Tags:

No near-term material upside in KG-D6,volumes to hover around current levels

Sequential improvement driven by refining,government approvals the key for E&P division RIL reported Q2FY13 Ebitda (earnings before interest,taxes,depreciation,and amortisation) of R77.1bn (-22% year-on-year,+14% quarter-on-quarter) and profit after tax of R53.8bn (-6% y-o-y,+20% q-o-q),5% and 2% below our estimates.

Net financial income contributed a high 20% of PBT (profit before tax). In our view,Q2FY13 was an expectedly strong quarter sequentially,driven by robust GRMs (gross refining margins),which we expect to moderate in coming quarters. Petchem margins remain subdued. Domestic E&P volumes continue to decline. We maintain an Underweight rating on the stock.

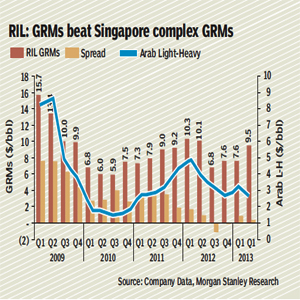

Entire sequential improvement driven by refining: RILs Q2FY13 GRMs were $9.5/bbl (barrel),up 25% q-o-q and at a $0.4/bbl premium over Singapore complex GRMs,but down 6% y-o-y. RIL attributed the better GRMs to overall improved product spreads and its flexibility to optimise refining yields to maximise margins.

The throughput of the refinery improved to 17.6 mt,up 1.7% on a q-o-q basis. Reported Ebit (earnings before interest and taxes) of R35.4bn for the division was up 65% q-o-q and 15% y-o-y. We highlight that the recent strength in GRMs is largely driven by unexpected refinery shutdowns globally,which we now expect to reverse. Coupled with additional new refinery capacity in China in Q4FY12 and onwards,this should put downward pressure on GRMs.

E&P

KG D6 volumes continue to decline: Gas volumes were down 12% q-o-q,averaging 28.5 mmscmd (million metric standard cubic metre per day) for Q2FY13; oil was down 12% to 8.7kbpd (thousand barrels per day). RIL continues to highlight that complexity of reservoir and higher water cut have been causing the production decline. Oil and gas production from PMT (Panna-Mukta-Tapti) fields was also down 9% and 6% q-o-q,respectively; these fields are in natural decline.

Government approvals are the key for the inventory of several E&P projects:

(i) Revised FDP for existing D1-D3 fields: In August 2012 RIL-BP submitted a revised Field Development Plan for currently producing D1-D3 fields to the management committee (under the ministry of petroleum & natural gas). This revised FDP calls for installation of increased water handling capacity and additional compression capacity over the next 2-3 to address the decline in reservoir pressure. RIL believes this will help it to increase the reserve life of current producing fields.

RIL with its partner BP plans to submit an integrated plan in 2HFY13. It will include its four satellite discoveries; R series and D26,to enhance overall production. RIL is currently planning to do the geophysical surveys,engineering studies and FEED (front end engineering & design) studies.

The company has received approvals for pre-development activities (seismic survey,engineering studies,etc.),but for the development work to start,the company will require further regulatory approvals.

n RIL has highlighted that it will take 3-4 years from the date of government approvals for these discoveries to start producing. Thus,we do not see any near-term material upside in KG-D6 and expect volumes to hover around current levels.

Gas price hike: RIL commented that it remains in dialogue with the government on the issue of a price hike. It firmly believes in moving towards market-linked gas prices.

Shale gas JVs: RIL claimed good progress in its shale gas joint ventures as gas prices recovered from the sub-$2/mcf (million cubic feet) level in the USA. RIL has invested $4.8 bn in all three JVs put together. For H1FY13,RIL reported revenues of $253m and Ebitda of $198m from the shale gas JVs. The shale gas numbers are not part of the reported standalone numbers and full details will be disclosed in the consolidated results at the end of the year. For the full year,we estimate that shale gas will generate $355m in Ebitda.

Morgan Stanley