Journalism of Courage

Premium

This is an archive article published on January 6, 2020

I-T notifies some returns for AY2020-21; simple ITR not for those owning house jointly

Usually, the I-T Department notifies the ITR forms in the first week of April of the relevant assessment year.

Usually, the I-T Department notifies the ITR forms in the first week of April of the relevant assessment year.

Usually, the I-T Department notifies the ITR forms in the first week of April of the relevant assessment year.

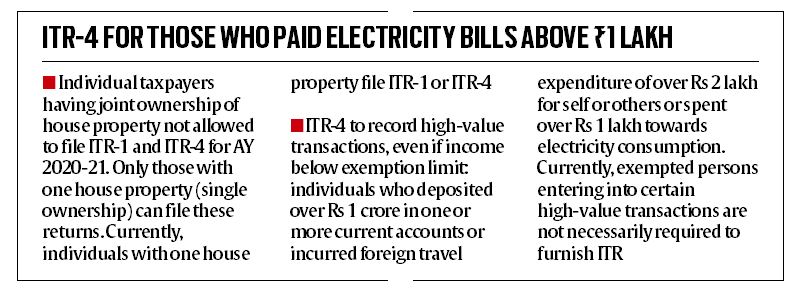

Carving out a separate category for individual taxpayers in the annual income tax returns (ITRs), the Income Tax Department has specified that those having joint ownership of a house property will not be eligible to file the Sahaj (ITR-1) or Sugam (ITR-4).

Notifying the two ITRs for assessment year 2020-21, the Central Board of Direct Taxes (CBDT) also followed up on the Budget announcement to mandate filing of ITR-4 for those individual taxpayers who have paid Rs 1 lakh in electricity bills in a year or spent Rs 2 lakh on foreign travel.

ITR-1 is the income tax return for individual taxpayers having total income upto Rs 50 lakh and includes mainly salaried taxpayers, while ITR-4 is filed by individuals having business income, HUFs and firms (other than LLPs) having a total income of up to Rs 50 lakh from business and profession and filing return under presumptive taxation scheme.

Though the CBDT has issued two forms — ITR-1 and ITR-4 — for AY2020-21, the return filing utility is yet to be activated, and thus, a taxpayer who is required to file the return before the end of the previous year cannot do so until the return filing facility is activated on the e-filing portal.

Other returns are expected to be notified before the end of this fiscal year.

Usually, the I-T Department notifies the ITR forms in the first week of April of the relevant assessment year.

“There are two major changes in the ITR Forms — first, an individual taxpayer cannot file return either in ITR-1 or ITR4 if he is a joint-owner in house property; second, ITR-1 form is not valid for those individuals who have deposited more than Rs 1 crore in bank account or have incurred Rs 2 lakh or Rs 1 lakh on foreign travel or electricity, respectively,” Naveen Wadhwa, DGM, Taxmann said.

Story continues below this ad

In Budget 2019-20, presented in July last year, the government had proposed to make filing of ITRs mandatory for certain individuals even if their income is below the taxable limit such as those depositing over Rs 1 crore in current account, those with over Rs 2 lakh expenditure on foreign travel, those spending over Rs 1 lakh on electricity bills and any person claiming benefits of tax exemption from long term capital gains under various provisions under section 54 of the Income-tax Act.

Currently, a person other than a company or a firm is required to furnish the return of income only if his total income exceeds the maximum amount not chargeable to tax, subject to certain exceptions. Therefore, a person entering into certain high-value transactions is not necessarily required to furnish his return of income.

Advertisement

Live Blog

Advertisement

PHOTOS

Top Stories

Advertisement

Must Read

Advertisement

Buzzing Now

TrendingAustralian man lists ‘top 5 things he can’t do’ in front of his Indian girlfriend, wins hearts on the Internet: ‘Bhai ki fielding set hai’

Trending‘7 days per week, 12 hours work’: IIT alumni-led AI startup Giga faces controversy as employee quits in a day, cites toxic workplace

TrendingIndian wealth management coach reveals billionaire mindset, reveals problems of being rich: 'Pressure due to social media'

- 01

- 02

- 03

- 04

- 05

Advertisement