focus on the short term, and expectations of higher fiscal deficits due to lower revenues (combined with higher expenditures to support exporters affected by potential trade disruptions) have triggered negative immediate reactions. We expect this to stabilise, particularly given India’s recent sovereign credit rating upgrade and the government’s steadfast commitment to fiscal consolidation.

Despite rate rationalisation capturing headlines, GST 2.0’s institutional reforms deserve equal attention. The operationalisation of the Goods and Services Tax Appellate Tribunal (GSTAT) will finally provide businesses with a dedicated forum for appeals, ending years of procedural uncertainty. While the streamlined slab structure and higher sin taxes may trigger more classification disputes and burden businesses even more with unused input tax credits from inverted duty structures, the GST Council’s commitment to faster refunds offers crucial relief by improving cash flows for affected companies.

Small exporters, long disadvantaged by cumbersome refund processes, will benefit from the removal of threshold limits on low-value export consignments. The amendment allowing Indian intermediaries to claim export benefits when supplies shift to foreign client locations removes a significant barrier to international trade competitiveness.

Perhaps most significantly, the voluntary simplified registration scheme for low-risk businesses with monthly output tax liability under Rs 2.5 lakh acknowledges that one-size-fits-all compliance creates disproportionate burdens for smaller enterprises. This targeted relief could bring thousands of marginal businesses into the formal tax net.

GST 2.0 carries several other strategic benefits. By raising tax rates on goods and services typically consumed by younger demographics (ultra-processed food, social media, and online gaming, what the Chief Economic Advisor referred to as the “deadly troika”), GST aims to better harness India’s demographic dividend. Similarly, deterrent rates on tobacco and aerated drinks serve public health objectives while generating revenue from products with inelastic demand.

The September 22 operational date might seem like a minor administrative detail, but successful implementation will require meticulous coordination across the entire value chain. Previous GST transitions worldwide have shown that even small glitches can cascade into major business disruptions. Malaysia’s experience illustrates this clearly: It rolled out GST in 2015 but abolished it in 2018 as businesses struggled to adjust their systems and processes.

The government’s challenge is ensuring that the benefits of simplification aren’t undermined by implementation hiccups. This would require robust training for tax officials (including at the state-level), clear communication to businesses, and quick resolution of technical issues that inevitably arise during such systemic changes.

All in all, GST 2.0 embodies Prime Minister Narendra Modi’s vision of a streamlined tax framework designed for long-term revenue growth rather than short-term collection maximisation. The reform bets that simplification, reduced compliance costs, and enhanced voluntary participation will eventually generate more revenue than the current complex system. Ultimately, the success of GST 2.0 will equally depend on taxpayers embracing higher voluntary compliance.

This is economic logic backed by international experience. Studies by the OECD and IMF show that countries that successfully simplify their tax systems typically see initial revenue drops, followed by sustained growth as compliance improves and economic activity expands. India’s GST 2.0 represents not just tax reform, but a strategic investment in the country’s economic future.

Mishra is Professor of Economics, Ashoka University, and Director and Head, Ashoka Isaac Center for Public Policy. Mukherjee is a research associate, Observer Research Foundation. Views are personal